Introduction: The Health AI Inflection Point

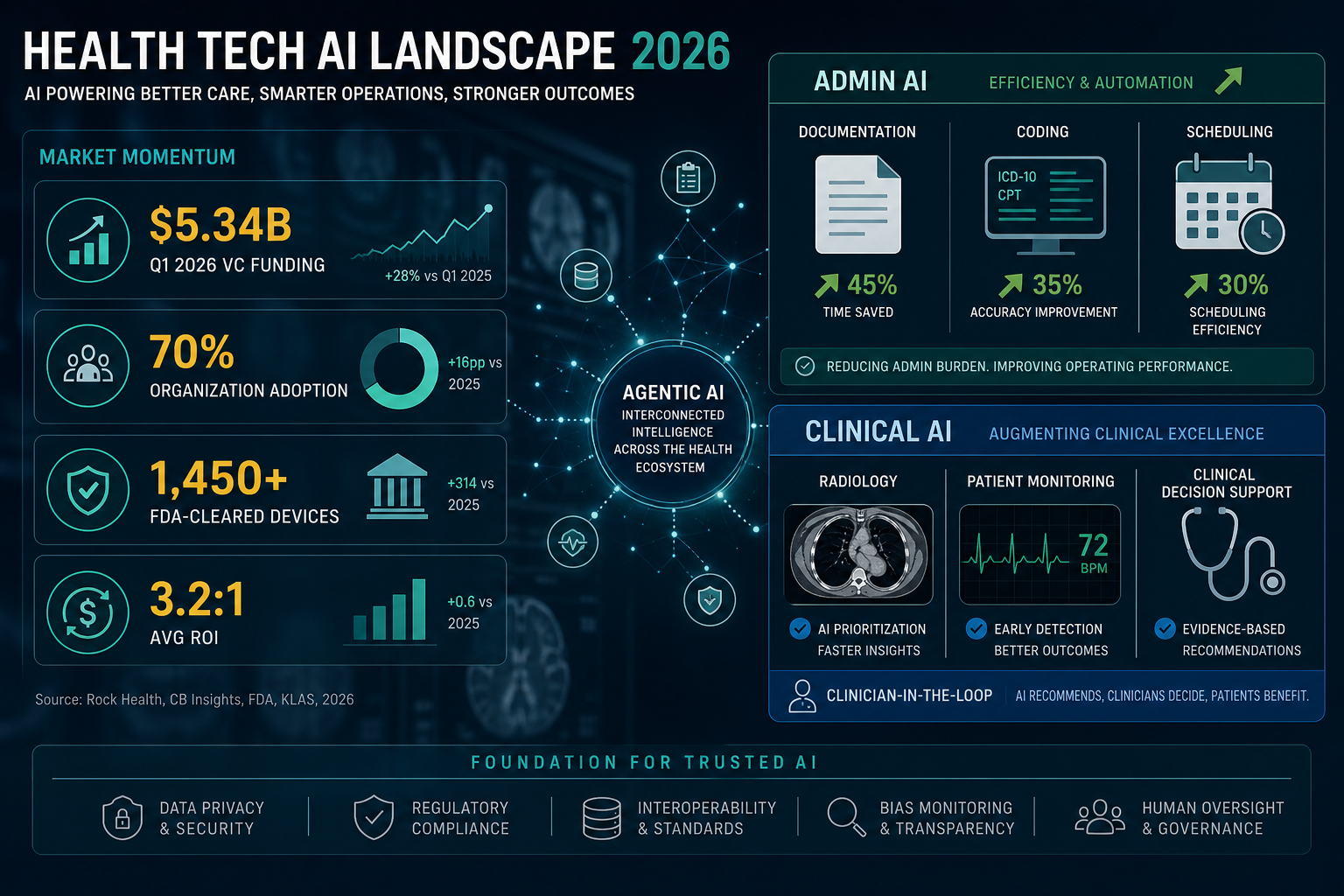

By mid-2026, health tech AI has crossed a threshold that few in the industry predicted even three years ago. It is no longer a pilot project or a speculative line item on a hospital budget. It is infrastructure. The numbers that define this moment are striking: global market estimates range from $36 billion to $56 billion, US digital health venture capital hit $5.34 billion in Q1 2026 alone, and 70% of healthcare organizations report active AI use. Yet these headline figures obscure a more complicated reality.

