The healthcare AI market in 2026 is not a single battlefield. It is three overlapping wars fought on different terrain: AI-native startups racing to embed themselves in clinical workflows, incumbent EHR vendors defending their installed bases with built-in AI modules, and big tech platform companies supplying the infrastructure that both sides depend on. Understanding who is winning — and where — requires looking past aggregate market size figures and examining the specific segments where customer preferences, deployment scale, and capital allocation reveal the actual balance of power.

This article draws on the Menlo Ventures 2025 survey of 700+ healthcare executives, the NVIDIA 2026 State of AI in Healthcare and Life Sciences survey, market sizing from Fortune Business Insights and Precedence Research, and deployment data from Philips and the FDA clearance database to build a competitive-intelligence view of the market. It is structured as a strategic analysis for product leaders, investors, and health system innovation officers — not a general market overview.

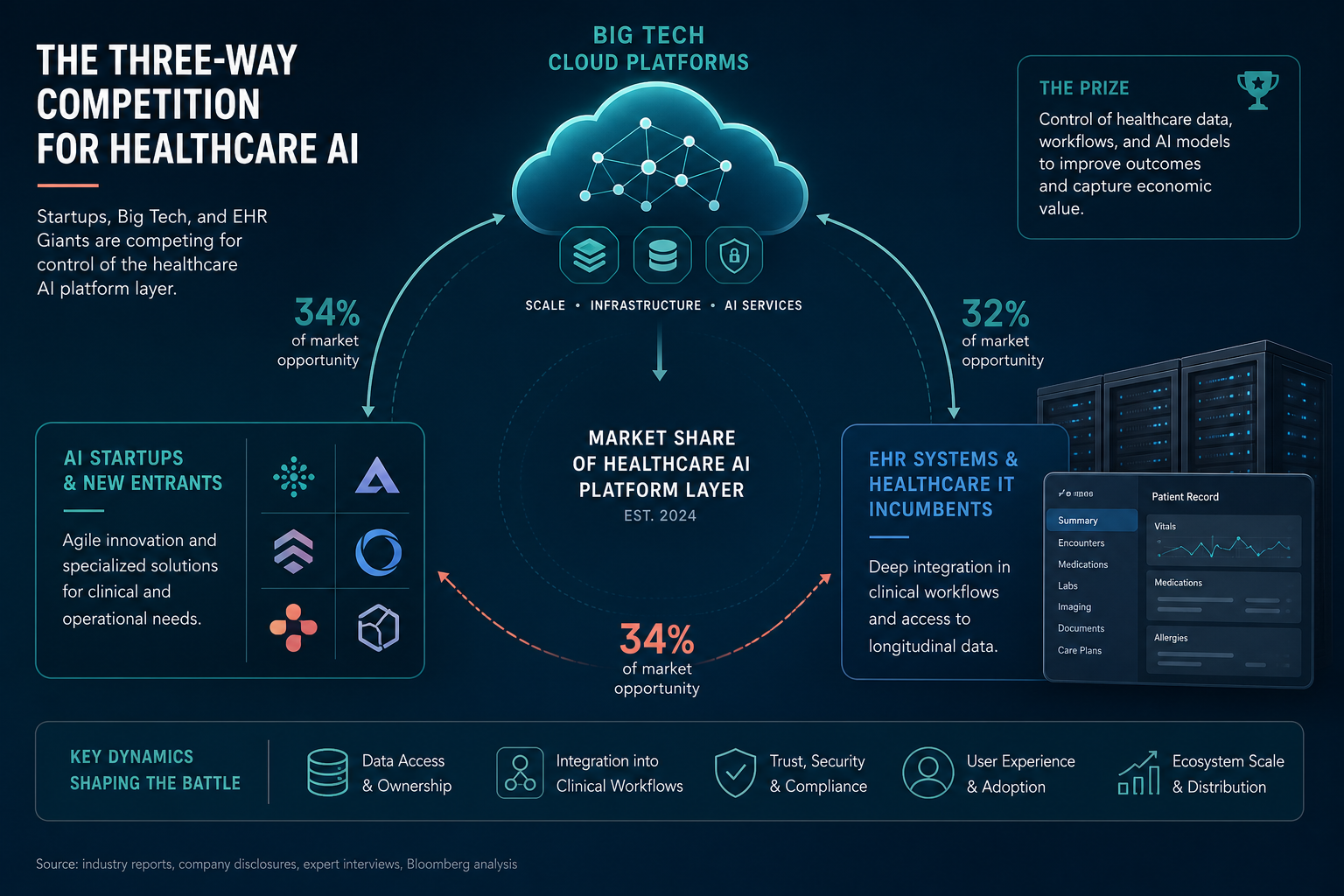

Market Structure: $1.4B in Healthcare AI Spend and the Startup Advantage

Healthcare AI spending reached $1.4 billion in 2025, nearly tripling from 2024, according to the Menlo Ventures survey fielded August–September 2025. Providers accounted for 75% of that total — roughly $1.05 billion — making health systems the dominant customer segment by a wide margin. The remaining spend came from payers, pharmaceutical companies, and life sciences organizations.

The most striking structural finding: 85% of healthcare generative AI spend flows to startups rather than incumbent technology vendors. This is not a marginal preference — it is a near-total capture of a rapidly expanding market by companies that did not exist a decade ago. The top two spend categories alone — ambient clinical documentation ($600 million) and coding and billing automation ($450 million) — account for $1.05 billion of the $1.4 billion total, and startups dominate both.

The broader market size context helps frame the opportunity. Fortune Business Insights valued the global AI in healthcare market at $39.34 billion in 2025, projecting growth to $56.01 billion in 2026 and $1,033.27 billion by 2034 (CAGR of 43.96%). Precedence Research offers a slightly lower estimate of $36.96 billion for 2025, rising to $51.20 billion in 2026 and $744.34 billion by 2035 (CAGR of 35.02%). The variance reflects differences in scope definition — what counts as "AI" and whether hardware is included — but both point to the same conclusion: the market is expanding at a pace that creates room for multiple player types to coexist, at least for now.

The Startup Wave: Eight Unicorns and the Dominance of Ambient Scribing

