The useful starting point for AI computing contracts in defense and healthcare is not a product demo. It is the procurement asymmetry facing a healthcare buyer in 2026. The Department of Defense sits on AI-related contract potential value reported at $90.7 billion across 1,319 contracts, up from $4.6 billion in 2024; the same analysis puts actual obligations at $7.2 billion, a much smaller figure that matters because ceiling value is not spend.[1] HHS, by comparison, is moving quickly but from a different scale: its potential AI contract value is reported at $138 million, after 448% growth, across more than 271 AI use cases.[1]

That gap does not mean defense has already bought the future and healthcare is simply next in line. It means the short list of cloud regions, model providers, GPU capacity, data platforms, and compliance templates available to healthcare has been shaped in a market where DoD requirements carry the heaviest bargaining power. By the time a health system CIO asks which AI infrastructure stack is “healthcare-ready,” the answer may already have been narrowed by classified-network access, government cloud authorizations, model access agreements, and compute capacity bought for national-security workloads.

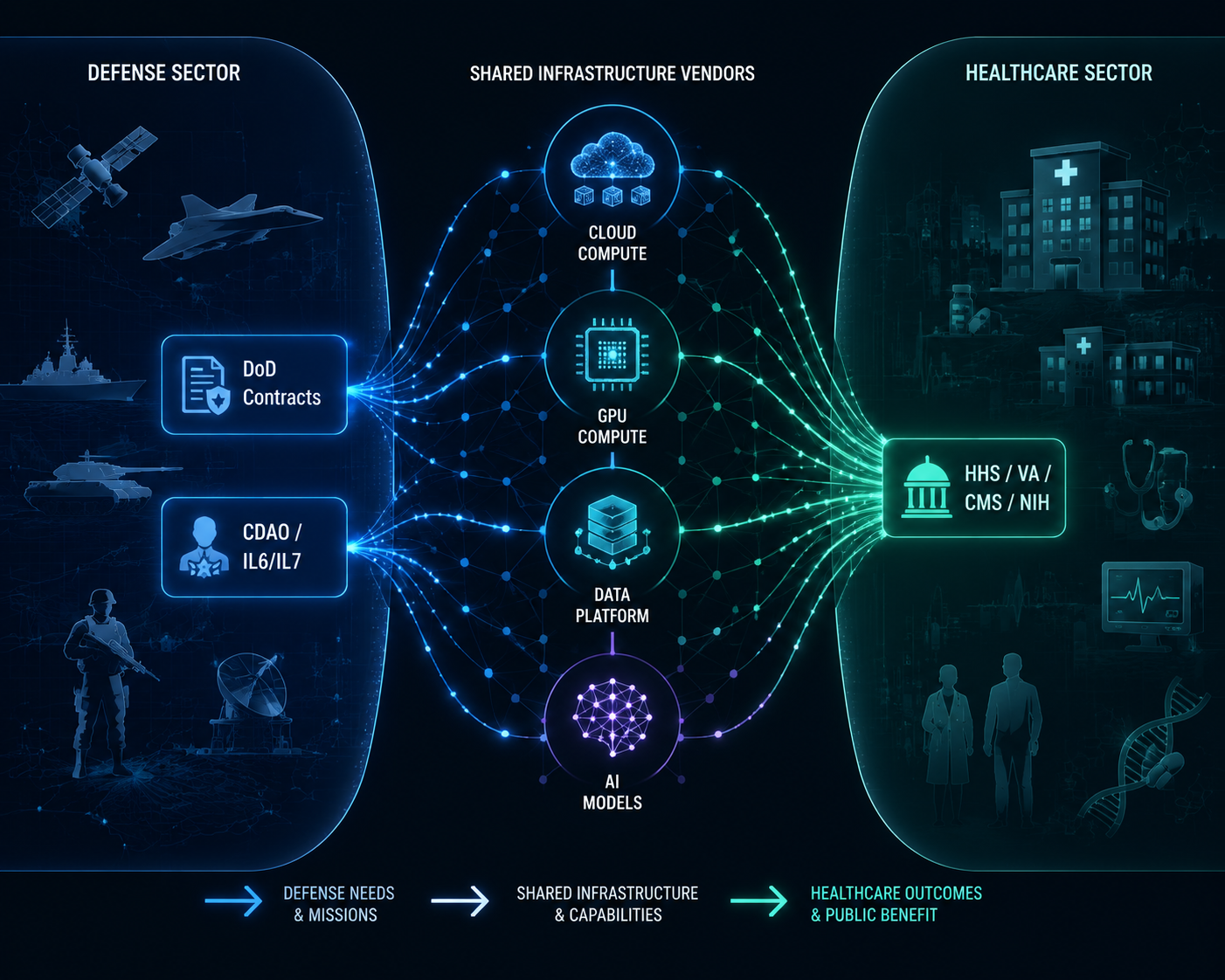

The important connection is not that a battlefield AI tool becomes a clinical tool. Most do not, and clinical validity cannot be borrowed from a defense authorization. The connection is more basic: both buildings are increasingly plugged into the same utility grid.

