The multiple sclerosis drug pricing cliff in Australia became visible before it became a formal access rupture. Ocrevus, Kesimpta, and Lemtrada were still on the Pharmaceutical Benefits Scheme, but the reimbursement logic around them had shifted sharply after Briumvi entered the scheme at a lower price. By early July 2026, Roche and Novartis were being asked to absorb price cuts reported at roughly 40–50%, a figure attributed in public reporting to industry sources rather than official departmental confirmation.[1]

That distinction matters. A reported cut is not the same as a published government schedule. But even with that caveat, the number explains why this was not treated as a routine PBS price movement. A 40–50% reset is the sort of change that can turn a reimbursement formula into a commercial withdrawal threat, even when the medicine remains clinically appropriate for the patient sitting in front of a neurologist.

The contradiction was awkward because both halves were true. The PBS was doing what it is built to do: press prices downward when comparable medicines are available. At the same time, the architecture that disciplines prices had created a cliff for established high-efficacy MS therapies. When Health Minister Mark Butler announced on July 16 that the drugs would remain PBS-listed while a rapid review was completed by December 2026, the immediate patient shock was deferred, not resolved.[3]

How the PBS Price Rule Became a Cliff

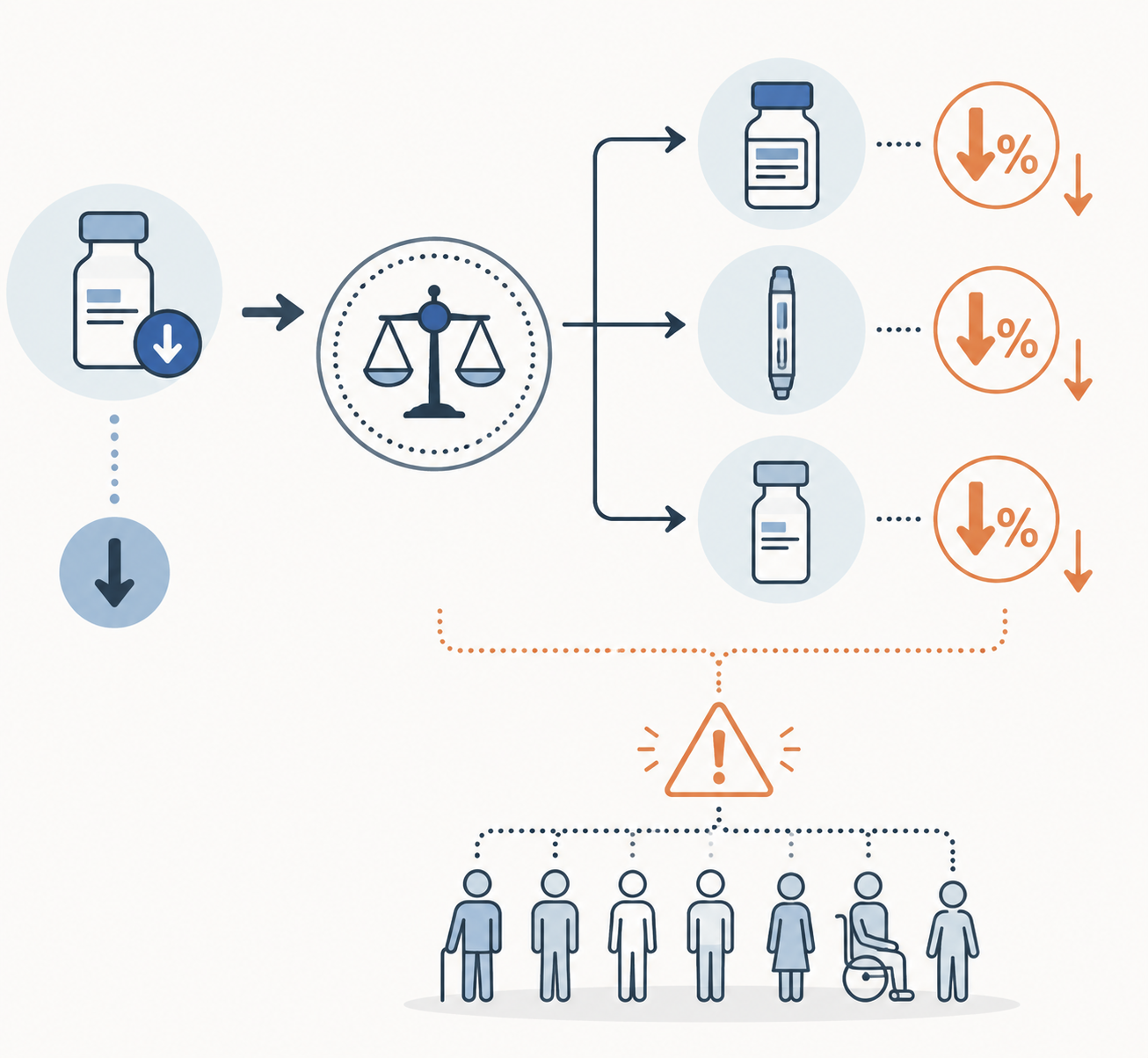

The trigger was Briumvi, ublituximab, a new treatment for relapsing-remitting MS. MS Australia announced that Briumvi would be listed on the PBS from January 1, 2026.[2] Some accounts have described the timing as late 2025; the clean way to read that is as the difference between the recommendation or listing process and the effective PBS date. The reimbursement consequences began once Briumvi sat inside the relevant PBS pricing frame.

