Introduction: The 2026 AI Healthcare Landscape — $36.7B Market, Five Distinct Categories

The healthcare artificial intelligence market has crossed an inflection point. By mid-2026, the global market is estimated at approximately $36.7 billion, expanding at a compound annual growth rate of 38.6%, according to Grand View Research. This is not a single, homogeneous industry. The companies that dominate this space cluster into five distinct categories, each with its own success metrics, regulatory pathways, and adoption curves. Understanding which companies lead within each category — and why — requires more than a flat list of names and funding rounds.

This analysis ranks the top AI healthcare companies of 2026 by category, using concrete data on valuation, revenue, clinical adoption, FDA clearances, and the Bessemer Venture Partners Health AI X Factor framework. The goal is to provide healthcare professionals, health IT decision-makers, and investors with an evidence-based map of where real traction exists — and where it does not.

Category 1: Clinical Documentation & Ambient Scribes — The Fastest-Adopted AI in Healthcare

No category has seen faster clinical adoption than ambient AI scribes. By March 2025, 92% of provider health systems were deploying, implementing, or piloting ambient AI documentation tools, according to Bessemer Venture Partners. The reason is straightforward: these tools address the single most time-consuming task in clinical practice — documentation — and deliver measurable ROI within months.

The category leader is Abridge, which raised a $300 million Series E in June 2025 at a $5.3 billion valuation. The company now generates over $100 million in annual recurring revenue, has deployed across more than 150 health systems, and was named #1 Best in KLAS for Ambient AI in Revenue Cycle Management for two consecutive years. Abridge's deep integration with Epic EHR gives it a structural advantage that competitors have struggled to match.

Key competitors in this space include Nabla (valued at $5.3 billion), Ambience Healthcare ($1.04 billion valuation, 2026 KLAS/CHIME Trailblazer Award winner, deployed enterprise-wide at Houston Methodist), and Suki ($168 million raised to date, announced a partnership with HealthEdge in January 2026 for ambient clinical intelligence in care management).

| Company | Valuation | ARR / Revenue | Health Systems | Key Distinction |

|---|---|---|---|---|

| Abridge | $5.3B | $100M+ ARR | 150+ | #1 Best in KLAS Ambient AI RCM; Epic integration |

| Nabla | $5.3B | Not disclosed | Not disclosed | Strong European presence; real-time ambient scribe |

| Ambience Healthcare | $1.04B | Not disclosed | Enterprise at Houston Methodist | 2026 KLAS/CHIME Trailblazer Award |

| Suki | Not unicorn | $168M raised total | Not disclosed | HealthEdge partnership for care management |

For a deeper dive into Abridge's product, regulatory status, and EHR integrations, see the full Abridge company profile. For details on how ambient AI scribes integrate with Epic EHR in real-world deployments, see the ambient AI scribe deployment report.

Category 2: Medical Imaging & Diagnostics — The Most FDA-Cleared Category

Medical imaging remains the most regulated and most evidence-rich category in healthcare AI. As of May 2025, approximately 1,250 AI/ML-enabled medical devices had been cleared by the FDA, with 76% concentrated in radiology. This regulatory density creates both a barrier to entry and a quality signal: companies with multiple FDA clearances and published clinical evidence have a durable competitive advantage.

The category leader by deployment scale is Aidoc, which has been deployed across more than 1,000 hospitals and holds multiple FDA clearances for its AI-powered triage and notification platform. Aidoc's approach — flagging critical findings on CT scans in real time and integrating directly into radiologist workflows — has made it the most widely adopted radiology AI platform in the United States.

Other major players include PathAI, which received FDA clearance for its AISight digital pathology platform; Viz.ai, whose stroke detection algorithm has become standard of care in many comprehensive stroke centers; Qure.ai, which operates in 90 countries with a focus on tuberculosis and chest X-ray screening in low-resource settings; and Butterfly Network, which combines a handheld ultrasound device with AI-guided image acquisition and interpretation.

| Company | Deployment Scale | FDA Clearances | Primary Use Case | Key Metric |

|---|---|---|---|---|

| Aidoc | 1,000+ hospitals | Multiple | CT triage & notification | Most widely deployed radiology AI in U.S. |

| PathAI | Not disclosed | AISight cleared | Digital pathology | FDA-cleared pathology platform |

| Viz.ai | Comprehensive stroke centers | Multiple | Stroke detection & care coordination | Standard of care in many centers |

| Qure.ai | 90 countries | Multiple | Chest X-ray & TB screening | Global health focus |

| Butterfly Network | Not disclosed | FDA-cleared device | Handheld ultrasound + AI guidance | AI-guided image acquisition |

For a comprehensive overview of the regulatory landscape and clinical evidence gaps in radiology AI, see the FDA-cleared radiology AI landscape article. For profiles of PathAI, Tempus, and Paige AI in computational pathology, see the pathology AI company profiles.

