Introduction: The Scale of AI Adoption in Health Insurance

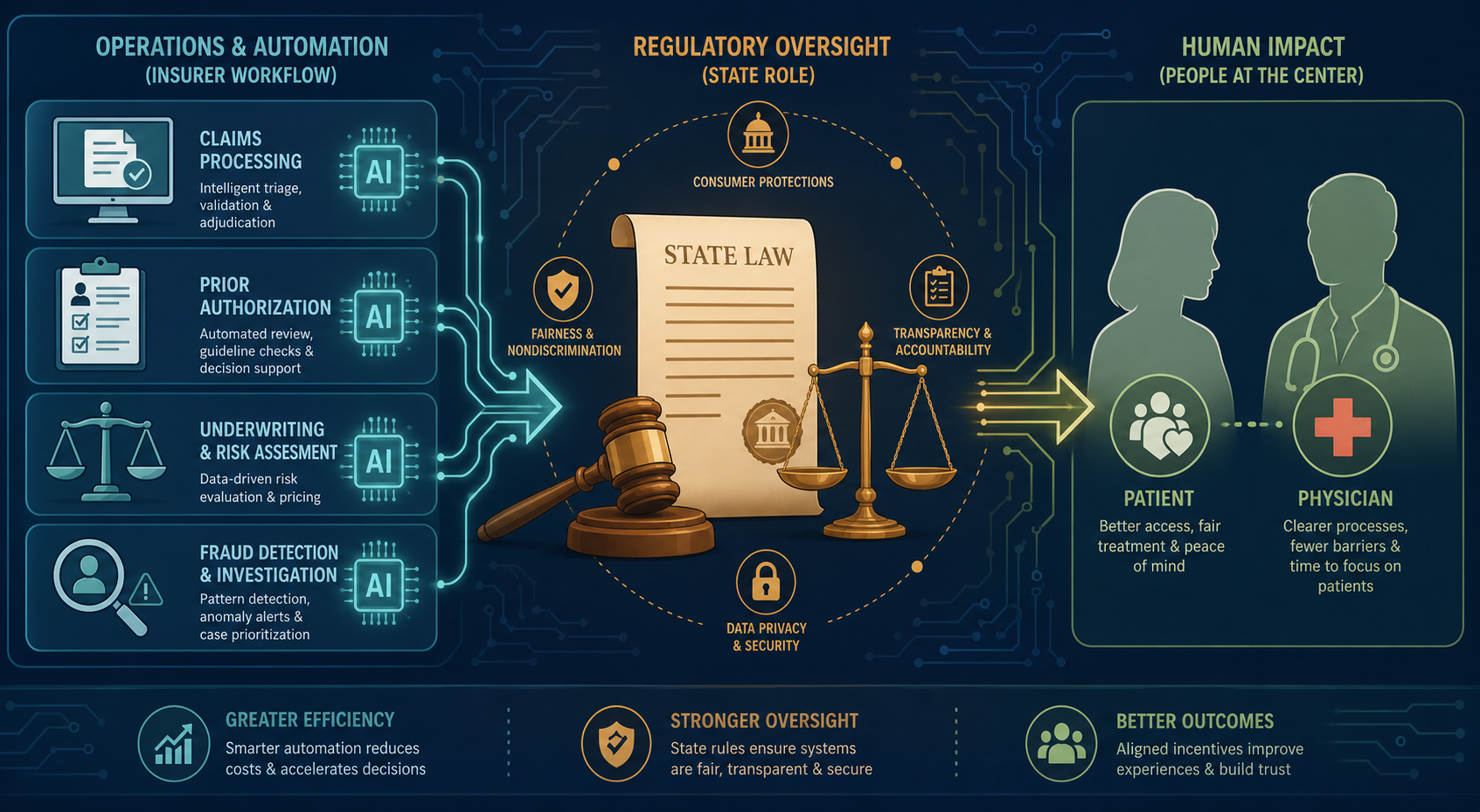

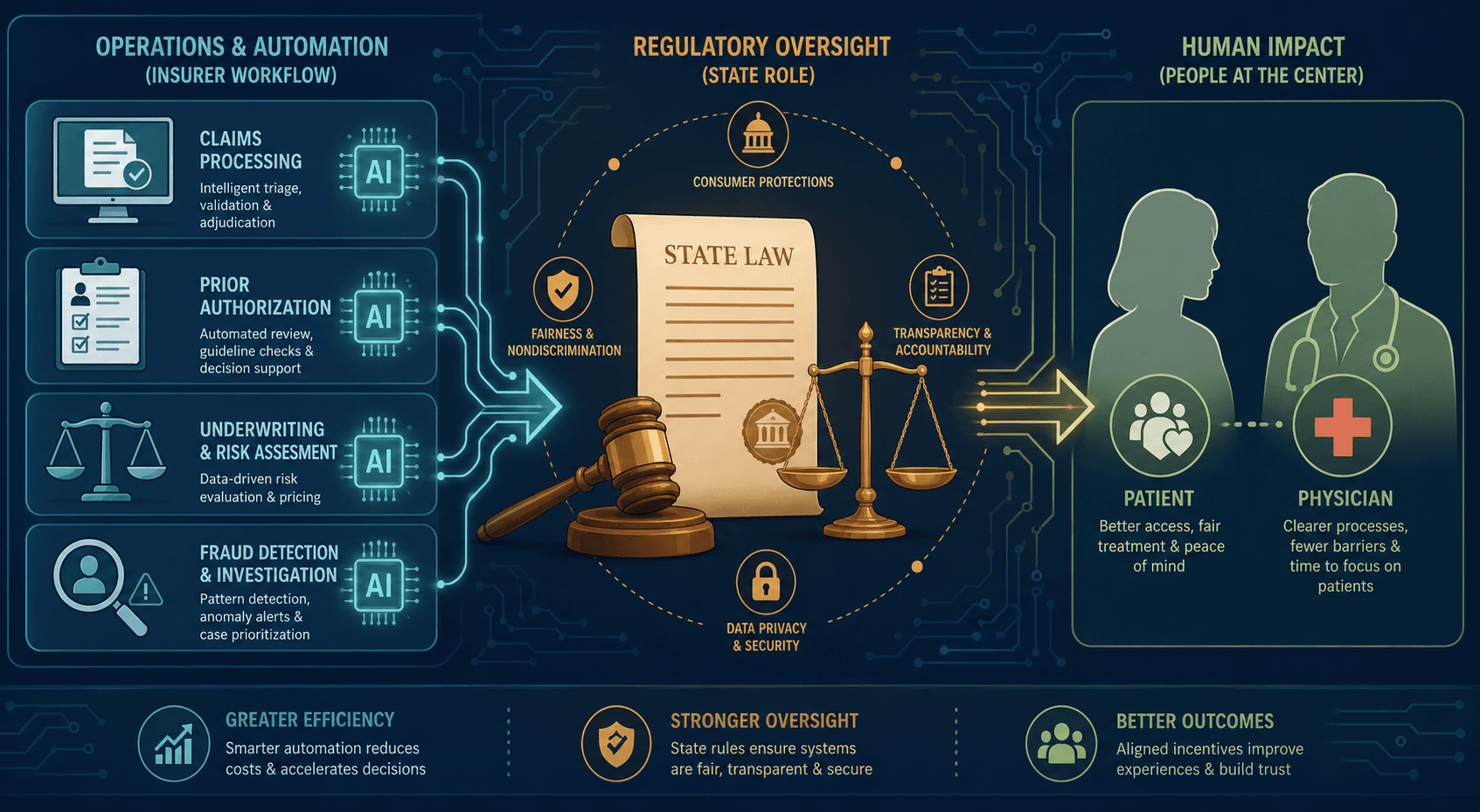

Artificial intelligence is no longer an experimental tool in the health insurance industry — it is a core operational technology. The most comprehensive survey to date, conducted by the National Association of Insurance Commissioners (NAIC) between November 2024 and January 2025 across 16 states, found that 84% of large health insurers (those with over $250 million in earned premiums) now report using AI or machine learning across their product lines. The survey, which collected responses from 93 companies, represents the first systematic, multi-state effort to quantify the penetration of AI in payer operations.

