AI Medical Companies Investment Landscape 2026

AI Medical Companies Investment Landscape 2026Executive Summary: The Three Forces Reshaping AI Medical Company Investment

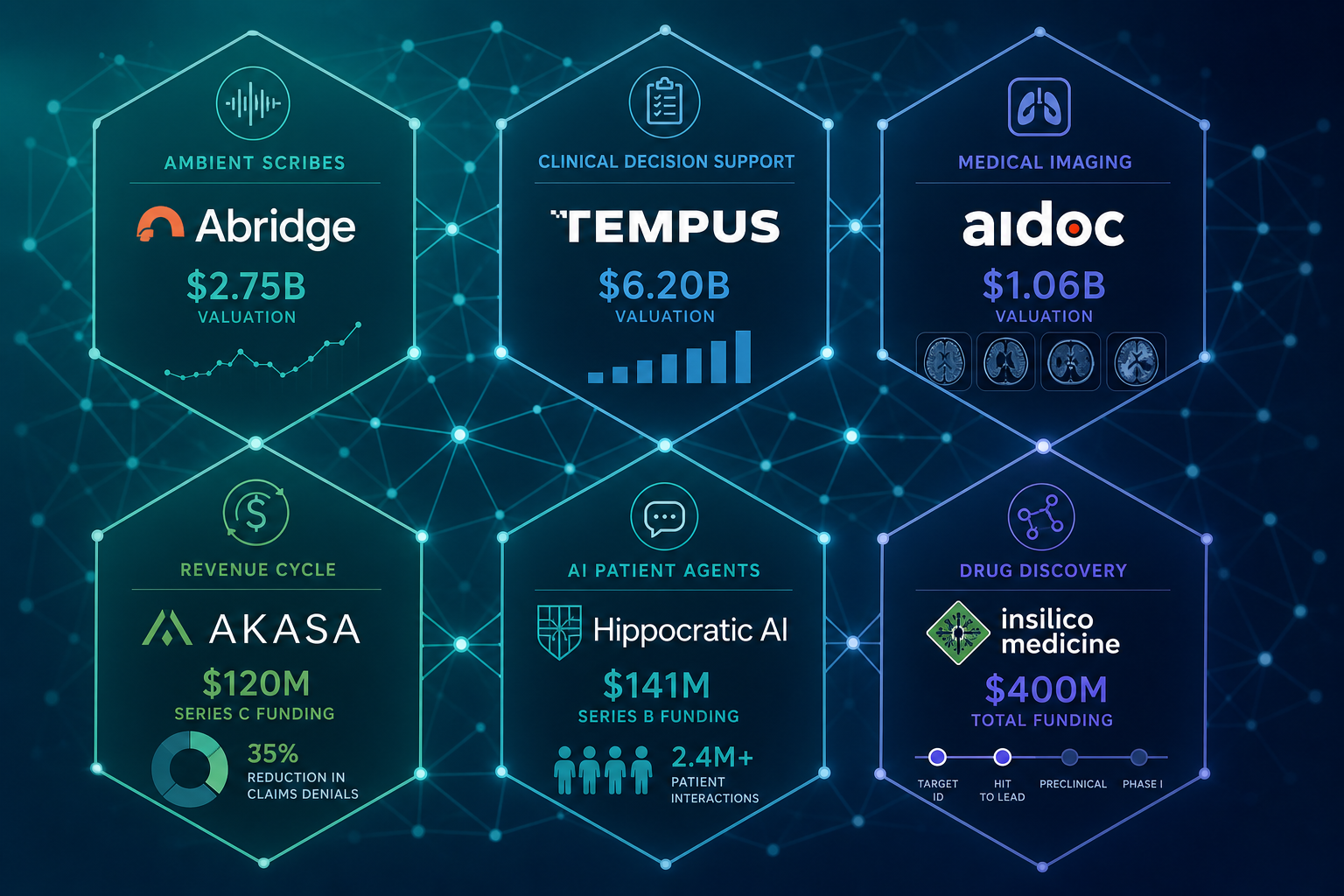

The investment landscape for AI medical companies in 2026 is not a simple story of more money flowing into a hot sector. It is a story of structural realignment driven by three distinct forces. First, AI-native startups captured a majority of health tech venture capital for the first time, absorbing 55% of the $14 billion deployed in 2025, according to Bessemer Venture Partners' State of Health AI 2026 report. Second, a phenomenon BVP terms the "Health AI X Factor" — a combination of hyper-growth velocity, revenue durability, and AI-native productivity — is compressing the time it takes for companies to reach $100 million in annual recurring revenue from a decade to three to five years, justifying billion-dollar valuations at earlier stages. Third, a surge in merger and acquisition activity, reaching 400 global health tech deals in 2025, is reshaping the competitive map as platform players absorb point solutions.

Yet a counterintuitive tension defines the public markets: the Health Tech 2.0 cohort — companies like Tempus, Waystar, and Hinge Health — grew at a median of 67% year over year in 2025, more than three times the rate of the BVP Emerging Cloud Index, but traded at a 10–20% discount on an enterprise-value-to-revenue basis. This "trust gap" — rooted in regulatory uncertainty, adoption friction, and reimbursement complexity — is the central analytical puzzle for investors evaluating the sector.

Macro Funding Picture: AI Captures the Majority of Health Tech Capital

The headline figure from 2025 is unambiguous: health tech venture capital totaled $14 billion, and AI-enabled companies took the majority share for the first time. According to BVP's analysis, AI's share of health tech funding rose from 29% in 2022 to 37% in 2024 and then jumped to 55% in 2025. Rock Health's H1 2025 data, cited by multiple sources, shows AI startups hauled in $4 billion of the $6.4 billion raised in the first half alone — 62% of all digital health funding.

The magnitude of the shift becomes clearer when you examine deal-level dynamics. The average health tech deal size rose 42% year over year, from $20.7 million in 2024 to $29.3 million in 2025. AI-enabled startups raised 83% more per deal than their non-AI counterparts. In Q1 2025 alone, the American Hospital Association reported that digital health funding surged 47% over Q4 2024, with mega-rounds of $100 million or more reaching $2.5 billion across 11 deals — and AI startups secured 8 of those 11 mega-rounds.

| Metric | 2022 | 2024 | 2025 |

|---|---|---|---|

| AI share of health tech funding | 29% | 37% | 55% |

| Total health tech VC deployed | ~$12B (est.) | ~$13B (est.) | $14B |

| Average deal size | ~$16M (est.) | $20.7M | $29.3M |

| AI premium per deal vs. non-AI | N/A | N/A | 83% |

| Global health tech M&A deals | ~280 (est.) | 350 | 400 |

Comments

Join the discussion with an anonymous comment.