Adoption Snapshot: How Fast Is Generative AI Entering Healthcare?

The pace at which generative AI has moved from pilot projects to daily clinical use is the defining healthcare technology story of 2026. According to the American Medical Association, over 80% of physicians now report using AI in their professional work — double the rate recorded in 2023. Yet the same data reveals a striking gap: only about one in four healthcare organizations (25%) have formally implemented AI tools, based on research from Menlo Ventures. This disconnect between individual clinician adoption and institutional governance is not a lag — it is the central structural tension of the current moment.

Market projections reinforce the sense of acceleration. The global generative AI healthcare market, valued at roughly $2.6 billion in 2025, is forecast to reach between $48 billion and $53 billion by 2035. These figures come with significant methodological variance across research firms, but the directional signal is consistent: capital is flowing into generative AI faster than the evidence base or regulatory framework can mature.

A Fall 2024 survey of 43 U.S. health systems found that 100% of respondents reported adoption activities in ambient notes — generative AI clinical documentation — though only 53% described a high degree of success. The same survey identified immature AI tools as the biggest barrier to adoption (cited by 77% of respondents), followed by financial concerns (47%) and regulatory uncertainty (40%). These numbers capture a field that is moving fast but unevenly, with pockets of genuine operational impact alongside widespread caution.

Where It’s Working: Three Domains with Real-World Evidence

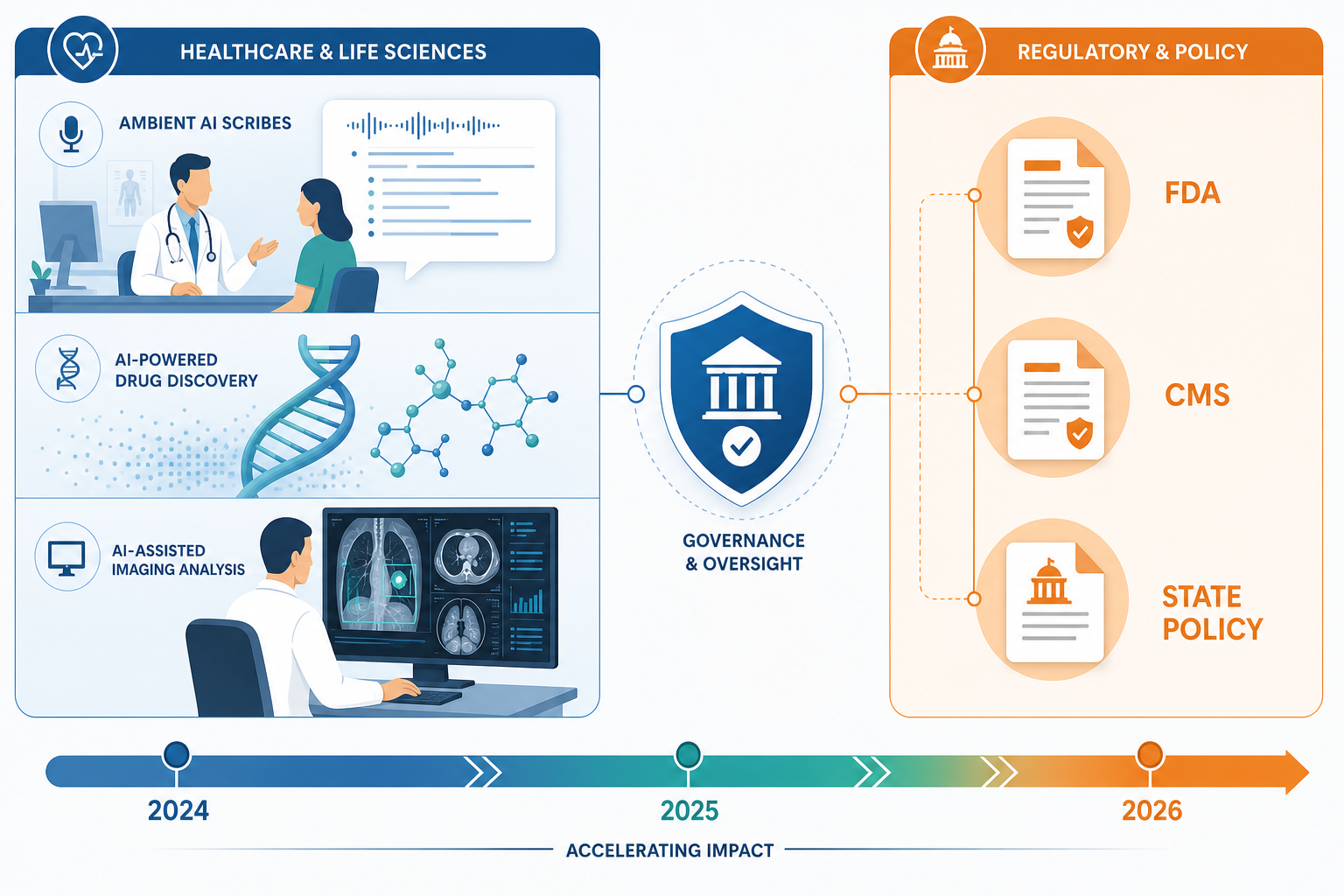

Generative AI’s transition from experimental to operational is not uniform across healthcare. Three domains stand out for having accumulated enough real-world evidence to demonstrate measurable impact: ambient AI scribes, drug discovery, and medical imaging. Each illustrates a different dimension of the governance gap — not because the technology is failing, but because it is succeeding faster than the policy infrastructure designed to oversee it.