This article provides a comprehensive, evidence-grounded analysis for healthcare policy professionals, health system administrators, compliance officers, and researchers. The central thesis is straightforward: AI adoption in health insurance utilization management is accelerating rapidly, but governance at every level — federal, state, and institutional — has not kept pace. The result is a growing wave of state-level regulation, class-action litigation, and physician distrust that is reshaping the deployment landscape faster than the technology itself.

The stakes are high. Prior authorization has long been a source of friction between insurers and providers, with physicians reporting that administrative burdens consume an average of 13 hours per week per physician. AI promises to streamline these workflows, but critics argue that by making utilization review cheaper to conduct, AI could supercharge a system already prone to delays and wrongful denials. The evidence emerging from physician surveys, litigation filings, and regulatory investigations suggests those concerns are not hypothetical.

How Insurers Are Deploying AI: Prior Authorization, Claims Adjudication, and Utilization Management

The NAIC survey provides the most granular breakdown available of how insurers are actually using AI. The data reveals a spectrum of deployment, from relatively low-risk automation tasks to high-stakes clinical decision-making.

| Use Case | Percentage of Insurers Using or Exploring AI/ML | Risk Level |

|---|---|---|

| Utilization management (broadly defined) | 56% | High |

| Prior authorization for approval | 37% (68% for individual major medical plans) | High |

| Claims adjudication | 44% | High |

| Disease management | 61% | Moderate |

| Claims fraud detection | 50% | Low-Moderate |

| Medical provider fraud detection | 51% | Low-Moderate |

| Sales and marketing | 45% | Low |

| Denying prior authorizations | 12% | Critical |

The 12% of insurers that report using AI to support denial decisions is the most controversial figure in the survey. While a minority, these are among the largest carriers in the country. UnitedHealth Group, for example, is spending approximately $1.5 billion on AI in 2026, and its Optum Real subsidiary is processing 500 million transactions annually — a volume projected to reach 2.5 billion by year end. The company reports that its digital prior authorization tool achieves a 96% approval rate, though this figure is self-reported and has not been independently validated.

Other major deployments include Humana's rollout of Google Cloud's Gemini-powered Agent Assist to more than 20,000 member advocates, handling up to 80 million calls per year, and Oscar Health's Oswell AI agent, which the company reports handles 86% of member questions and reduced peak response times by 67%. These figures, while operationally impressive, come from carrier and vendor disclosures rather than independent audits.

The Stanford HAI policy brief on responsible AI in health insurance decision-making flags a critical concern: AI tools trained on historical coverage decisions will inevitably lock in flawed patterns. If past denials were inappropriate or biased, the AI will replicate and scale those errors. This is not a hypothetical risk — it is a structural feature of how supervised learning models work when trained on legacy claims data.

The Controversy: Physician Distrust, Denial Rate Allegations, and Patient Harm

The deployment of AI in utilization management has generated a credibility crisis that extends far beyond the usual insurer-provider friction. The American Medical Association's 2024 survey of physicians provides the most comprehensive evidence of the scale of the problem.

- Three in five physicians (61%) are concerned that health plans' use of AI is increasing prior authorization denials.

- 94% of physicians reported that prior authorization has a negative impact on patient clinical outcomes.

- 93% reported delayed access to necessary care.

- 82% reported that patients abandon treatment due to authorization struggles.

- 29% reported that prior authorization led to a serious adverse event for a patient, including hospitalization, permanent impairment, or death.

