Searching for AI clinical trials companies usually starts with the wrong question. The useful question is not which vendor has the broadest AI story; it is which delay, failure mode, or workload the technology is supposed to change. A sponsor behind on enrollment has a different buying problem from a team trying to pressure-test a protocol, rescue site performance, clean multimodal data, or monitor safety signals after launch.

That distinction matters because the market now mixes full clinical technology suites, narrow matching engines, simulation platforms, imaging and pathology AI companies, decentralized trial operators, and safety-monitoring tools under the same label. They may all belong in the AI-in-clinical-trials conversation. They do not all belong in the same procurement comparison.

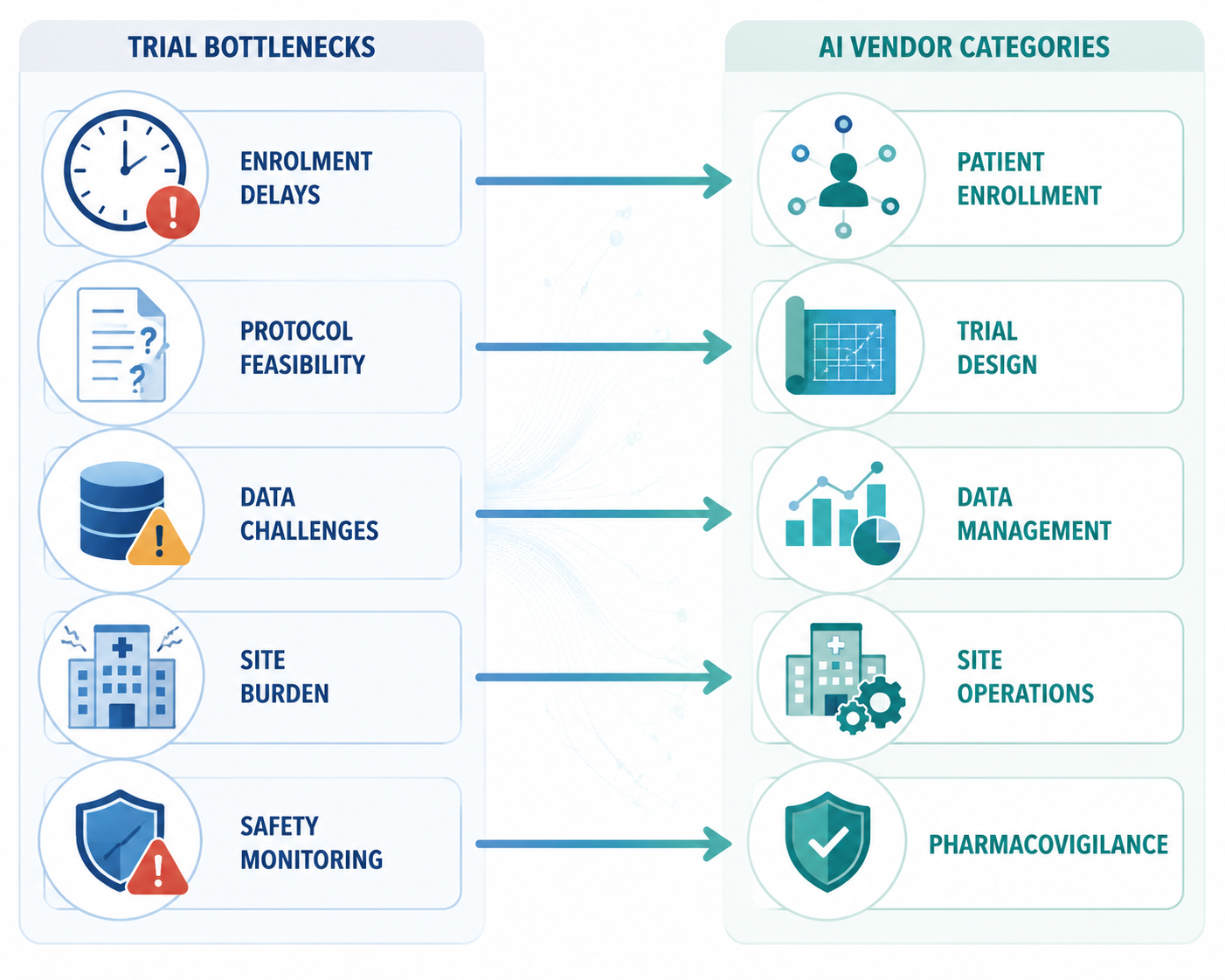

The Five Buying Categories

For an executive review, the cleanest first cut is functional. Most AI clinical trials companies fit primarily into one of five categories, even when their marketing language reaches beyond it.

