South Africa’s Ozempic market did not move on one front in July 2026. It moved on three. Novo Nordisk scheduled Extensior, its lower-cost authorized copy of Ozempic, for launch on July 27; Sun Pharma received SAHPRA approval for Semagard, the first generic semaglutide approved in the country, on July 15; and regulators escalated action against compounded iDexis semaglutide and tirzepatide products through a coordinated recall backed by court orders, fines, professional-liability pressure, and possible license consequences.[1][2][3]

That is why the phrase “Ozempic biosimilar launch in South Africa and healthcare access” needs one correction before the access question can be answered. These products are not biosimilars in the strict regulatory sense. Semaglutide is a peptide. Extensior is an authorized copy — the same active pharmaceutical ingredient and manufacturing base under a different name and packaging — while Semagard is a generic. The distinction matters because each product changes the market in a different way.

This is an industry-access event, not a clinical guidance story. The relevant questions are not whether GLP-1 medicines work, or which patient should be started on semaglutide. The sharper questions are who can legally supply, who can price below the branded benchmark, who can survive the patent environment, who gets reimbursed, and what happens when a large informal channel is removed before the formal system has widened.

A Watershed, But Not Yet Access

The case for calling July 2026 a watershed is strong. South Africa has seen branded GLP-1 demand grow faster than the reimbursement and public-sector machinery around it. The GLP-1 market reportedly tripled from about $45 million to $134 million in 18 months, while Ozempic climbed from 170th to 12th place in medical scheme spending.[4] Those are not small changes at the edge of a sleepy category. They show a medicine class pushing into scheme budgets before the country has settled the basic access rules.