The 29% figure for serious adverse events is particularly striking. It represents physicians' direct experience — not a controlled study — but it signals a level of harm that regulators cannot ignore. Physicians reported completing an average of 39 prior authorizations per week, consuming 13 hours of physician and staff time. 88% reported that prior authorization requirements lead to higher overall utilization of healthcare resources, a finding that undercuts the efficiency rationale for the process.

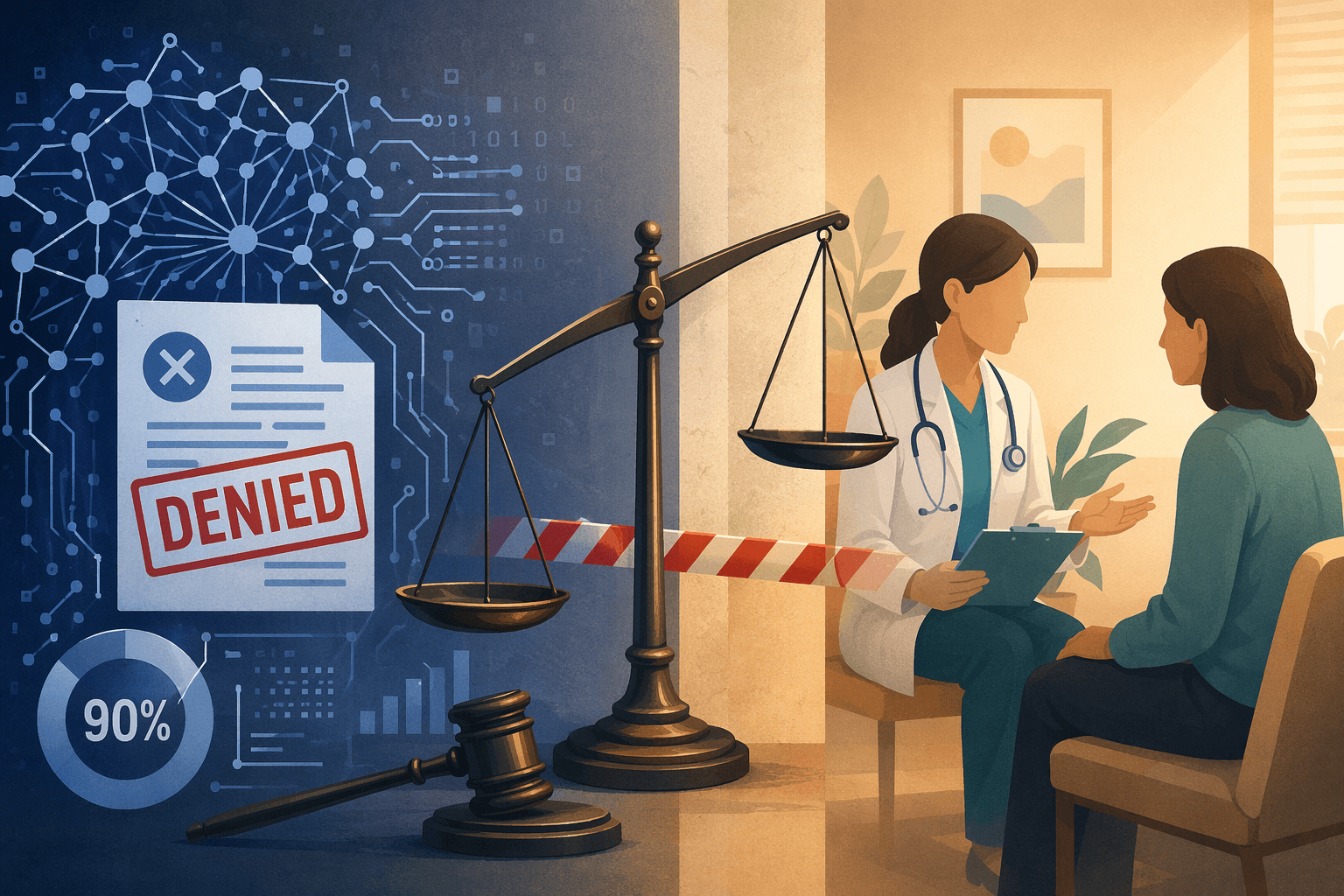

The most explosive allegation comes from the federal class action against UnitedHealth Group. The lawsuit, Estate of Gene B. Lokken et al. v. UnitedHealth Group, Inc., alleges that the company's nH Predict AI model has a 90% error rate on appealed denials. The plaintiffs claim that the AI model was designed to deny care that would have been covered under the terms of the plan, and that human reviewers were pressured to follow the AI's recommendations rather than exercise independent medical judgment.

The U.S. District Court for the District of Minnesota partially denied UnitedHealth's motion to dismiss in February 2025, allowing breach of contract and breach of implied covenant claims to proceed. The court found that the plaintiffs had plausibly alleged that the AI model systematically denied claims that should have been covered.

The broader context for these allegations is the Medicare Advantage appeals system. Data from 2019 to 2023 shows that while Medicare Advantage plans approved more than 93% of prior authorization requests at the initial level, the overturn rate on appeal was 82%. This massive discrepancy — a 93% initial approval rate but an 82% appeal overturn rate — suggests that the initial denial decisions are frequently incorrect. If AI is being used to generate those initial denials, the 82% overturn rate becomes a direct measure of AI error in practice.

The AMA survey also notes that AI tools have been accused of producing denial rates 16 times higher than typical. While this figure is attributed to physician reports rather than independent measurement, it reflects a widespread perception among clinicians that AI-driven utilization review is fundamentally different in kind — not just in degree — from traditional manual review.