| Primary bottleneck | AI vendor category | Typical buyer question | Example companies |

|---|---|---|---|

| Enrollment is late or screening is too manual | Patient enrollment and matching | Can we find eligible patients faster and reduce chart-review burden? | Deep6.ai, Antidote, BEKhealth, Viz.ai, Trially, AiCure, IQVIA |

| Protocol feasibility is weak or assumptions are uncertain | Trial design and simulation | Can we test eligibility criteria, control-arm assumptions, or trial scenarios before execution? | Unlearn.ai, Altis Labs, Phesi, Saama |

| Evidence generation, data quality, or analysis is the constraint | Data management and analytics | Can we integrate, curate, analyze, or interpret complex trial and real-world data? | Medidata Acorn AI, IQVIA, ConcertAI, PathAI, Owkin |

| Sites are overburdened or trial operations are fragmented | Site and operational enablement | Can we reduce friction for sites and participants across hybrid or decentralized workflows? | Curebase, Vial, Merative/Zelta |

| Safety case processing or signal detection needs scale | Pharmacovigilance | Can we support adverse-event intake, triage, monitoring, or safety analytics? | Multiple emerging AI safety and pharmacovigilance vendors |

The market is attracting enough budget attention that this map is no longer academic. Research and Markets projected the AI-in-clinical-trials market at $2.09 billion in 2026, reaching $18.62 billion by 2040 at a 17% CAGR, while Beroe estimated a $2.7 billion market in 2025 growing at 24–28% CAGR to $8.5 billion by 2030.[1][2] Those numbers should not be read as interchangeable. They define the market differently, and market size is not evidence that a particular vendor can fix a particular trial.

The adoption signals are still useful. Beroe expected AI to be used in 60–70% of clinical trials by 2030 and estimated potential annual pharma savings of $20–30 billion; the same market discussion cited roughly $59.3 billion in cumulative funding among leading AI-driven pharma companies as of December 2022 and a 30% rise in pharma-tech AI partnerships from 2022 to 2024.[2] Those are maturity signals, not vendor rankings.

Patient Enrollment Is Crowded Because the Pain Is Measurable

Enrollment is the category that most often pulls AI into clinical operations conversations because the failure mode is visible early and blamed late. The operating pressure is familiar: 80% of trials fail to meet enrollment timelines. Published-study results cited in this market discussion found that AI reduced screening time by 34% and improved enrollment by 11.1%, alongside an IQVIA-reported 20% increase. Those figures are more useful than a generic claim that AI “accelerates trials” because they point to specific operational levers: screening time and enrollment yield.

This is also where evidence quality needs to be separated from sales language. A peer-cited 11.1% enrollment improvement and a reported 20% increase do not mean every matching product will produce that lift in every protocol. A looser industry claim of enrollment improvement as high as 65% should be treated as a claim to investigate, not as a procurement assumption, when the underlying study design, comparator, and trial context are not visible.

Deep6.ai is a useful example of why this category is not just “recruitment marketing.” Its genomics module, launched in September 2023, uses AI to mine electronic medical records and genetic reports for precision matching. That is a different workflow from patient-facing trial awareness, referral management, or decentralized patient engagement. A sponsor running an oncology study with biomarker-heavy eligibility criteria may care more about structured and unstructured record mining than broad outreach.

Antidote, BEKhealth, Viz.ai, Trially, AiCure, and IQVIA sit near this part of the map, but they should not be treated as identical options. Some tools emphasize eligibility matching against clinical records. Some work closer to patient identification and referral pathways. Some overlap with engagement, adherence, or decentralized trial execution. The procurement question should be written before the vendor list is built: are we trying to reduce manual pre-screening, widen the eligible patient pool, improve referral velocity, support adherence, or forecast enrollment more accurately?

The same distinction changes implementation risk. An EMR-mining tool may need health-system data access, site trust, privacy review, and integration with screening workflows. A patient-facing matching tool may depend more on outreach strategy, consent flow, and referral handoff. A sponsor can buy the right-sounding category and still miss enrollment if the tool does not touch the actual delay between identifying a potentially eligible patient and getting that patient randomized.

Trial Design and Simulation Vendors Belong in a Different Conversation

Unlearn.ai, Altis Labs, Phesi, and Saama are often grouped into AI clinical trials lists, but they should not automatically be compared with enrollment vendors. Their stronger fit is earlier in the operating model: trial design, feasibility, simulation, synthetic or external control work, patient-population modeling, and protocol assumption testing.

The distinction is practical. If the protocol excludes too many real-world patients, a matching engine may only reveal the problem faster. If the control-arm assumption is weak, recruitment technology will not fix the analysis plan. If eligibility criteria are operationally unworkable across regions, the bottleneck is design discipline before it is site activation.