The startup cohort in healthcare AI has produced eight unicorns — more than any other vertical AI segment including legal, financial services, and media. These companies have not simply raised capital; they have achieved real clinical deployment at scale, which is the hardest validation in healthcare technology.

The ambient clinical documentation category illustrates the pattern most clearly. Abridge holds 30% of the ambient scribe market and executed the largest generative AI rollout in healthcare history: deployment across 40 hospitals and 600+ medical offices in the Kaiser Permanente system. Ambience holds 13% market share. Together, these two startups control 43% of a $600 million spend category that barely existed three years ago.

Other notable startups in the unicorn cohort include:

- OpenEvidence — clinical information retrieval and synthesis platform used by clinicians for evidence-based decision support.

- Hippocratic AI — patient engagement and pre-visit automation, targeting the staffing shortage in non-clinical patient communication.

- Several additional companies in coding automation, revenue cycle management, and clinical decision support that have reached unicorn valuation but have not disclosed market share data publicly.

These startups are not standing still. Having established beachheads in documentation and clinical information retrieval, they are expanding into adjacent workflows: coding and billing automation, prior authorization, clinical decision support, and patient navigation. The NLP in Clinical Documentation: AI Scribes, Coding, and Clinical Documentation Improvement glossary entry provides technical context for how these expansions are built on the same natural language processing foundations.

The broader context of generative AI performance and governance concerns is covered in the site's Generative AI and Health: What the Clinical Evidence Actually Shows in 2026 research evidence entry, which should be consulted alongside any competitive analysis that assumes generative AI reliability in clinical settings.

The Incumbent Response: Epic, Oracle, and the EHR Counteroffensive

EHR vendors are not ceding the AI market to startups. After a period of apparent inaction during 2023–2024, the major electronic health record platforms have launched a coordinated counteroffensive built on their deepest strategic asset: existing workflow integration.

Epic has introduced a built-in ambient scribe capability that runs directly within its existing charting workflows. The strategic logic is straightforward: a clinician using Epic does not need to context-switch to a separate startup application, manage a second login, or worry about data integration between systems. The scribe is simply there, inside the workflow the clinician already uses. The trade-off is that Epic's scribe may not match the accuracy or specialty-specific tuning of dedicated startup products — but for many health systems, the integration advantage outweighs the performance gap.