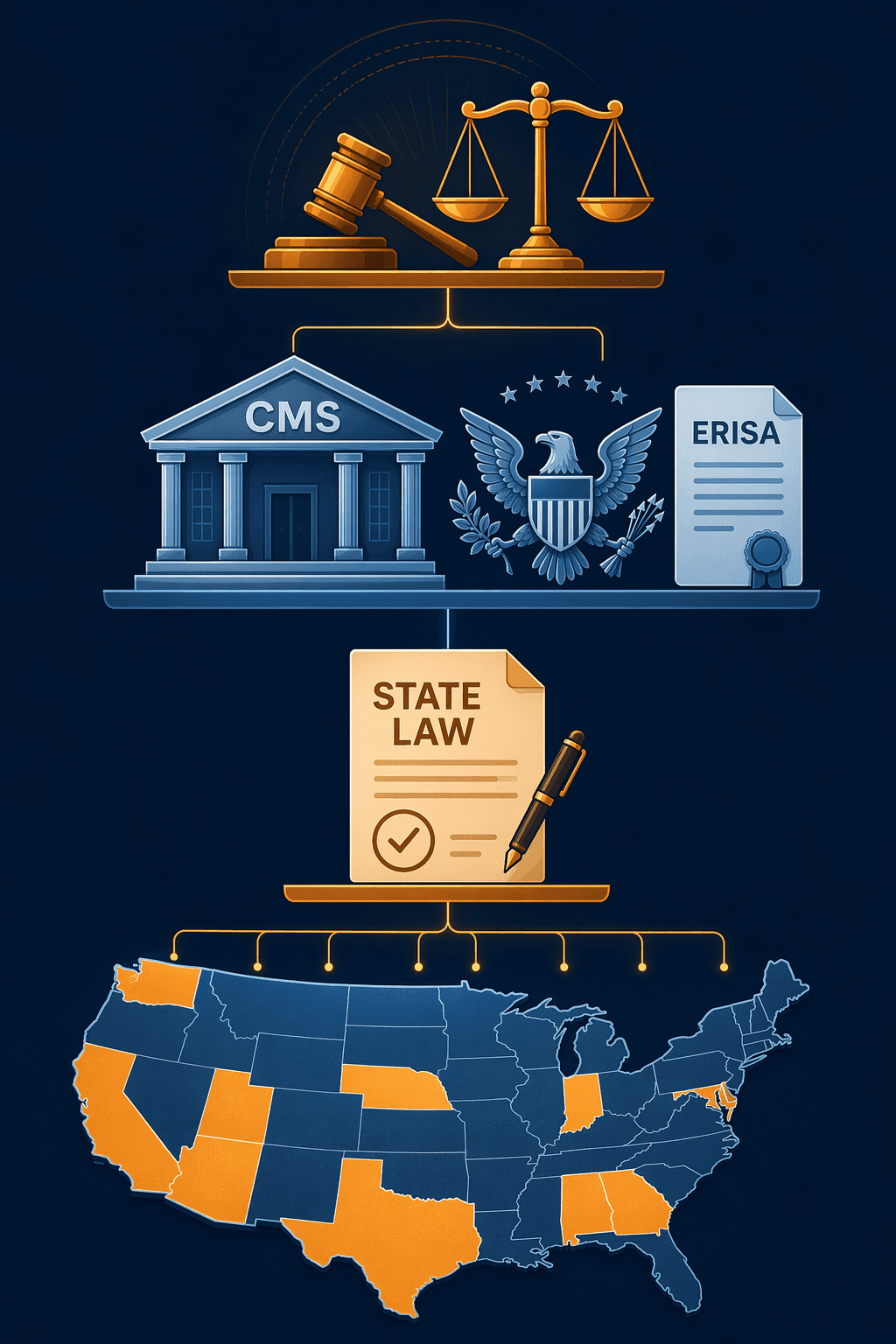

Regulatory Response: CMS Guardrails and the Unfinished 2026 AI Provisions

The federal regulatory response to AI in health insurance has been piecemeal. The most significant action to date is the Centers for Medicare & Medicaid Services (CMS) rule that took effect in January 2024, which requires Medicare Advantage plans to base medical necessity determinations on the individual circumstances of each enrollee and to have those determinations reviewed by a physician or other appropriate health care professional. The rule was a direct response to concerns that automated systems were being used to deny care without adequate human oversight.

However, the CMS rule does not explicitly address AI. It requires human review of denials, but it does not set standards for how AI can be used in the initial screening or recommendation process. This gap became the focus of proposed 2026 AI guardrails that would have required plans to validate their AI tools against real-world outcomes, disclose AI use to beneficiaries, and ensure that AI-driven decisions could be meaningfully appealed.

Those proposed guardrails were not finalized. The KFF issue brief published in May 2026 confirms that the 2026 AI provisions were proposed but never adopted, leaving a significant regulatory gap at the federal level. This means that as of mid-2026, there is no federal standard specifically governing how AI can be used in health insurance utilization management — only the general CMS requirement that individual circumstances be considered and that a physician review denials.

Meanwhile, CMS transparency rules that took effect in March 2026 require public disclosure of prior authorization approval and denial metrics across Medicare Advantage, Medicaid managed care, CHIP, and ACA plans. This is a significant step toward accountability, but it measures outcomes, not processes. A plan could report high denial rates without revealing that an AI model with a documented error rate generated those denials.