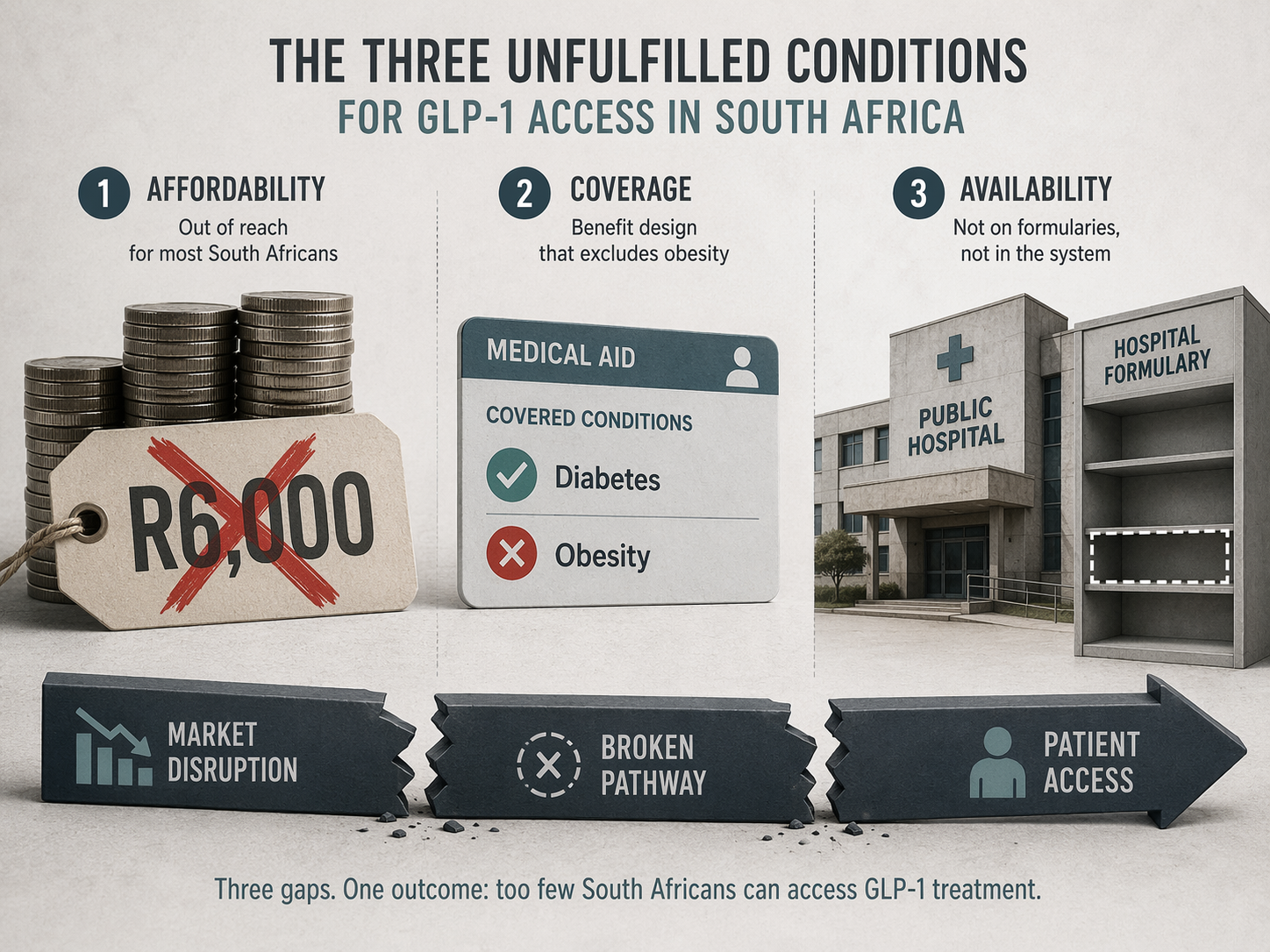

The pressure is not mysterious. South Africa has about 2.3 million adults with diabetes and around 30% adult obesity prevalence, the highest in the WHO African region.[5][6] Yet GLP-1s remain absent from the public sector. Private-sector patients face monthly treatment costs commonly described in the R3,000–R6,000 range, and scheme coverage is still tied mainly to narrow diabetes criteria rather than broad obesity treatment. Obesity itself is not a prescribed minimum benefit.

That gap explains why the iDexis recall belongs in the same article as Extensior and Semagard. iDexis was reportedly manufacturing about 84,500 compounded units monthly, more than the combined sales of Ozempic and Wegovy in South Africa.[3] A supply channel of that scale does not appear because patients are calmly waiting for formulary committees. It appears when demand has outrun affordable, reimbursed, regulated supply.

The Three Disruptions Do Different Work

Extensior is the least surprising and most defensive of the three moves. Novo Nordisk is not surrendering the South African semaglutide market; it is segmenting it. An authorized copy lets the originator concede price pressure without allowing all demand to migrate to a rival generic or to compounded products. It also keeps the company inside the access conversation at the moment when payers and policymakers are asking why a medicine with such large metabolic relevance remains largely private.

But the crucial Extensior number was still missing at the time of the launch announcement: the price. Reuters reported the July 27 launch plan, but pricing was expected closer to launch and had not yet been disclosed.[1] Without that number, Extensior is evidence of competitive pressure, not evidence of access. A lower-cost copy that remains near private-sector affordability limits would protect market share more than it would change treatment availability.

Semagard does something different. Sun Pharma’s SAHPRA approval tests the regulatory and patent opening from the outside. It is the first generic semaglutide approved in South Africa, but approval is not the same as commercial availability. Reuters reported the approval on July 15; launch date and pricing were not yet announced.[2] For access, those missing details are not administrative footnotes. They decide whether Semagard becomes a real price competitor or remains a signal that the market may open later.

The patent context explains why this approval is unusual without making patents the whole story. Novo Nordisk’s South African semaglutide portfolio has been described as 15 patents: 11 granted, three pending, and one expired. The core compound patent ZA200707261 is due to expire in 2027, while secondary patents extend much further, in some cases to 2045.[7] That structure does not prevent every market move before 2027, but it does make any generic approval before the core expiry commercially and legally significant.

The iDexis action is neither a price launch nor a patent event. It is enforcement catching up with a parallel supply system. South African regulators moved against compounded GLP-1 products with a recall supported by an interim court order, fines reportedly ranging from R25,000 to R75,000, professional-liability pressure, and the possibility of license consequences.[3] The word “interim” should not be skipped. It means the order is not a final judgment. Still, the practical message to prescribers and suppliers is already clear: the tolerated space for compounded semaglutide has narrowed sharply.

Demand Has Already Outrun the Formal Channel

The South African GLP-1 story is often told as if it begins with weight-loss aspiration and ends with patent expiry. That misses the access mechanics. Demand is already showing up in three places at once: medical scheme claims, private cash-paying use, and compounded-product demand. The market’s rise from about $45 million to $134 million in 18 months shows commercial acceleration; Ozempic’s jump in scheme spending shows payer exposure; iDexis’s reported monthly output shows what happens outside the branded channel.[3][4]

Those measures are not interchangeable. Scheme spending does not mean broad reimbursement. Private market sales do not mean affordability. Compounded output does not prove equivalent quality or legal acceptability. Together, however, they show a category whose demand is larger than the system built to contain it.

This is where enforcement creates a hard access problem. Regulators had strong reasons to act against unauthorized compounded products, especially when supply claims run ahead of formal approvals and quality oversight. But removing a channel producing tens of thousands of units a month also exposes the vacuum that allowed it to grow. Patients do not become eligible for public-sector GLP-1 treatment because a recall notice is issued. Clinicians do not gain a reimbursed obesity pathway because a compounder is pushed out.

What Would Have to Change for Patients

The access test is narrower than the market event. Three things would have to happen before July’s disruption materially narrows the treatment gap.

| Condition | Why it matters | Status in July 2026 |

|---|---|---|

| Prices must fall far below branded levels | A lower-cost product only changes access if monthly treatment moves out of the R3,000–R6,000 bracket for a meaningful share of patients | Extensior pricing undisclosed; Semagard pricing unannounced |

| Medical scheme rules must loosen | Private reimbursement remains limited if coverage stays tied to restrictive diabetes criteria while obesity is excluded from prescribed minimum benefits | No broad obesity coverage shift reported |

| Public-sector formularies must include GLP-1s | South Africa’s largest access gap sits in the public sector, where GLP-1s remain unavailable | Essential medicines review prioritized, but no public formulary inclusion yet |

Price Is the First Gate

The first access gate is brutally simple: a product can be cheaper than Ozempic and still be too expensive for most patients. Current monthly treatment costs in the R3,000–R6,000 range already exclude many people who could clinically benefit. A modest discount may help schemes manage budgets, but it will not by itself create mass access.