The Defense Ceiling Sets the Market Conversation

The $90.7 billion figure should be read with discipline. It is potential value across contracts that mention AI, not a ledger of checks already written.[1] But ceiling value still changes a market. It tells vendors where to build certified capacity, which sales teams get senior attention, where reference architectures mature, and which security assumptions become normal before healthcare buyers enter the room.

The clearest example is the Chief Digital and Artificial Intelligence Office’s July 2025 ceiling awards of up to $200 million each to Google, OpenAI, Anthropic, and xAI.[2] Those awards did not prove that any one model is fit for a hospital workflow. They did show that frontier model access, government contracting, and federal AI infrastructure were being packaged at a scale and speed that civilian health agencies rarely dictate on their own.

Then came the classified-network layer. In May 2026, eight vendors were identified for IL6 and IL7 classified network access: AWS, Google, Microsoft, NVIDIA, OpenAI, Oracle, Reflection, and SpaceX.[3] For healthcare, IL6 and IL7 are not routine requirements. But the capacity, security engineering, audit posture, and government-cloud operating patterns developed for those environments influence the same vendor roadmaps that later appear in HHS, VA, NIH, DHA, and hospital-system conversations.

| Defense-side signal | Healthcare procurement consequence |

|---|---|

| Large AI contract ceilings and obligations below ceiling | Healthcare buyers inherit price anchors without being able to treat ceiling value as actual market spend |

| CDAO model awards to frontier AI vendors | Model access discussions arrive already shaped by federal terms, security review, and government-cloud delivery assumptions |

| IL6 and IL7 classified-network access for cloud, compute, and model vendors | FedRAMP, isolation, auditability, and government-cloud maturity become practical vendor differentiators |

| Enterprise data-platform agreements such as Palantir’s Army work | Health agencies see mature data integration platforms before equivalent healthcare-specific evidence exists |

Palantir illustrates the same point from the data-platform side. A March 2026 Pentagon memo made Palantir’s Maven Smart System a core military AI system, and the company also had a $10 billion Army enterprise agreement for data integration.[4] That does not make a defense targeting platform a healthcare platform. It does, however, help explain why a data-integration vendor can arrive in healthcare with an enterprise-contracting vocabulary, security posture, and deployment story already tested against federal buyers with larger ceilings than most health agencies can offer.

What Carries Over Is Infrastructure, Not Clinical Proof

The carryover mechanism is easy to miss because vendors describe it in healthcare language once they are selling to healthcare. Underneath, the same components keep reappearing: Google Cloud TPUs, Microsoft Azure Government, AWS GovCloud, NVIDIA H100s, Palantir Foundry, and access to frontier models through government-approved environments. These are not interchangeable labels. They decide where data can sit, who can administer the environment, how audit logs are retained, which models can be called, and what procurement officers can compare.

Google’s CDAO award announcement, for example, emphasized Google Cloud infrastructure and TPU capacity across the continental United States.[5] For NIH researchers using cloud programs such as STRIDES, the relevance is not that a defense contract becomes a grant. It is that a major cloud provider’s government AI capacity, accelerator planning, and support model are being matured in a federal environment where defense demand is unusually powerful.

The compute layer is moving in the same direction. Defense reporting has described a fiscal 2027 supercomputing modernization request of about $30 billion, while contractor positioning analysis cites a fiscal 2026 AI request of $13.4 billion and the same roughly $30 billion fiscal 2027 modernization figure.[6][7] Those numbers are requests and positioning signals, not proof of final appropriations or healthcare availability. Still, they help explain why scarce accelerator supply, secure hosting, and high-performance AI infrastructure are not priced in a healthcare-only market.

This matters most in vendor conversations that appear mundane. A healthcare CIO asking whether an AI workload should run in a commercial cloud, a government cloud, a dedicated tenant, or an air-gapped environment is not only asking a technical question. The CIO is being asked to accept a procurement lineage: FedRAMP expectations, NIST AI Risk Management Framework language, government-cloud contract vehicles, incident-reporting terms, model monitoring commitments, and assumptions about who can inspect the stack.