State-Level Action: A Wave of AI-Specific Insurance Laws (2025–2026)

With federal action stalled, states have become the primary arena for AI governance in health insurance. As of April 2026, at least 11 states have enacted laws that directly regulate the use of AI in utilization management, and more than 25 states have adopted the NAIC model bulletin guidance on AI governance. The state laws vary in scope and specificity, but they share a common core: AI cannot be the sole basis for denying medical care.

| State | Bill | Effective Date | Key Provisions |

|---|---|---|---|

| California | SB 1120 | January 1, 2025 | Restricts AI as sole basis for denial; requires licensed physician for final medical necessity determinations. |

| Arizona | HB 2175 | 2025 | Requires independent review by healthcare providers before denial. |

| Texas | SB 815 | 2025 | Prohibits AI for adverse determinations; allows AI only for administrative support or fraud detection; commissioner may audit AI systems. |

| Nebraska | LB 77 | 2025 | Prohibits AI output as sole basis for medical necessity decisions; requires disclosure of AI use. |

| Alabama | SB 63 | October 1, 2026 | Requires AI-based PA decisions to consider enrollee's medical history and unique clinical circumstances; annual certification to DOI. |

| Indiana | HB 1271 | July 1, 2026 | Prohibits AI as sole basis for downcoding claims without healthcare professional review of medical record. |

| Utah | SB 319 | January 1, 2027 | Requires disclosure of AI use to Insurance Department, providers, and enrollees; requires independent medical judgment for adverse determinations. |

| Washington | SB 5395 | 2026 | Prohibits reliance solely on AI to deny, delay, or limit services; requires human review of adverse determinations; reporting of PA denials aided by AI. |

| Maryland | HB 820 / HB 1563 | June 1, 2026 | Requires AI tools to consider individual circumstances; mandates quarterly reporting of adverse decisions to insurance commissioner. |

| Georgia | SB 544 | January 1, 2027 | Permits AI for automation and decision-making support; prohibits AI-based adverse determinations without licensed healthcare provider review and approval. |

Several patterns emerge from this legislative wave. First, the laws are converging on a common standard: AI can assist but cannot decide. Every statute requires some form of human involvement in final adverse determinations. Second, disclosure requirements are becoming more specific. Utah's law, for example, requires disclosure to the Insurance Department, providers, and enrollees — a three-way transparency mandate that goes beyond any other state. Third, audit rights are expanding. Texas gives its insurance commissioner explicit authority to audit AI systems, and Maryland's quarterly reporting requirement creates a data stream that can be used for enforcement.

The Holland & Knight legal alert notes that these state laws create a compliance challenge for national insurers, who must now navigate a patchwork of requirements that differ on key details — what constitutes adequate human review, what must be disclosed, and how frequently reporting is required. For health systems and providers, the variation creates uncertainty about what protections apply to their patients in different states.

Federal Policy Tension: The Trump Administration AI Framework and ERISA Preemption

The state-level regulatory push is colliding with a federal policy framework that takes a fundamentally different approach. The Trump administration's March 2026 AI Framework recommends federal preemption of what it characterizes as "cumbersome" state AI laws and establishes a Department of Justice litigation task force to challenge state AI rules that the administration believes create barriers to innovation.

This creates a direct tension. States like California, Texas, and Maryland have enacted laws that explicitly restrict how AI can be used in health insurance. The federal framework, by contrast, prioritizes removing regulatory barriers to AI deployment. The KFF issue brief identifies this as an unresolved conflict that creates significant compliance uncertainty for insurers operating across multiple states.

The ERISA dimension adds another layer of complexity. Employer-sponsored health plans are governed by the Employee Retirement Income Security Act of 1974 (ERISA), which generally preempts state laws that "relate to" employee benefit plans. If a federal court finds that a state AI law is preempted by ERISA, the law would not apply to the millions of Americans covered by employer-sponsored plans — precisely the population that state legislators were trying to protect.

For health system administrators and compliance officers, the practical implication is that the regulatory landscape is not just fragmented — it is actively contested. A state law that protects patients in one jurisdiction may be preempted for patients in the same hospital who happen to have employer-sponsored insurance. This uncertainty makes it difficult to design consistent appeals processes and patient communication strategies.