Ambient AI Scribes: The Strongest Evidence Base

The most compelling real-world data comes from a 63-week study conducted by The Permanente Medical Group (TPMG) between October 2023 and December 2024. Across 7,260 physicians and more than 2.5 million patient encounters, ambient AI scribes saved an estimated 15,791 hours of documentation time — equivalent to 1,794 eight-hour workdays. The clinical impact was equally notable: 84% of physicians reported improved patient communication, and 82% reported improved work satisfaction. High users accounted for 89% of all activations, suggesting that the technology’s benefits compound with familiarity.

These results are not an isolated case. A 2025 review found that AI-powered documentation tools could reduce nursing documentation time by 21–30%, saving 95–134 hours per year per nurse. In revenue cycle management, Deloitte estimates generative AI can save 41–50% of professional time. The operational case is clear — and it is precisely this clarity that makes the regulatory gap concerning. Ambient scribes are now embedded in daily workflows at scale, yet the policy frameworks governing their use remain fragmented.

For a deeper dive into the clinical evidence across these and other domains, see our companion article: Generative AI and Health: What the Clinical Evidence Actually Shows in 2026.

Drug Discovery: 173+ AI-Originated Programs in Clinical Trials

Drug discovery represents the domain where generative AI’s potential impact is largest but its regulatory pathway is most uncertain. As of early 2026, over 173 AI-originated drug programs have entered clinical trials, according to industry estimates. The AI drug discovery market is approximately $5–7 billion in 2025, with projections reaching $8–10 billion in 2026.

The EU AI Act’s high-risk provisions, which take effect on August 2, 2026, could classify some drug development AI as high-risk, introducing mandatory compliance requirements that may reshape how these tools are developed and deployed. This creates an unusual dynamic: the technology is advancing through clinical trials, but the regulatory framework that will govern its next stage of deployment is only now being finalized.

Medical Imaging: Generative Models for Data Augmentation

In medical imaging, generative adversarial networks (GANs) have demonstrated strong technical performance for data augmentation and image segmentation. One study reported a Dice coefficient of 0.89 for MRI brain segmentation using GAN-based approaches. While this domain has not yet produced the large-scale deployment evidence seen in ambient scribes, it represents a rapidly maturing application area where generative models are being used to address the chronic shortage of annotated training data.

For a broader view of how AI is reshaping clinical workflows across specialties, see AI in Medicine: How It’s Actually Reshaping Clinical Workflows.

The Regulatory Landscape: 2026 as an Inflection Point

Three major policy developments in 2026 define the regulatory inflection point for generative AI in healthcare. Each represents a different dimension of the governance gap, and together they illustrate why this year is critical for the technology’s trajectory.

FDA’s January 2026 Policy Shift on Clinical Decision Support

On January 6, 2026, FDA Commissioner Marty Makary announced that the agency will soften its approach to regulating clinical decision support (CDS) software. Under the new policy, products that deliver a single recommendation can enter the market without FDA review, provided they fulfill other criteria for escaping regulation. The practical implication is significant: unregulated generative AI tools could now enter clinical workflows without premarket evaluation.

This decision represents a deliberate choice to prioritize innovation access over premarket validation. For health system administrators and compliance teams, it creates a new category of risk: tools that are legally marketable but clinically unvalidated. The burden of evaluation shifts from the FDA to individual health systems, many of which lack the infrastructure to conduct independent AI assessments.

CMS Reimbursement Pathways: Building the Economic Infrastructure

On the reimbursement front, CMS is moving to create formal payment pathways for AI-enabled services. On April 9, 2025, Senators Rounds and Heinrich introduced the Health Tech Investment Act (S 1399), which would establish a Medicare payment system for algorithm-based healthcare services (AHBS) delivered through FDA-cleared or -approved AI devices. The bill would assign AHBS to a new technology ambulatory payment classification for at least five years, providing a stable reimbursement pathway that could accelerate adoption.

This legislative effort sits alongside emerging CMS coverage decisions, such as the AI-detected coronary calcium code. Together, they signal that the economic infrastructure for AI reimbursement is being built — but it is being built around FDA-cleared devices, not the unregulated generative AI tools that the January 2026 FDA policy shift enables. The result is a two-tier system: regulated tools with clear reimbursement pathways, and unregulated tools with none.

For a detailed analysis of CMS coverage decisions, see our dedicated article: CMS AI Reimbursement Policy: Coverage Decisions for AI-Assisted Diagnostics.