Category 3: Drug Discovery & Precision Medicine — Highest Valuations, Longest Timelines

Drug discovery AI commands the highest valuations in healthcare AI, but it also carries the longest timelines to clinical output. The category is defined by a tension: massive capital investment and sky-high valuations versus a track record of zero approved drugs from AI-native discovery platforms as of mid-2026.

The largest public company in this category is Tempus AI, with a market capitalization ranging from $8.7 billion to $14 billion depending on the trading day. Tempus reported $1.27 billion in revenue in 2025, representing 83% year-over-year growth, and counts 95% of top oncology pharmaceutical companies as partners. The company's platform combines genomic sequencing, clinical data aggregation, and AI-driven analytics to support precision oncology. Tempus stock rose 65% post-IPO, adding $5.7 billion in market cap.

Other notable companies include Recursion Pharmaceuticals, which combines high-throughput cellular imaging with machine learning; Insilico Medicine, which has advanced a novel drug candidate into Phase II trials using its AI platform; and Isomorphic Labs, the DeepMind spinout with an implied valuation of $14-26 billion, though it has not yet brought a drug to clinical trials.

| Company | Valuation / Market Cap | Revenue | Key Metric | Clinical Output |

|---|---|---|---|---|

| Tempus AI | $8.7-14B | $1.27B (2025) | 83% YoY growth; 95% of top oncology pharma | Precision oncology platform; multiple partnerships |

| Recursion | Not disclosed | Not disclosed | High-throughput cellular imaging + ML | Multiple preclinical programs |

| Insilico Medicine | Not disclosed | Not disclosed | Phase II candidate from AI platform | One drug in Phase II trials |

| Isomorphic Labs | $14-26B (implied) | Not disclosed | DeepMind spinout; AlphaFold heritage | No drugs in clinical trials yet |

For detailed profiles of Insilico Medicine, BenevolentAI, and Atomwise (now Numerion Labs), see the AI drug discovery company profiles. For Tempus's digital pathology acquisitions and regulatory status, see the Tempus and PathAI profile.

Category 4: Revenue Cycle & Administrative Automation — Measurable ROI in Months

Revenue cycle management (RCM) and administrative automation represent the category with the most direct, measurable financial ROI. Unlike clinical AI tools that must prove diagnostic accuracy before adoption, RCM AI can demonstrate revenue improvement in the first quarter of deployment. This has driven rapid adoption across health systems of all sizes.

The category leader by scale is Notable, which automates over 1 million daily administrative workflows across 10,000 care sites. Notable has partnered with Inova Health (January 2026) and Marshall Health Network (March 2026) to expand its AI-driven prior authorization, scheduling, and billing automation platform.

Other key players include AKASA, which expanded its partnership with Cleveland Clinic in October 2025 to focus on mid-revenue cycle automation; and CodaMetrix, which was ranked #1 in the 2026 Best in KLAS report for Autonomous Medical Coding. CodaMetrix has raised $110.65 million to date and focuses on AI-powered medical coding that integrates directly with EHR systems.

| Company | Scale | Key Partnership | KLAS Ranking | Funding Raised |

|---|---|---|---|---|

| Notable | 1M+ daily workflows; 10K care sites | Inova Health, Marshall Health Network | Not ranked in coding | Not disclosed |

| AKASA | Not disclosed | Cleveland Clinic (expanded Oct 2025) | Not ranked in coding | Not disclosed |

| CodaMetrix | Not disclosed | Not disclosed | #1 Best in KLAS Autonomous Medical Coding (2026) | $110.65M |

Category 5: AI Patient Agents & Clinical Support — The Newest Category, Fastest Growth

The newest and fastest-growing category in healthcare AI is the emergence of AI-powered patient agents and clinical decision support tools. These systems use large language models and generative AI to interact directly with patients and clinicians, handling tasks ranging from pre-visit questionnaires to post-discharge follow-up to real-time clinical question answering.