PBS reference pricing is simple in principle and uncomfortable in edge cases. Medicines judged therapeutically similar can be grouped so the government does not pay materially different prices for treatments expected to deliver similar clinical value. When a lower-priced medicine enters the group, it can reset the benchmark against which the others are assessed. That is defensible as public purchasing discipline. It is also how a cheaper entrant can change the economics of products that were already embedded in clinical practice.

In this case, the lower Briumvi price appears to have pulled Ocrevus and Kesimpta toward a much lower reimbursement expectation. ABC News reported that Roche and Novartis rejected cuts understood to be in the 40–50% range.[1] Medical Republic similarly reported that the PBS future of leading MS therapies was hanging on a pricing decision, with the pressure tied to reference pricing after Briumvi’s entry.[5]

The important word is “grouped.” The PBS was not merely comparing list prices in the abstract. It was applying a mechanism that treats therapeutic similarity as a reason to align reimbursement. If one medicine can meet the government’s access and value requirements at a lower price, the system asks why the others should keep a higher public price. That is the budgetary logic. The clinical question is narrower and harder: whether therapeutic similarity at group level should translate into a near-immediate reimbursement cliff for each individual product in a class where switching, stability, route of administration, dosing interval, prior response, and clinician judgment all matter.

Nothing in that mechanism requires a company to accept the new price. The PBS can set the condition for subsidy; the manufacturer can decide whether the subsidized market still works commercially. That is where the cliff appears. Gradual price disclosure can be absorbed, planned around, or contested over time. A very large benchmark-driven reduction creates a binary choice: accept the lower reimbursement or risk walking away from subsidized access.

| Step | What Changed | Why It Mattered |

|---|---|---|

| Briumvi entered the PBS | Ublituximab became available through the PBS from January 1, 2026 | A lower-priced comparator entered the MS treatment group |

| The benchmark shifted | Therapeutically similar medicines faced pressure to align with the lower price | The pricing question moved from one product to the whole group |

| Existing manufacturers resisted | Reported cuts of roughly 40–50% were rejected by Roche and Novartis | The dispute became an access question rather than only a budget question |

| PBAC considered the issue | The committee met July 8–10, 2026 | The immediate decision point arrived before a broader policy fix |

| A rapid review was announced | The drugs stayed PBS-listed while review work continued to December 2026 | The cliff was bridged temporarily, not redesigned |

Why “Still Listed” Was Not the Whole Story

The neat administrative reassurance was that patients did not immediately lose PBS access. After the July 8–10 PBAC meeting, Butler said Ocrevus, Kesimpta, and Lemtrada would remain available on the PBS while the government conducted a rapid review due by December 2026.[3] The Guardian also reported that the medicines would stay on the PBS during that process.[4]

But “listed” is not a complete access category if the listing is commercially unstable. A medicine can remain in the schedule while a manufacturer disputes the price conditions attached to continued supply. A patient can hear that the PBS has preserved access and still face a credible risk that the company supplying their therapy may decide the reimbursement is not viable. That is why the public language of lifeline and the private anxiety of interruption could coexist.

The patient arithmetic was stark. ABC reported that without subsidy, Ocrevus would cost about $33,000 per year, while PBS patients paid the standard subsidized co-payment rather than the full price.[1] The Guardian reported PBS co-payments of $25 for general patients and $7.70 for concession card holders as of January 2026.[4] The difference between those numbers is the practical meaning of PBS access: not a discount at the margin, but the difference between ordinary affordability and a bill most households could not absorb.

Reports placed about 10,000 patients at risk from the dispute.[1][4] That figure should not be read as 10,000 people immediately losing medicine in July. It is a measure of exposure to the access risk if the standoff had ended in withdrawal or restricted supply. For a stable MS patient on a high-efficacy therapy, however, even a deferred risk has clinical weight. Stability is not a bureaucratic status; it is often the outcome that years of treatment selection have been trying to protect.