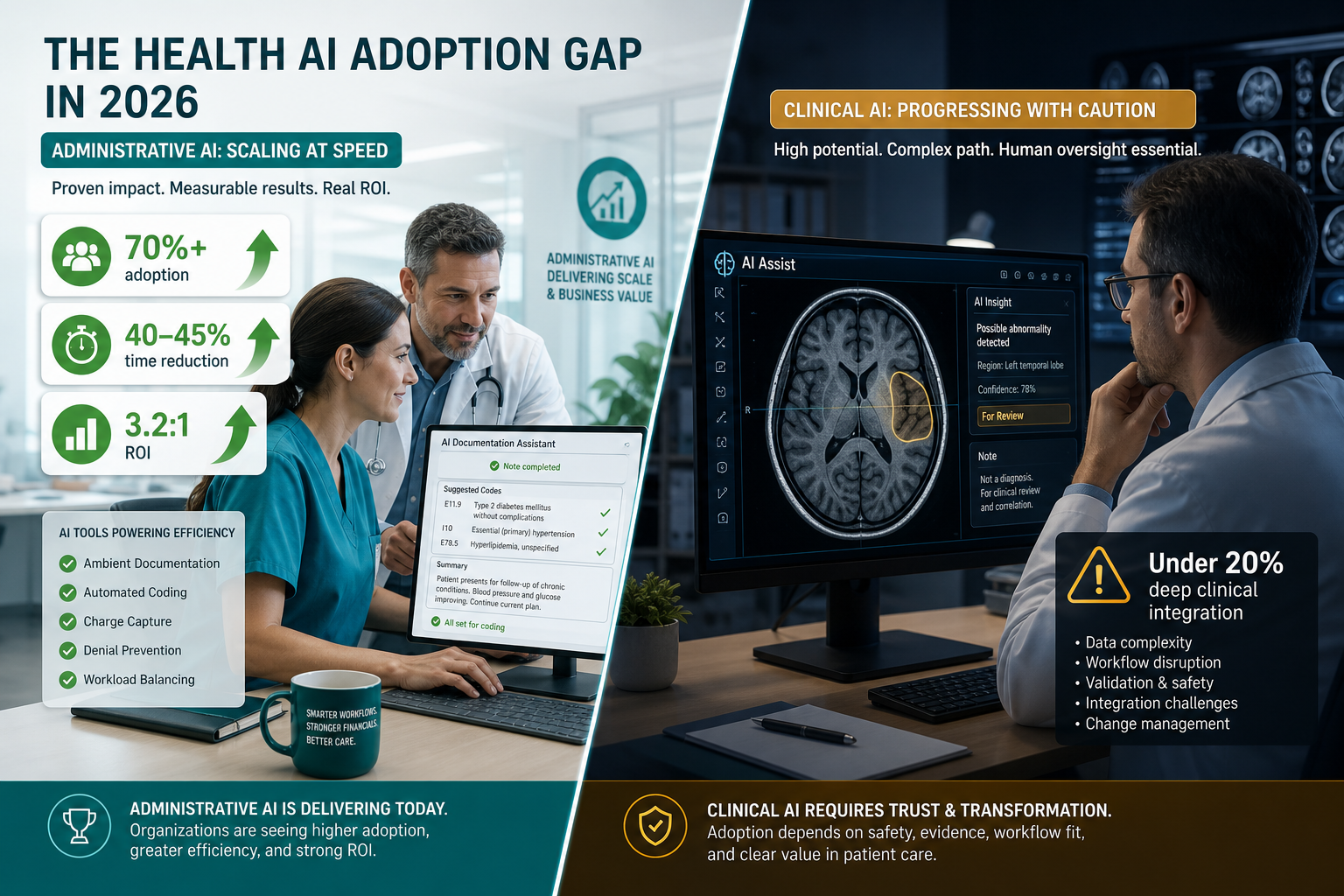

The same data that signals rapid adoption also reveals a sharp divide. Administrative and workflow AI — ambient scribes, revenue cycle tools, prior authorization automation — is delivering measurable returns, with average ROI reported at 3.2:1 and payback periods of 12 to 18 months. Meanwhile, deep clinical integration, where AI directly supports diagnosis and treatment decisions, remains stuck below 20% across institutions. The market is not a monolith. It is a two-speed system, and the gap between the two speeds carries real consequences for investment strategy, deployment planning, and regulatory readiness.

This article reconciles the major data streams — market sizing, venture funding, adoption surveys, ROI evidence, and regulatory records — to give healthcare executives, health IT leaders, and investors a cross-referenced picture of where health tech AI stands in mid-2026. The goal is not to celebrate the numbers but to understand what they actually mean, where they conflict, and where the real work remains.