The category leader by valuation and physician adoption is OpenEvidence, which reached a $12 billion valuation after a January 2026 funding round. The platform has registered over 760,000 U.S. physicians — more than 75% of the nation's active physician workforce — and handles 18 million clinical consultations per month. On March 10, 2026, OpenEvidence processed 1 million consultations in a single day. The company is notably capital-efficient, achieving a 16.3x valuation multiple on total capital raised. In March 2026, it launched a Coding Intelligence feature to expand into the RCM space.

Another major player is Hippocratic AI, valued at $3.5 billion, which has deployed safety-oriented generative AI agents across 50+ health systems, payors, and pharmaceutical companies in six countries. Hippocratic AI's agents are built in 30 minutes and deployed in 3-4 hours, and the company was named to Forbes America's Best Startup Employers 2026 list in March 2026.

A notable emerging player is Ellipsis Health, which partnered with NVIDIA Riva Parakeet in November 2025 to enhance transcription accuracy for its AI-powered behavioral health screening platform.

| Company | Valuation | Clinical Adoption | Key Metric | Differentiator |

|---|---|---|---|---|

| OpenEvidence | $12B | 760K+ physicians; 18M consults/month | 1M consults in a single day (Mar 10, 2026) | Capital-efficient: 16.3x valuation on capital raised |

| Hippocratic AI | $3.5B | 50+ health systems in 6 countries | Agents built in 30 min, deployed in 3-4 hours | Safety-oriented generative AI agents |

| Ellipsis Health | Not disclosed | Not disclosed | NVIDIA Riva Parakeet partnership | Behavioral health AI screening |

For a broader discussion of AI clinical decision support in primary care, including evidence and deployment realities, see the AI clinical decision support in primary care article.