The Anti-CD20 Context Makes the Pricing Question Less Tidy

Briumvi, Ocrevus, and Kesimpta sit in a treatment landscape where anti-CD20 therapies have become central to MS care; Lemtrada sits nearby as another high-efficacy option in the same access debate. MS Australia’s 2025 reporting put the number of Australians living with MS at 37,756, up 77% since 2010, with total economic burden exceeding $3 billion per year.[6] Its prevalence and health economic impact work also reported $592 million in spending on disease-modifying therapies and indicated that roughly half of treated patients were using anti-CD20 therapies.[7]

Those figures do not prove that every affected option must be reimbursed at its historic price. They do show why this was not a small pricing footnote. When a reimbursement rule affects high-use MS therapies, it reaches into a large share of contemporary treated care. If the rule narrows practical choice, the consequences fall on patients already living with a disease whose costs are distributed across medicine, disability, productivity, informal care, and health system use.

Maintaining multiple options is not the same as paying any price asked. That distinction is worth keeping intact. Ocrevus, Kesimpta, Lemtrada, and Briumvi differ in ways that matter operationally and clinically, including mode and timing of administration, patient history, tolerance, monitoring needs, and clinician preference. A reference price can reasonably ask whether the public system is overpaying for similar outcomes. It cannot, by itself, settle whether a lower group benchmark preserves enough therapeutic plurality for real-world MS care.

This is where the manufacturer argument becomes more than familiar industry resistance to lower prices. A company saying “this threatens innovation” is too broad to carry the issue. A company saying “at this reimbursement level, we may not continue supply of a therapy used by thousands of subsidized patients” raises a concrete access consequence. That consequence still needs scrutiny, but it belongs in the same room as the public payer’s need to discipline prices.

The Rapid Review Bought Time, Not a Design Answer

The July sequence was compressed. ABC reported on July 8 that the dispute could leave patients facing huge bills for Ocrevus and Kesimpta if the drugs were pulled from subsidized access.[1] PBAC met from July 8 to 10. On July 16, Butler confirmed the medicines would remain PBS-listed while a rapid review examined the issue, with completion due by December 2026.[3]

That review should not be mistaken for a final settlement. It is a policy process created under pressure, not proof that the reference pricing architecture has been repaired. The 2024 Health Technology Assessment Review had already identified reference pricing and related PBS processes as areas needing reform, according to reporting on the dispute.[4][5] The MS episode supplied the case study: a rule intended to avoid overpayment can move so abruptly that it endangers continuity of access before the system has a measured way to test the clinical and market consequences.

One obvious answer is to say the companies should simply take the lower price. Sometimes that will be right. Public schemes cannot let every incumbent product veto a cheaper competitor’s effect on reimbursement. Another obvious answer is to exempt high-efficacy MS therapies from sharp benchmark effects. That is too easy in the other direction. A system that cannot harvest savings from lower-priced entrants will gradually lose the fiscal room that makes broad subsidized access possible.

The harder task is deciding when a lower-priced entrant should reset a class immediately, when transition rules should soften the movement, and when clinically meaningful differences inside a group justify a more granular approach. That is not an argument against reference pricing. It is an argument for noticing when reference pricing has stopped behaving like a calibrated instrument and started behaving like a trapdoor.

What the Cliff Revealed

The Briumvi listing exposed a weakness that was always latent in the design. Therapeutic grouping works best when the medicines inside the group are sufficiently substitutable for pricing purposes and when the price movement gives patients, clinicians, suppliers, and the payer enough time to adjust. In the MS case, the new benchmark appears to have arrived with a force that the affected manufacturers treated as commercially unacceptable and that patient groups experienced as an access threat.

There are further complications sitting just outside the immediate July decision. Ocrevus faces eventual biosimilar competition as patent protection expires in coming years, with timing varying by jurisdiction. That future competition may lower costs regardless of this particular dispute. But future biosimilars do not answer the 2026 design question: how should the PBS handle a lower-priced entrant today when the benchmark effect may destabilize existing subsidized therapies before the market has naturally adjusted?

Australia avoided the immediate rupture in July 2026. Patients were not told, at the end of that week, to find $33,000 a year or change therapy overnight. That matters. But the episode also showed that a public pricing system can be both rational and destabilizing. The PBS protected the budget by following a recognizable reference pricing logic; it protected patients by pausing the access consequence through a rapid review. What remains unresolved is whether the same architecture can preserve therapeutic plurality when the next lower-priced comparator changes the reference point.

References

- PBS dispute could leave MS patients with huge bills for crucial drugs Ocrevus and Kesimpta, ABC News, July 8, 2026

- New relapsing remitting MS treatment, Briumvi, listed on the PBS, MS Australia

- Multiple sclerosis patients given PBS lifeline amid drug pricing dispute, ABC News, July 16, 2026

- Life-changing MS drugs to stay on the PBS. So why are others under threat – and how is Trump involved?, The Guardian, July 16, 2026

- PBS future of two leading MS therapies hangs on pricing decision, Medical Republic

- Multiple sclerosis economic burden exceeds $3 billion as prevalence soars, MS Australia, December 2025

- MS Prevalence and Health Economic Impact in Australia 2025, MS Australia

Comments

Join the discussion with an anonymous comment.