HHS has been pushing that conversation from the policy side. Analysis of the HHS AI strategy highlights a five-pillar approach, the creation of an AI Governance Board, and an April 3, 2026 deadline for agencies to identify high-impact AI systems.[8] That deadline did not create the cloud market, but it gave health agencies a governance clock. Procurement teams suddenly needed vendors who could speak not only about accuracy or automation, but about inventory, risk classification, oversight, monitoring, and documentation.

That is where the federal AI compliance discussion becomes a procurement issue, not a side memo from legal. A health agency that aligns with NIST AI RMF language still has to buy something: a cloud environment, a model endpoint, a data platform, an observability layer, or professional services. The same pressure shows up in broader public-health AI regulation, where ClinicalMind’s analysis of federal and state AI regulation in public health tracks how governance obligations are becoming operational requirements. The buyer’s problem is not deciding whether governance matters. It is deciding which vendors can produce the evidence artifacts fast enough to clear review.

Draft federal procurement language is moving in the same direction. Rohirrim’s analysis of the Pentagon AI contracting environment points to the broader May 2026 awards era and GSA procurement clause activity as part of a contracting shift toward explicit AI terms.[9] For healthcare buyers, the consequence is that “AI-ready” increasingly means “ready for federal review,” even when the clinical use case is still local and unsettled.

Healthcare Agencies Are Already Buying Into the Same Vendor Market

The healthcare-side evidence is not a single master contract proving that defense built healthcare AI. It is a pattern of parallel demand. HHS potential AI contract value has risen to $138 million, with more than 271 AI use cases identified in the Brookings analysis.[1] That is small next to DoD’s potential value, but large enough to force agencies into the same questions about cloud capacity, approved environments, data integration, and model governance.

NIH shows the research version of the problem. Federal News Network reported that NIH AI use cases rose 51% to 124 even as the agency faced reductions in force affecting more than 4,000 staff, and it described the role of STRIDES in giving researchers access to commercial cloud resources.[10] That combination is not a neat productivity story. It is a capacity story: more AI work, fewer internal people, and more dependence on external cloud infrastructure that has its own federal contracting center of gravity.

CMS shows the operational version. ExecutiveGov reported that CMS saved $2 billion using AI fraud detection since March 2025.[11] That number supports a narrower conclusion than vendors often want: AI can be attached to high-value administrative and fraud workflows in federal healthcare. It does not prove that the same infrastructure will produce safe clinical decision support, or that savings from fraud detection translate into patient-care outcomes.

VA sits somewhere between care delivery, benefits administration, and federal-scale data operations. Its AI strategy page lists 367 AI use cases and an $8.8 million National AI Institute, while separate budget reporting describes a $130 million fiscal 2027 request for AI automation at the Veterans Benefits Administration.[12][13] The use-case count may include overlaps across programs, so it should not be treated as 367 mature deployments. It does show a federal health system attempting to manage AI as a portfolio rather than as scattered experiments.

DHA makes the defense-healthcare boundary especially visible because it is both a military organization and a healthcare operator. Federal News Network’s reporting on military health AI described battlefield trauma tracking through BATDOK and ambient clinical documentation in the Military Health System.[14] GovConWire reported a $1.61 billion health readiness IDIQ and a $300 million MHS GENESIS health IT deployment IDIQ.[15] Those figures should be handled carefully because IDIQ ceilings are not guaranteed spend, but they show how military healthcare can procure care-delivery technology inside the same institutional environment that is hardening defense AI infrastructure.

The Vendor Shortlist Is Being Narrowed Before the Hospital RFP

A hospital RFP can still look open. Procurement can invite several vendors, score them against clinical, financial, security, and integration criteria, and run a formal comparison. But the infrastructure field behind that RFP is rarely blank. If the workload needs government-cloud maturity, FedRAMP documentation, mature identity controls, data-residency options, accelerator access, and a model governance story, the shortlist begins to look familiar before the first demo.