Oracle Health (formerly Cerner) launched its AI-powered EHR in August 2025, embedding generative AI capabilities directly into the clinical record. The product represents a bet that a full-stack AI-native EHR can leapfrog both legacy systems and point-solution startups by offering an integrated experience that neither can match.

athenahealth has taken a modular approach, adding AI capabilities to specific workflows — coding assistance, prior authorization automation, and clinical note generation — without requiring a full platform migration. This allows them to compete with startups on a feature-by-feature basis while retaining the advantage of existing customer relationships.

The most complex incumbent player is Nuance DAX Copilot, now part of Microsoft. With 33% ambient scribe market share — the largest single share in the category — Nuance occupies a hybrid position. It is an incumbent product with deep EHR integrations (including Epic), but it is also a big tech platform play through Microsoft's cloud and AI infrastructure. The Microsoft Dragon Copilot (Nuance DAX Copilot): Platform Profile for Enterprise Ambient AI Clinical Documentation profile provides detailed context on its deployment architecture and competitive positioning.

| Player | Type | Ambient Scribe Share | Key Strategic Asset | Key Vulnerability |

|---|---|---|---|---|

| Abridge | AI-native startup | 30% | Best-in-class accuracy, Kaiser deployment | Narrow product scope, no EHR lock-in |

| Ambience | AI-native startup | 13% | Specialty-specific tuning | Smaller scale, less brand recognition |

| Nuance DAX Copilot | Big tech / incumbent hybrid | 33% | Deep EHR integrations, Microsoft infrastructure | Legacy product perception, slower iteration |

| Epic (built-in scribe) | EHR incumbent | Not disclosed | Native workflow integration, no context switch | May trail startups on accuracy and specialty coverage |

| Oracle Health AI EHR | EHR incumbent | N/A (full platform) | Full-stack AI-native EHR | Requires platform migration, unproven at scale |

Big Tech Platform Plays: Microsoft, NVIDIA, and Google

Big technology companies compete in healthcare AI primarily at the platform layer, supplying the infrastructure, models, and cloud services that both startups and incumbents depend on. Their strategic position is both powerful and constrained: they enable the entire ecosystem but rarely own the clinical relationship directly.

Microsoft's healthcare AI strategy centers on three assets: Nuance DAX Copilot for ambient documentation, Azure AI for Healthcare for model deployment and compliance, and the Cloud for Healthcare program that provides infrastructure and go-to-market support for healthcare AI companies. Microsoft's advantage is breadth — it can offer a startup both the platform to run its models and a distribution channel through Nuance's existing health system relationships.

NVIDIA plays a different role. Its Clara platform provides the GPU infrastructure, pretrained models, and application frameworks that healthcare AI companies use to build and deploy their products. NVIDIA does not compete directly with its customers — it supplies the picks and shovels. The company's annual survey data is widely cited as evidence of AI adoption and ROI in healthcare, though it should be noted that the survey is vendor-commissioned.

Google's Vertex AI for Healthcare offers a managed machine learning platform with healthcare-specific features including FHIR data integration, medical imaging APIs, and compliance certifications. Google has also invested in partnerships with health systems and AI startups, positioning Vertex as the infrastructure layer for organizations that want to build or customize their own AI applications rather than buying off-the-shelf products.

- Microsoft: Nuance DAX Copilot (33% ambient scribe share), Azure AI for Healthcare, Cloud for Healthcare program.

- NVIDIA: Clara platform (GPU infrastructure, pretrained models, application frameworks), annual State of AI in Healthcare survey.

- Google: Vertex AI for Healthcare (managed ML platform with FHIR integration, medical imaging APIs, compliance certifications).

The platform-layer dynamic creates an unusual competitive structure: big tech companies compete with each other for enterprise AI budgets while simultaneously supplying the infrastructure that their customers' competitors use. A startup building on NVIDIA Clara or Google Vertex AI may find itself competing for the same health system contract as Microsoft's Nuance DAX Copilot — but also relying on Microsoft Azure for cloud compute.