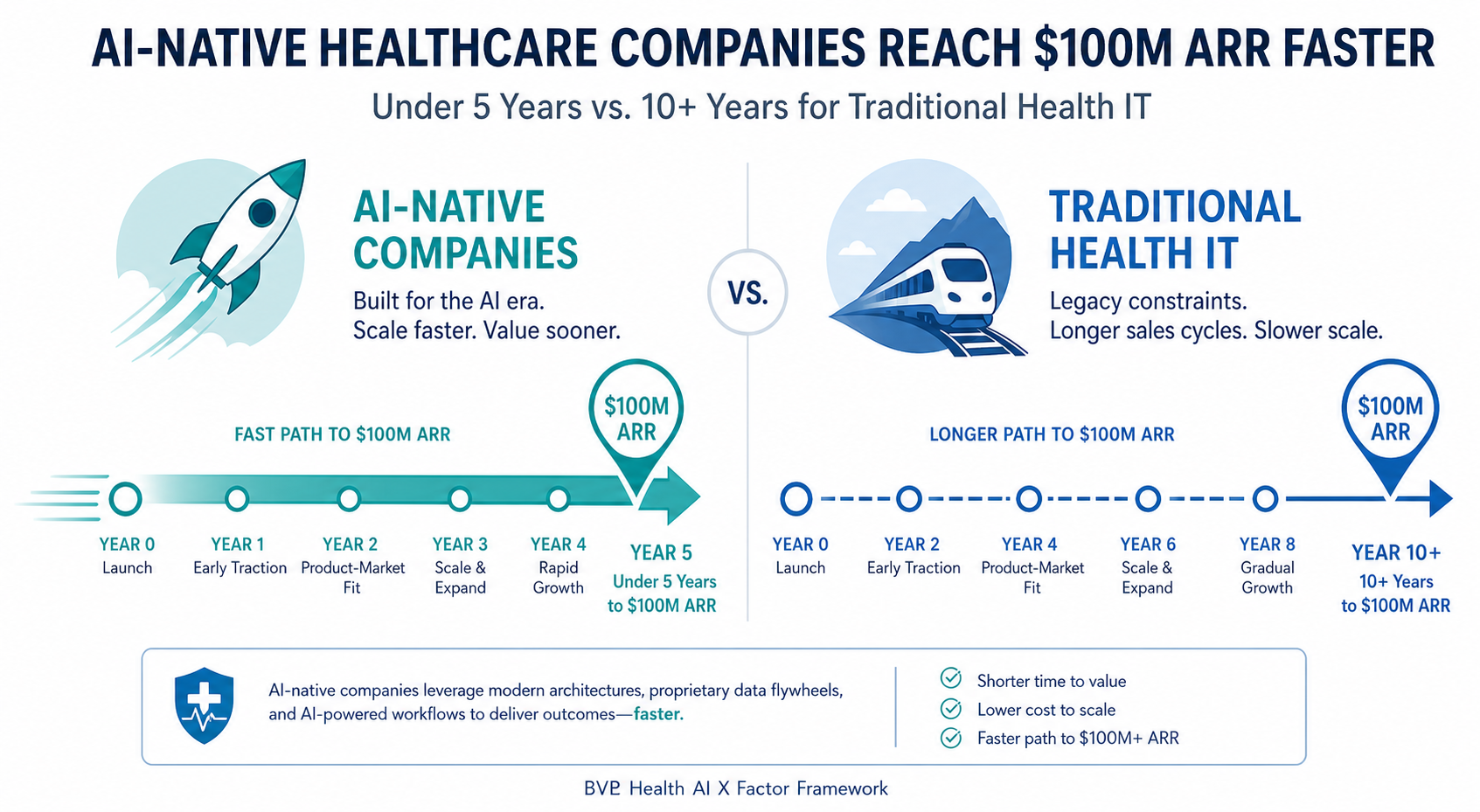

Cross-Cutting Analysis: The BVP Health AI X Factor Framework

Bessemer Venture Partners' Health AI X Factor framework provides a useful lens for comparing companies across categories. The framework identifies four pillars that distinguish AI-native healthcare companies from traditional health IT: hyper-growth velocity, revenue durability, AI-native margins, and point solution to platform expansion.

| X Factor Pillar | AI-Native Companies | Traditional Health IT | Example |

|---|---|---|---|

| Hyper-growth velocity | 6x+ year-over-year revenue growth | ~20% annual growth | Tempus: 83% YoY growth |

| Revenue durability | 120%+ net revenue retention | ~90-100% NRR | Abridge: $100M+ ARR from 150+ health systems |

| AI-native margins | $500K-$1M+ ARR per FTE | $200-400K ARR per FTE | OpenEvidence: 16.3x valuation on capital raised |

| Point solution to platform | Expanding from single use case to platform | Stays within category | Notable: from prior auth to full RCM platform |

The aggregate market data supports this framework. AI companies captured 55-62% of all digital health funding in 2025, up from 29% in 2022. Venture capital investment into health AI reached approximately $14 billion in 2025, with 33 healthcare AI startups valued at $1 billion or more. Series D+ valuations jumped 63% from 2024, and 400 M&A deals were completed in 2025, up from 350 in 2024, with average deal size increasing 42% to $29.3 million.

For a broader context on how AI is reshaping clinical workflows across all specialties, see the AI in medicine clinical workflow overview.

Selection Methodology, Caveats, and 2026–2027 Outlook

The companies featured in this analysis were selected based on a combination of valuation, revenue, clinical adoption metrics, FDA clearances, and category leadership. The goal was to identify the most significant players in each of the five categories, not to produce an exhaustive list. Companies like Qure.ai, which is dominant in global health but underweighted in US-centric rankings, were included to provide geographic balance.

- Valuation figures for private companies (Isomorphic Labs $14-26B, OpenEvidence $12B, Abridge $5.0-5.6B) vary across sources and should be treated as estimates. Ranges are provided where available.

- Market size projections vary significantly by analyst firm ($36.7B Grand View Research vs. $56B Fortune Business Insights for 2026). Methodology and scope differences should be noted.

- Some company metrics (e.g., '92% of health systems deploying AI scribes') come from single-source surveys or venture research. Cross-verification is recommended for high-stakes procurement decisions.

- The 'top' companies are context-dependent. Companies like Qure.ai are dominant in global health but underweighted in US-centric lists. Readers should assess relevance to their specific needs.

- Several companies in the drug discovery category have very high valuations but minimal or no approved drugs yet. Valuation reflects potential, not clinical output.

- Company status (public/private, valuation, revenue) changes rapidly. All data reflects publicly available information as of mid-June 2026 and may be outdated within weeks.

Looking ahead to 2026-2027, several trends will shape the competitive landscape. The 400 M&A deals in 2025 and the 63% jump in Series D+ valuations suggest that consolidation is accelerating. AI-native companies that can demonstrate the BVP X Factor — hyper-growth, durable revenue, AI-native margins, and platform expansion — will continue to attract the majority of capital. Companies that fail to move beyond single-use-case point solutions will face acquisition pressure or obsolescence.

The five categories will also converge. Abridge is expanding from ambient documentation into clinical decision support. OpenEvidence has launched Coding Intelligence to enter the RCM space. Tempus is acquiring digital pathology companies to bridge diagnostics and drug discovery. The winners of 2027 may not be the same companies that lead their categories today — but the categories themselves will persist, each with its own metrics of success.