This is why the overlap among Google, Microsoft, AWS, NVIDIA, Palantir, OpenAI, Anthropic, Oracle, and other federal AI vendors matters even when the healthcare use case is not military. Defense demand helps determine which vendors can afford to maintain specialized secure environments, which ones can negotiate model access at federal scale, which ones can staff compliance reviews, and which ones can absorb long procurement cycles. Healthcare buyers then encounter those capabilities as if they were naturally “healthcare AI infrastructure.”

| Infrastructure layer | Defense procurement pressure | Healthcare inheritance |

|---|---|---|

| Cloud environment | Government and classified workloads require isolation, auditability, and authorized regions | Health agencies compare vendors partly on FedRAMP posture, government-cloud maturity, and data-control options |

| Compute | AI simulation, classified workloads, and supercomputing modernization increase demand for accelerators | Healthcare research and imaging workloads face price and availability conditions shaped outside medicine |

| Foundation models | CDAO awards normalize federal access agreements with frontier model vendors | Healthcare buyers ask whether model endpoints can meet public-sector security, monitoring, and governance terms |

| Data platforms | Enterprise defense agreements mature integration and operational analytics platforms | VA, DHA, and health systems encounter platforms with federal deployment histories but still need clinical validation |

| Compliance artifacts | DoD and federal procurement clauses make documentation, risk controls, and review evidence routine | HHS, VA, NIH, and hospital CIOs inherit templates that help procurement but do not establish medical effectiveness |

The distinction between infrastructure readiness and clinical evidence is the line healthcare procurement cannot afford to blur. A secure enclave can reduce some data-exposure risks. A government cloud can simplify certain public-sector reviews. A vendor with DoD experience may understand audit trails, identity management, and procurement documentation. None of that shows that a sepsis model improves outcomes, an ambient documentation tool reduces burnout without increasing note errors, or an imaging model performs safely across patient populations.

Defense-grade compliance can be useful and still insufficient. It answers questions about environment, access, resilience, and control. Healthcare has to add questions about clinical workflow, patient safety, bias, liability, informed use, adverse-event monitoring, and whether the model’s output should influence care at all. The shared infrastructure may be a starting point for review, but it is not a substitute for one.

How a CIO Should Read the Contract Map

The practical reading is not to avoid vendors with defense work. In 2026, that would remove many of the providers most capable of offering secure cloud, model access, accelerator capacity, and federal documentation. The practical reading is to know which parts of the vendor’s credibility come from infrastructure performance and which parts still need healthcare proof.

- Separate ceiling value from obligated spend. A $200 million ceiling or a multibillion-dollar IDIQ can indicate market positioning, but it does not show how much work was actually delivered.

- Ask which environment the healthcare workload will actually use. A vendor’s classified or government-cloud capability may not be the same environment proposed for a hospital deployment.

- Treat FedRAMP, NIST AI RMF alignment, and governance artifacts as necessary procurement evidence, not as clinical outcome evidence.

- Map model access separately from data access. The safest cloud architecture can still create unacceptable risk if prompts, outputs, logs, or fine-tuning data are governed poorly.

- Price the dependency. If a healthcare AI roadmap depends on one cloud, one accelerator class, one model provider, or one data platform, that dependency belongs in the risk register before it becomes an operating constraint.

The most useful vendor question is often plain: which claims are proven by your federal infrastructure work, and which claims are proven in healthcare? A good answer separates security authorization from patient impact, cloud maturity from model performance, data integration from clinical adoption, and procurement speed from safety.

Healthcare AI buyers are therefore not merely choosing among healthcare vendors. They are entering a market whose infrastructure has been hardened, priced, and prioritized through defense procurement. The useful standard is simple: separate ceiling from obligation, separate infrastructure readiness from clinical evidence, and treat defense-healthcare vendor overlap as a strategic dependency to manage rather than a shortcut to trust.

References

- Where does federal AI spending stand in 2026? — Brookings

- Anthropic, Google, OpenAI and xAI win Pentagon AI contracts worth up to $200 million each — CNBC

- Pentagon clears vendors for IL6/IL7 classified network access — Nextgov/FCW

- Pentagon adopts Palantir AI as core military system — Reuters

- Google Public Sector awarded CDAO contract to accelerate AI adoption — Google Cloud Blog

- Pentagon seeks $30B for supercomputing modernization — DefenseScoop

- Defense AI contractor positioning analysis — CCS Global Tech

- HHS AI Strategy analysis — Holland & Knight

- Pentagon AI contracts analysis — Rohirrim

- NIH advances AI pilots amid staff reductions — Federal News Network

- AI and cloud are reshaping federal healthcare — ExecutiveGov

- Building the Future: VA’s AI Strategy — U.S. Department of Veterans Affairs

- VA budget proposal seeks funding for AI automation at VBA — Nextgov

- Military Health System expands battlefield and clinical AI tools — Federal News Network

- DHA awards health readiness and MHS GENESIS deployment IDIQs — GovConWire

Comments

Join the discussion with an anonymous comment.