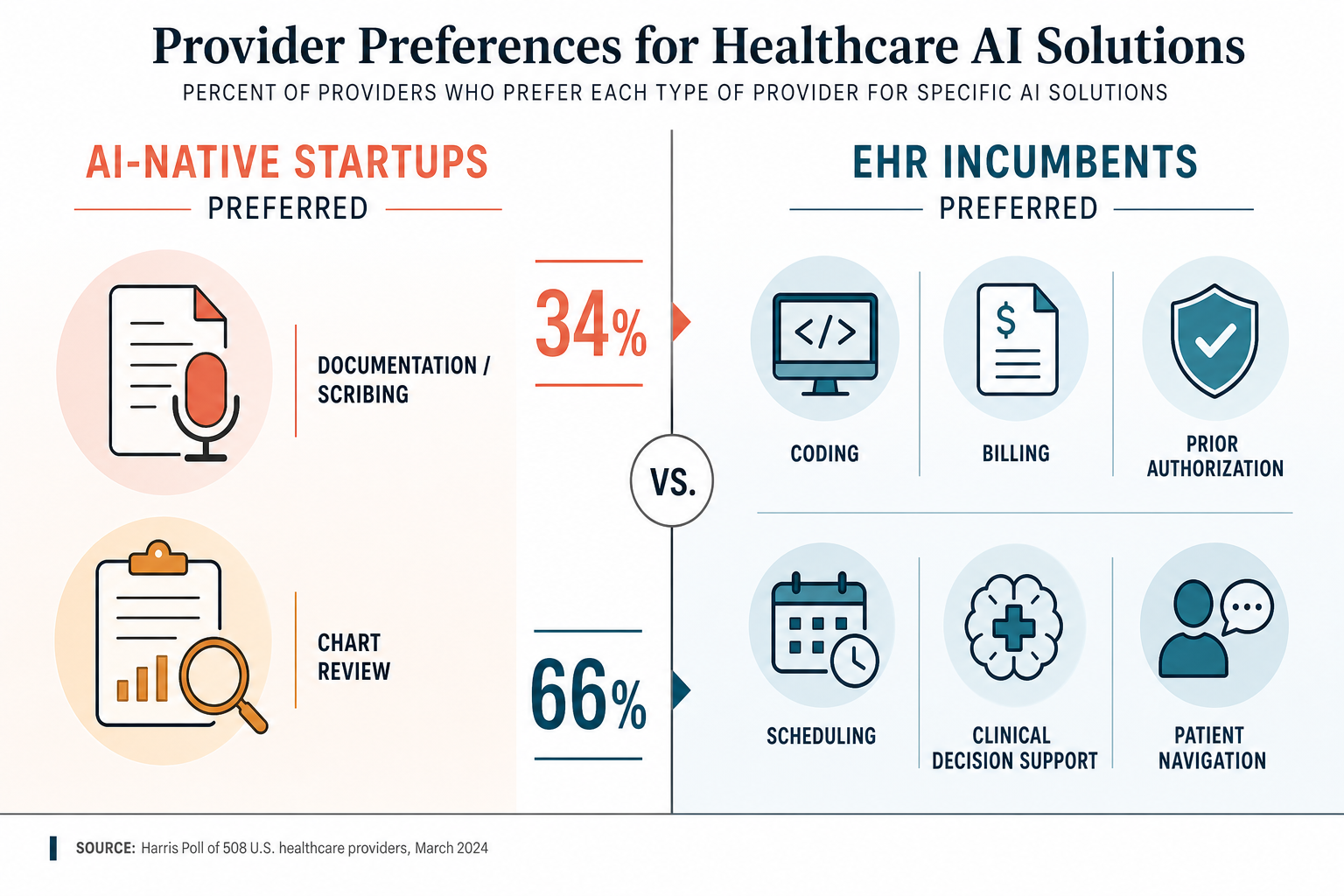

Where Customer Preferences Reveal Fault Lines

The Menlo Ventures survey provides the most granular view available of where providers prefer startups versus incumbent EHR vendors. The data reveals a sharp split that defines the competitive landscape:

| Use Case | Preferred Vendor Type | Implication |

|---|---|---|

| Clinical documentation / ambient scribing | AI-native startups | Startups have established beachhead in the largest spend category ($600M) |

| Chart review / clinical information retrieval | AI-native startups | OpenEvidence and similar tools have strong clinician adoption |

| Medical coding and billing | EHR incumbents | Startups face uphill battle displacing embedded coding workflows |

| Prior authorization | EHR incumbents | Integration with existing revenue cycle systems is critical |

| Scheduling | EHR incumbents | Low willingness to add standalone scheduling AI tools |

| Clinical decision support (CDS) | EHR incumbents | CDS must be deeply integrated into order entry and results review |

| Patient navigation / engagement | EHR incumbents | Patient portals and communication tools are already part of the EHR stack |

The pattern is clear: startups win where the task is narrowly defined, the workflow is relatively new (ambient scribing did not exist before 2022), and the value proposition is a dramatic improvement over manual processes. EHR incumbents win where the task is deeply embedded in existing systems, the switching cost is high, and the AI capability is an enhancement to an existing workflow rather than a replacement.