Available market summaries place Unlearn.ai at $84.9 million raised and Saama at more than $500 million raised, while Phesi’s Trial Accelerator Platform is described as drawing on more than 100 million patient profiles across 4,000 indications.[3] Those figures signal that this is a serious vendor segment, but they still do not answer the buyer’s harder question: does the model help with the exact trial decision now on the table?

For trial design and simulation, the evaluation should be tied to a decision that can change before the protocol hardens. That may be whether to modify an inclusion criterion, adjust visit burden, assess a digital twin or external-control approach, or compare feasibility across study designs. The vendor’s value is not that it uses AI; the value is that it changes a design choice early enough to avoid months of operational drag.

Data Management and Analytics: Stronger Fit When the Problem Is Evidence, Not Enrollment

Medidata Acorn AI, IQVIA, ConcertAI, PathAI, and Owkin sit in a broader evidence and analytics lane. They may influence trial execution, but they are often most relevant when the bottleneck involves data integration, endpoint interpretation, imaging or pathology workflows, real-world data, model-assisted analysis, or evidence generation across trials and care settings.

This is where broad platform suites can have a real advantage, especially in large, complex, multi-country studies where the sponsor already runs core trial operations through established systems. Medidata and IQVIA can be attractive not simply because they are recognizable names, but because data, workflow, analytics, and services may already sit close together. That proximity can reduce some integration burden, although it can also narrow flexibility if the sponsor needs a very specific model or analytic method.

Specialists still matter. ConcertAI is listed in the source material at $300 million raised, PathAI at $255 million, and Owkin at $304 million; Owkin also received an EMA letter of support for its MesoNet and HCCnet models in May 2023.[3] Funding does not validate model performance, and a regulatory letter of support is not the same as universal acceptance for every use case. But these details help distinguish mature analytics companies from thin AI wrappers around ordinary dashboards.

In this category, buyers should ask what data the model was trained on, what population it generalizes to, how missingness is handled, whether the output is used for exploratory analysis or decision-making, and what documentation exists for audit and regulatory review. A pathology AI company, a real-world oncology data company, and an enterprise clinical data platform may all support evidence generation. They do not carry the same validation burden or implementation path.

Site and Operational Enablement Is Where AI Has to Respect the Site

Site enablement deserves its own category because many trial delays are created by fragmented work rather than a lack of analytics. A site may be asked to run another portal, reconcile another dataset, explain another participant-facing tool, and support another sponsor process without extra staff. AI that looks impressive in a central operations dashboard can still fail if it adds work at the coordinator desk.

Curebase and Vial are better understood in this operational lane than as pure recruitment or analytics vendors. Merative/Zelta also belongs in the operational technology discussion; Merative’s February 2026 clinical trial trends analysis described movement toward a continuous trials model.[4] That kind of framing matters for hybrid and decentralized studies, where scheduling, consent, remote data capture, monitoring, and participant communication can become the trial’s practical constraint.

The vendor review should therefore include a site-burden test. Which steps disappear for coordinators? Which steps move from site staff to automation or centralized support? Which alerts are actionable, and which merely create another queue? Who owns exceptions? If the product reduces sponsor oversight work by shifting cleanup to sites, it has not solved the operational problem.

Pharmacovigilance Is Emerging, but the Evidence Is Thinner

Pharmacovigilance belongs on the map because safety case processing, adverse-event intake, signal detection, and literature monitoring are natural candidates for AI-assisted triage and pattern recognition. It should not, however, be inflated into the best-evidenced trial-execution category based on the evidence cited here.

For buyers, the key distinction is whether the tool supports safety operations around a clinical trial, post-market surveillance, or both. Safety workflows carry a different tolerance for missed signals, false reassurance, and undocumented model behavior. A pharmacovigilance AI vendor should be evaluated through safety governance, validation, auditability, and human review requirements before it is treated as an ordinary productivity tool.

How the Same Buyer Question Changes by Bottleneck

A useful shortlist starts with the sentence the clinical team can defend in a governance meeting. “We need AI for trials” is too vague. “We are losing weeks to manual chart review before pre-screening” points toward patient matching. “Our eligibility criteria may be suppressing feasibility” points toward design simulation. “Our endpoint interpretation depends on complex images or pathology data” points toward analytics specialists. “Sites are drowning in operational tasks” points toward enablement.