Litigation Landscape: Class Actions Against UnitedHealthcare and Cigna

The most significant legal development in AI-driven utilization management is the federal class action against UnitedHealth Group. The case, Estate of Gene B. Lokken et al. v. UnitedHealth Group, Inc., filed in the U.S. District Court for the District of Minnesota, alleges that the company's nH Predict AI model systematically denies care that should be covered under the terms of employer-sponsored health plans.

The plaintiffs' central allegation is that nH Predict has a 90% error rate on appealed denials — meaning that when patients or providers challenge a denial, the original decision is overturned 90% of the time. The lawsuit claims that UnitedHealth designed the AI model to maximize denials rather than accurately assess medical necessity, and that human reviewers were given inadequate time and training to meaningfully override the AI's recommendations.

In February 2025, the court partially denied UnitedHealth's motion to dismiss, allowing breach of contract and breach of implied covenant claims to proceed. The court found that the plaintiffs had plausibly alleged that the AI model systematically denied claims that should have been covered — a legal threshold that, if proven at trial, could establish that AI-driven denials violate ERISA's fiduciary duties.

A separate case against Cigna involves similar allegations. The Cigna lawsuit claims that the company used an algorithmic system to automatically deny claims without individual physician review, and that the company's own physicians were pressured to approve denials generated by the algorithm without independent evaluation. While the Cigna case has received less attention than the UnitedHealth litigation, it raises the same fundamental question: can an AI system make medical necessity determinations that are binding on patients?

For health systems, the litigation creates both risk and opportunity. The risk is that if AI-driven denials are found to be unlawful, health systems that have relied on payer AI tools for prior authorization may face retrospective liability for claims that were improperly denied. The opportunity is that the litigation is generating a public record of how AI tools actually perform — data that can inform procurement decisions and contract negotiations with insurers.

Conclusions and Outlook: Closing the Governance Gap

The evidence assembled in this article supports a clear conclusion: AI adoption in health insurance utilization management has outpaced governance at every level. The NAIC survey shows that 84% of large insurers are using AI, but the regulatory framework — federal, state, and institutional — was designed for a world in which human beings made coverage decisions. The gap between deployment and governance is not narrowing; it is widening.

The consequences of this gap are visible in the data. The AMA survey documents widespread physician distrust and patient harm. The Medicare Advantage 82% appeal overturn rate suggests systemic over-denial. The UnitedHealthcare class action alleges a 90% error rate for a specific AI tool. State legislatures are responding with a patchwork of laws that create compliance complexity without establishing a coherent national standard.

- Algorithmic bias: AI models trained on historical claims data will replicate and scale existing patterns of discrimination and inappropriate denial.

- Lack of transparency: Insurers are not required to disclose which AI tools they use, how they were validated, or what their error rates are.

- Physician distrust: 61% of physicians believe AI increases denials, and 29% report serious adverse events linked to prior authorization.

- Litigation exposure: The UnitedHealthcare and Cigna cases could establish that AI-driven denials violate ERISA fiduciary duties, creating industry-wide liability.

- Regulatory fragmentation: State laws vary on key provisions, and the federal preemption push creates uncertainty about which rules apply.

Looking ahead to the next 12–18 months, several developments warrant close attention. The UnitedHealthcare class action is likely to proceed toward discovery, which could produce the first public audit of a major payer AI system. The Trump administration's DOJ litigation task force may challenge specific state AI laws, creating test cases for the preemption question. CMS may revisit the proposed 2026 AI guardrails, particularly if the appeal overturn rate data continues to generate political pressure. And more states are expected to follow the California-Texas-Maryland model, potentially creating a critical mass of regulation that forces federal action.

For health system administrators and compliance officers, the immediate priority should be understanding which AI tools their contracted insurers are using and what rights patients have under applicable state law. The transparency requirements in states like Utah and Maryland create new data streams that can be used to monitor denial patterns. For policy professionals and researchers, the priority should be developing evidence-based standards for AI validation in utilization management — standards that do not currently exist at any level of government.

Comments

Join the discussion with an anonymous comment.