Market Size: Reconciling the $36–56 Billion Range

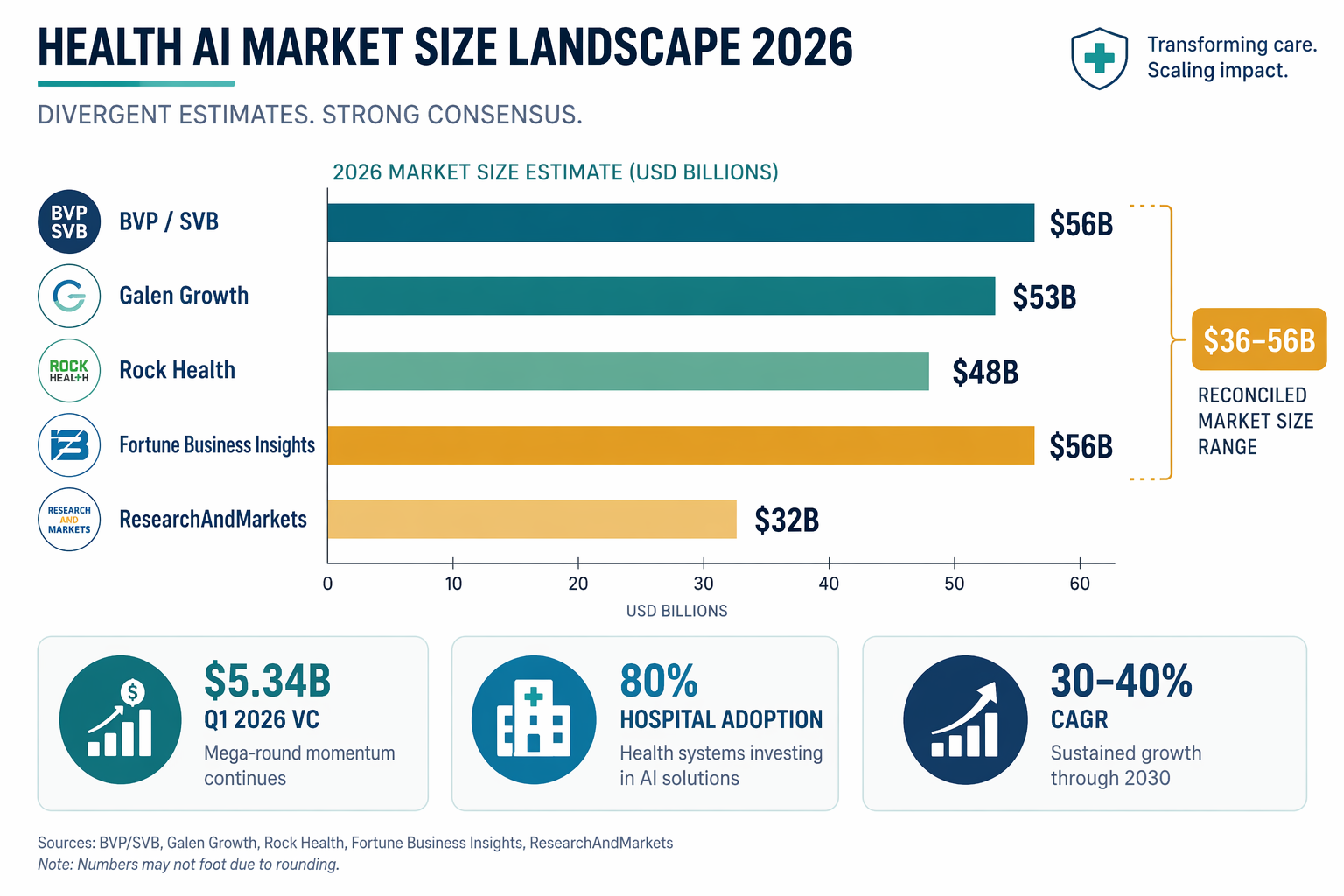

Anyone attempting to size the global AI healthcare market in 2026 quickly encounters a problem: the estimates do not agree. ResearchAndMarkets pegs the 2026 figure near $32 billion, while Fortune Business Insights places it at $56 billion. The spread is not a sign of bad data — it reflects fundamentally different definitions of what counts as "AI in healthcare." Narrower definitions include only clinical AI software and SaMD. Broader ones sweep in AI-enabled medical devices, drug discovery platforms, revenue cycle automation, and even consumer wellness tools.

The most commonly cited range among the sources reviewed for this analysis — Bessemer Venture Partners, Galen Growth, Rock Health, and the consolidated Uvik dataset — converges on $36 billion to $56 billion for 2026. The variance matters less than the trajectory. All major forecasts project a compound annual growth rate between 30% and 40%, pushing the market past $100 billion by 2030. Even the most conservative estimates place the sector among the fastest-growing segments in healthcare technology.

| Source | 2026 Estimate | Methodology Scope |

|---|---|---|

| Fortune Business Insights | $56.01B | Broad: includes AI software, hardware, and services across clinical and administrative use cases |

| BVP / SVB (implied range) | $45–50B | Health AI X Factor framework; includes AI-native health tech companies and platform plays |

| ResearchAndMarkets | $31.97B | Narrower: focused on AI software and platforms in clinical settings |