| If the bottleneck is... | Prioritize vendors that can show... | Be cautious about... |

|---|---|---|

| Late enrollment | Reduced screening time, better eligible-patient identification, clear referral workflow | Broad claims about recruitment without site-level workflow detail |

| Weak feasibility or protocol design | Simulation outputs that can change criteria, sample assumptions, or design choices | Tools positioned as recruitment solutions when the protocol itself is the constraint |

| Data complexity or endpoint interpretation | Validated analytic methods, data provenance, model documentation, human review | Funding totals used as a proxy for model fitness |

| Site burden | Fewer site tasks, fewer portals, better exception handling, lower coordinator workload | Sponsor-facing automation that pushes work downstream |

| Safety monitoring | Audit trails, human oversight, safety validation, clear escalation logic | Black-box triage in regulated safety workflows |

This is also where the platform-versus-point-solution decision becomes more disciplined. A broad suite may be proportionate for a global Phase 3 program that needs enrollment analytics, data operations, monitoring, and reporting in one operating environment. A point solution may be better for a sharply defined bottleneck, such as identifying genomically eligible patients, simulating a control arm, or applying AI to pathology review. Neither architecture is inherently superior. The wrong architecture is the one that forces the trial team to reorganize around a problem they do not have.

Regulatory Credibility Now Belongs in Vendor Selection

AI vendor selection in clinical trials can no longer stop at demos, integrations, and commercial references. Regulators have moved far enough into AI governance that buyers should expect vendors to explain how their models are documented, validated, monitored, and controlled.

FDA’s January 2025 draft guidance on using AI to support regulatory decision-making for drugs and biological products set out a seven-step credibility assessment framework for AI models.[5] The guidance is still draft, so it should not be treated as final policy. It is still highly relevant to procurement because it shows the kinds of questions sponsors should be prepared to answer when AI outputs influence decisions submitted to, or discussed with, regulators.

In January 2026, FDA and EMA jointly published 10 Guiding Principles of Good AI Practice in Drug Development, and FDA’s CDER site also notes that CDER established an internal AI Council in 2024 to support consistent AI regulatory oversight.[6] In April 2026, FDA launched an AI-Enabled Optimization of Early-Phase Clinical Trials Pilot Program through a request for information.[7] Together, these actions do not make every AI trial tool regulator-ready. They do make regulatory posture a procurement criterion rather than an afterthought.

The practical vendor questions are direct: what is the model’s intended use in the trial, and what decisions does it influence? What validation evidence exists for that use? Has the model changed since validation, and how are changes controlled? Can the vendor explain performance across relevant populations, sites, and data sources? Is there a human review step where one is clinically or operationally necessary? Can the sponsor retain enough documentation to support inspection, submission, or internal quality review?

Reporting standards are also part of the conversation. When a vendor claims clinical-trial relevance, buyers should ask whether its validation evidence can be described consistently with established AI trial reporting expectations such as the CONSORT-AI Reporting Standard for AI in Clinical Trials. A tool used only for operational triage will not need the same evidence package as a model used to support endpoint interpretation, but both should have a clear intended use and a defensible validation story.

A Practical Way to Shortlist AI Clinical Trials Companies

The first filter should be the trial bottleneck, not the vendor logo. If the sponsor cannot name the delay or risk the vendor is meant to reduce, the shortlist is premature.

- For enrollment delays, compare patient identification, screening, referral, and engagement workflows separately before grouping vendors together.

- For protocol feasibility, look for simulation, external-data, or digital-twin capabilities that can change design decisions before execution.

- For analytics-heavy studies, evaluate data provenance, validation evidence, endpoint relevance, and regulatory documentation.

- For site operations, require evidence that the tool removes work from sites rather than creating another sponsor-facing dashboard.

- For safety workflows, prioritize auditability, human oversight, escalation logic, and quality-system fit.

AI clinical trials companies have matured into a structured ecosystem, but maturity does not remove the buyer’s job. Locate the bottleneck first. Decide whether a broad suite or specialized point solution is proportionate to that problem. Then verify the vendor’s evidence, integration burden, and regulatory posture before procurement moves forward.

References

- AI in Clinical Trials Market Research 2026: Market to Reach $18.62 Billion by 2040, with IQVIA, Medidata, IBM Watson, Oracle and Phesi Leading Through Integrated Data and Patient Matching, GlobeNewswire, March 2, 2026.

- Global AI in Clinical Trials Market Trends & Current Partnerships, Clinical Leader, February 2025.

- Top Companies Transforming Clinical Trials with AI, Expert Market Research.

- Clinical trial trends 2026, Merative, February 2026.

- Considerations for the Use of Artificial Intelligence to Support Regulatory Decision-Making for Drug and Biological Products, U.S. Food and Drug Administration, January 2025.

- Artificial Intelligence in Drug Development, U.S. Food and Drug Administration.

- AI-Enabled Optimization of Early-Phase Clinical Trials Pilot Program; Request for Information, Federal Register, April 29, 2026.

Comments

Join the discussion with an anonymous comment.