This split has strategic implications. Startups that want to expand beyond documentation and chart review into coding, billing, prior authorization, and CDS will need to either partner with EHR vendors (ceding some control and margin) or build their own integration layer (requiring significant engineering investment and health system buy-in). EHR vendors that want to capture the documentation and clinical information market will need to match startup-level accuracy and user experience — which is harder than it sounds, given that startup products are often built by teams with deep clinical NLP expertise.

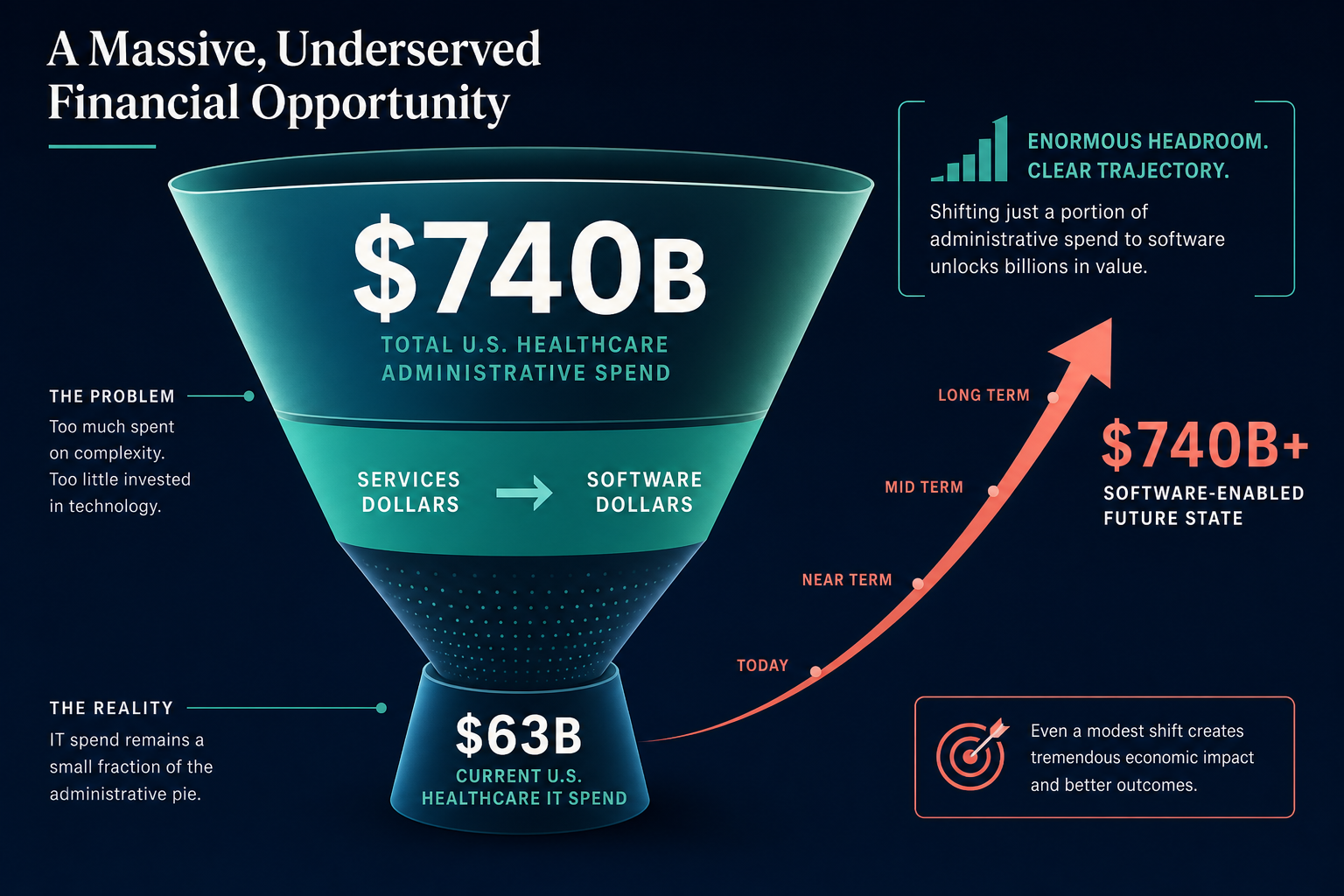

The $740B Administrative Spend Opportunity

The core growth thesis for healthcare AI is not about clinical replacement — it is about converting administrative services dollars into software dollars. U.S. healthcare administrative spending totals $740 billion annually, according to industry estimates cited in the Menlo Ventures analysis. Of that, healthcare IT captures only $63 billion. The gap — $677 billion — represents the addressable market for AI-driven automation of administrative tasks.