| Uvik (consolidated) | $36–56B | Reconciliation of multiple analyst reports; cites ~$120B forecast by 2028 at 35–40% CAGR |

For practical purposes, the $36–56 billion range is a useful working estimate. It captures the sector's scale without overstating precision. What matters more than the exact number is the consensus that the market is growing at a pace that outruns most other healthcare technology segments, and that the growth is being driven by a specific set of forces: generative AI adoption, agentic workflow automation, and the expansion of FDA-cleared clinical AI devices.

Investment Landscape: Record Funding and the AI Share Shift

The capital flowing into health tech AI in 2026 tells a clearer story than the market size estimates. In Q1 2026 alone, US digital health startups raised $5.34 billion across 105 deals, according to Galen Growth's HealthTech Alpha Premium data. That figure captures 76% of all global digital health VC for the quarter. Rock Health's parallel tracking, which uses a slightly different methodology and coverage scope, reports $4 billion for the same period — still the strongest Q1 since the pandemic peak and up from $3 billion in Q1 2025.

The more telling metric is AI's share of total health tech funding. Bessemer Venture Partners reports that AI companies captured 55% of all health tech funding in 2025, up from 37% in 2024, 33% in 2023, and 29% in 2022. For every dollar invested in AI companies overall in 2025, $0.22 went to healthcare AI startups. AI has moved from a thematic sub-sector to the dominant allocation category.

- 18 mega-rounds ($100M or more) closed in Q1 2026, with an average deal size of $56.2 million — up 144% from $22.8 million in Q1 2025.