This is why the off-patent manufacturing debate matters, even though it has not yet materialized in South Africa. Analysts have projected that off-patent semaglutide could eventually be mass-produced for roughly $3–15 per month.[8][9] That is not a South African retail price forecast, and it should not be treated as one. It is a boundary marker: it shows how large the gap may be between production economics and current patient-facing prices once patents, distribution, devices, margins, and procurement systems are layered on top.

Coverage Is the Second Gate

The second gate is reimbursement. Even if Extensior or Semagard lands at a clear discount, medical scheme access can remain narrow if rules continue to focus on diabetes and exclude obesity as a prescribed minimum benefit. That distinction matters in South Africa because the unmet need is not confined to diagnosed diabetes. The obesity burden is large, but a medicine can be clinically relevant to obesity and still sit outside routine benefit design.

Neither Extensior nor Semagard should be overread here. At the time of the reported announcements, neither product was approved for weight-loss-only prescribing. That limits their immediate usefulness for obesity access, regardless of how they are discussed in the market. The label is not a small technicality when schemes and prescribers are deciding whether a claim is payable.

The Public Sector Is the Third Gate

The third gate is the hardest and the most important. South Africa’s public sector has no GLP-1 route. For a country with about 2.3 million adults with diabetes and the highest adult obesity prevalence in the WHO African region, that absence defines the access gap more than any private-sector launch does.[5][6]

There is now a policy opening, but not yet a formulary result. WHO added GLP-1 medicines to its Essential Medicines List in 2025 for long-term obesity treatment, and South Africa’s national essential medicines process has prioritized a review following that move.[6] That can change procurement logic if it leads to listing, tendering, and budget allocation. Until then, the public-sector patient remains outside the main GLP-1 market, even as private brands, authorized copies, generics, and enforcement actions move around them.

Why This Is Bigger Than One Product Launch

The unusual feature of July 2026 is not that South Africa has interest in semaglutide. That was already obvious. The unusual feature is that three market-shaping forces arrived together: originator price segmentation, independent generic approval, and enforcement against informal compounding. In most medicine markets, these forces appear in sequence. Here they collided.

Novo’s move protects share while acknowledging that the branded price environment cannot simply be defended by scarcity and patent position. Sun’s approval creates a formal generic challenger before the core compound patent expires in 2027, although the secondary patent landscape still reaches much further. The iDexis recall warns that unofficial supply cannot be the de facto access policy for a high-demand metabolic therapy.[1][2][3][7]

For investors and manufacturers, this makes South Africa a test market for emerging-market GLP-1 strategy. For payers, it turns a budget-pressure category into a coverage-design problem. For policymakers, it raises a procurement question that cannot be answered by waiting for branded demand to stabilize. And for patients, it may still mean very little next month if prescriptions remain expensive, restricted, or unavailable in public clinics.

Aspen’s GLP-1 ambitions do not yet change that conclusion. The available material points to Canada first, with South African timing uncertain. It may become relevant, but it is not part of the immediate July access mechanism.

The Narrow Answer

July 2026 genuinely changes the African GLP-1 market. South Africa now has an authorized copy scheduled, a SAHPRA-approved generic, and a regulator-backed move against a large compounded supply channel within the same two-week window. That combination has not been the normal emerging-market script for semaglutide.

It does not yet prove that South Africa’s GLP-1 treatment gap has narrowed. Extensior’s price was still undisclosed in the available launch reporting. Semagard’s launch date and pricing were still unannounced. Neither product had a weight-loss-only approval in the reported materials. The iDexis court order was interim. The public sector still had no GLP-1 pathway.

The market has changed before the access system has caught up. Whether patients feel the change depends on three decisions that are still ahead: prices must fall to a level that is not merely less expensive but meaningfully affordable; medical schemes must move beyond narrow diabetes-only reimbursement; and the essential medicines review must translate into public-sector formulary inclusion.

References

- Novo Nordisk to launch lower-cost Ozempic copy in South Africa, Reuters, July 17, 2026.

- India's Sun Pharma wins South Africa approval to launch generic Ozempic, Reuters, July 15, 2026.

- South Africa escalates Ozempic crackdown, Business Insider SA, July 2026.

- Blockbuster weight-loss and diabetes medicines sales surge despite cost barriers, Spotlight, February 4, 2026.

- IDF Diabetes Atlas, International Diabetes Federation, 2024.

- WHO backs GLP-1 drugs for long-term obesity treatment, Sowetan, December 2, 2025.

- Ozempic, Patents, and a possible costly oversight, Eversheds Sutherland SA.

- Off-patent semaglutide in 2026, IQVIA, July 2025.

- Ozempic goes generic, MedicalBrief.

Comments

Join the discussion with an anonymous comment.