The $450 million coding and billing automation spend category is the leading indicator of this conversion. Coding and billing are currently labor-intensive processes that consume a significant portion of the $740 billion administrative total. AI tools that can automate code assignment, claims generation, and denial management convert what is currently a services cost into a software subscription — with higher margins, greater scalability, and faster iteration cycles.

The same logic applies across the administrative stack: prior authorization, scheduling, revenue cycle management, patient communication, and compliance documentation. Each of these categories currently employs large teams of human workers. AI that can perform these tasks at comparable or better accuracy, with lower cost and higher throughput, represents a direct conversion of services spend to software spend.

The Ambient Clinical Intelligence: Beyond Scribing to Decision Support clinical application entry explores how the same ambient AI technology that captures clinical documentation is being extended into decision support and workflow automation — a direct example of the services-to-software conversion in action.

Investment Landscape: Pharma Builds, Payers Lag

The investment dynamics across healthcare AI reveal a fragmented landscape where different sub-sectors are at very different stages of maturity.

Pharmaceutical companies are the most aggressive builders: 66% are developing or fine-tuning proprietary AI models, according to the Menlo Ventures survey. This reflects the high value of drug discovery and clinical trial optimization, where even modest improvements in success rates translate into billions of dollars. Pharma companies have the data, the budget, and the regulatory experience to build internal AI capabilities rather than relying entirely on external vendors.

Payer-side AI adoption, by contrast, remains nascent. Health insurers have been slower to deploy generative AI tools, partly due to regulatory complexity (prior authorization and claims processing are heavily regulated) and partly due to legacy system constraints. This represents a significant opportunity for startups and platform vendors, but also a longer sales cycle and higher implementation risk.

The ROI picture is encouraging but should be interpreted with caution. The Menlo Ventures survey reports an average 3.2:1 return on healthcare AI investments with a 12–18 month payback period. The NVIDIA survey found that 85% of executives say AI is helping increase revenue, and 80% say it is helping reduce costs. However, both surveys are vendor-commissioned and may carry selection bias toward AI-positive findings.

- 66% of pharmaceutical companies are building or fine-tuning proprietary AI models (Menlo Ventures).

- 85% of healthcare executives say AI is helping increase revenue (NVIDIA survey).

- 80% of executives say AI is helping reduce costs (NVIDIA survey).

- 70% of organizations are actively using AI, up from 63% in 2024 (NVIDIA survey).

- 69% are using generative AI and LLMs, up from 54% in 2024 (NVIDIA survey).

- Average ROI of 3.2:1 with 12–18 month payback period (Menlo Ventures, citing industry compilations).

- 22% of healthcare organizations have implemented domain-specific AI tools, a 7x increase over 2024 (Menlo Ventures).

The Philips 2026 emerging trends report adds a qualitative dimension: agentic AI — systems that can autonomously execute multi-step clinical workflows — is predicted to move into the spotlight in 2026, with the UK's NHS launching a project focused on responsible deployment. Mount Sinai and Mayo Clinic are already using AI agents to streamline workflows. Interest in AI agents is predicted to increase rapidly, particularly in Asia, Australia, and Europe. This trend could reshape the competitive dynamics described above, because agentic AI requires deeper workflow integration than current point solutions — potentially favoring EHR incumbents and platform providers over standalone startups.

The competitive landscape of healthcare AI in 2026 is not a winner-take-all market. It is a three-way contest where each player type has distinct advantages and vulnerabilities. Startups have the innovation velocity and category-defining products. EHR incumbents have the workflow integration and customer relationships. Big tech platforms have the infrastructure and capital. The next phase of the market will be defined not by which type wins, but by how the boundaries between them shift — through acquisition, platform expansion, or the emergence of agentic AI that rewrites the rules entirely.