The Shadow AI Governance Gap

Perhaps the most pressing governance challenge is “shadow AI” — the use of unvetted generative AI tools by clinicians without institutional approval. Wolters Kluwer’s 2026 healthcare AI trends report notes that shadow AI surged in 2025, and that forward-thinking organizations are beginning to explore “AI safe zones”: controlled environments for safe experimentation with approved tools. As Wolters Kluwer CTO Alex Tyrrell stated, “2026 will be the year of governance. Health system C-suites are playing catch-up to clinicians who have rapidly adopted GenAI apps.”

| Policy Development | Date | Impact on Generative AI | Governance Gap Dimension |

|---|---|---|---|

| FDA softens CDS oversight | Jan 6, 2026 | Unregulated GenAI tools can enter clinical workflows without premarket review | Premarket validation vs. market access |

| Health Tech Investment Act (S 1399) | Apr 9, 2025 | Creates Medicare payment pathway for FDA-cleared AI devices | Reimbursement infrastructure vs. unregulated tools |

| Shadow AI surge | 2025–2026 | Clinicians using unvetted GenAI apps without institutional approval | Institutional governance vs. individual adoption |

| EU AI Act high-risk provisions | Aug 2, 2026 | May classify drug development AI as high-risk, requiring compliance | International regulatory divergence |

Persistent Risks: Hallucination, Bias, and Privacy

The governance gap is not merely an administrative inconvenience — it amplifies real clinical risks that the existing evidence base has documented but not resolved. Three categories of risk are particularly relevant for policy professionals and health system administrators evaluating generative AI tools.

Hallucination Rates in Clinical Contexts

A scoping review of 120 papers published by March 2024 found that hallucination rates in clinical decision support models are estimated at 8–20%. While 64% of the reviewed papers addressed model hallucinations, only 9.2% suggested modifying model parameters to address the problem. This gap between problem identification and solution development is a critical vulnerability, particularly as the FDA’s January 2026 policy shift allows unregulated generative AI tools to enter clinical workflows without premarket evaluation of their hallucination risk.

Bias Propagation and Dataset Limitations

The same scoping review found that 58% of papers addressed bias, but few proposed concrete fixes. In clinical contexts, generative AI models trained on datasets that underrepresent certain populations can propagate and amplify existing disparities. The risk is not hypothetical: models that perform well on benchmark datasets often degrade significantly when deployed in diverse clinical settings, and the lack of standardized bias auditing frameworks makes it difficult for health systems to evaluate this risk during procurement.

Privacy Vulnerabilities Across the AI Lifecycle

A 2024 JMIR study identified privacy threats across the generative AI lifecycle that are distinct from traditional data security concerns. These include model inversion attacks (reconstructing training data from model outputs), membership inference attacks (determining whether a specific patient’s data was used in training), and attribute disclosure attacks (inferring additional patient details from model responses). The regulatory response to these threats remains fragmented: the EU AI Act categorizes medical AI as high-risk with mandatory compliance requirements, while the U.S. AI Bill of Rights offers nonbinding principles.

Outlook: What the Evidence-Policy Gap Means for 2026 and Beyond

The central story of generative AI in healthcare in 2026 is not about any single technology breakthrough or regulatory decision. It is about the widening gap between operational deployment and regulatory readiness. Ambient AI scribes have saved tens of thousands of clinician hours. AI-originated drug programs are moving through clinical trials. Generative models are improving medical image analysis. But the policy frameworks that should govern these tools — ensuring they are safe, equitable, and effective before they reach patients — are being built reactively, not proactively.

For health system administrators and procurement teams, this gap creates practical challenges:

- The FDA’s January 2026 policy shift means that some generative AI tools entering clinical workflows have not undergone premarket evaluation. Health systems must develop their own evaluation frameworks or rely on third-party assessments.

- CMS reimbursement pathways are being built around FDA-cleared devices, creating a financial incentive structure that may not align with the tools clinicians are actually using.

- Shadow AI adoption is forcing organizations to choose between restrictive bans that drive usage underground and permissive policies that lack safety guardrails. The “AI safe zone” model — controlled environments for approved experimentation — represents a middle path that several forward-thinking organizations are exploring.

- The EU AI Act’s high-risk provisions, effective August 2, 2026, will introduce mandatory compliance requirements that may create regulatory divergence between U.S. and European markets, complicating global deployment strategies.

The evidence-policy gap is not a temporary condition that will resolve itself. It is a structural feature of a field where technology development outpaces the institutional processes designed to govern it. Closing this gap will require coordinated action across multiple fronts: clearer FDA guidance on what constitutes a “single recommendation” under the new CDS policy, standardized bias auditing frameworks that health systems can use during procurement, and formal governance structures that allow safe experimentation without exposing patients to unvalidated tools.

For policy professionals, researchers, and health system leaders, the task is not to slow adoption but to build the governance infrastructure that adoption requires. The technology is already in the clinic. The question is whether the policy framework will catch up before the risks catch up with the technology.