- The Disease Agnostic AI layer — platforms that apply AI across multiple clinical conditions — absorbed $2.88 billion across 47 deals.

- Health Management Solutions led sector-specific investment at $892 million across 19 deals.

- Key Q1 2026 deals include: Whoop $575M Series G, Devoted Health $366M Series F, Verily $300M Series E, and OpenEvidence $250M Series D.

- The Health Tech 2.0 cohort — companies like Waystar, Tempus, Hinge Health, and HeartFlow — added $36.6 billion in fresh market capitalization during 2024–2025.

The IPO window has also reopened for health tech companies with clear AI narratives. Waystar's public listing and the market reception to Tempus and Hinge Health signal that public market investors are willing to reward companies that can demonstrate AI-driven revenue growth and operational efficiency. This is a meaningful shift from the 2022–2023 period, when health tech IPOs were rare and often poorly received.

For a deeper look at the companies leading this investment wave, see our analysis of top AI healthcare companies in 2026, which profiles the major players across clinical, administrative, and platform categories.

Adoption at Scale: 70%+ Organizational Use and the GenAI Surge

NVIDIA's second annual "State of AI in Healthcare and Life Sciences" survey, published in early 2026, provides the most comprehensive snapshot of organizational adoption. Among the key findings: 70% of respondents' organizations are actively using AI, up from 63% in 2024. Generative AI and large language models are the dominant workload, with 69% of organizations using them, up from 54% the prior year. Agentic AI — systems that can autonomously execute multi-step workflows — is being used or assessed by 47% of organizations.

The adoption figures from other sources reinforce the trend. Consolidated data from Uvik reports that approximately 80% of hospitals now use AI in at least one clinical or operational function, and roughly 89% of healthcare executives report AI usage within their organizations. Bessemer Venture Partners notes that 67% of clinicians use AI tools daily, and over 90% use them at least weekly.

The fastest-adopted AI application in healthcare history may be the ambient AI scribe. As of March 2025, 92% of provider health systems were deploying, implementing, or piloting AI-powered ambient documentation tools. That adoption speed is roughly five times faster than the early EHR adoption curve. The reason is straightforward: the ROI case is immediate and measurable. Early adopters report 10–15% revenue capture improvements in the first year through better coding and documentation, alongside 40–45% reductions in physician charting time.

Consumer adoption is also accelerating. BCG's survey of 13,353 internet-connected adults across 15 countries, conducted in November 2025, found that nearly 60% of consumers are already using AI for personal health purposes. OpenAI reports that over 40 million people use ChatGPT daily for healthcare questions. Healthcare is the second-fastest-growing enterprise AI segment for OpenAI, with 8x customer growth from 2024 to 2025.

ROI Evidence: Where the Returns Are Real

The ROI data for health tech AI in 2026 is stronger than many skeptics predicted. The consolidated average across multiple sources places the return at 3.2:1, with payback periods of 12 to 18 months. NVIDIA's survey reports that 85% of executives say AI is helping increase revenue, and 80% say it is reducing costs. Among respondents, 85% expect their AI budgets to increase this year, with 46% planning increases of more than 10%.

| ROI Metric | Reported Value | Source / Context |

|---|---|---|

| Average ROI on healthcare AI investments | 3.2:1 | Uvik (consolidated from multiple industry reports) |

| Typical payback period | 12–18 months | Uvik; consistent with BVP and NVIDIA survey findings |

| Physician documentation time reduction | 40–45% | Uvik; BVP reports similar ranges for ambient scribe deployments |

| Clinical note error rate reduction | 25–30% | Uvik |

| Revenue capture improvement (AI scribes) | 10–15% in first year | BVP, based on early adopter health system data |

| Executives reporting AI-driven revenue increase | 85% | NVIDIA 2026 State of AI in Healthcare survey |

| Executives reporting AI-driven cost reduction | 80% | NVIDIA 2026 State of AI in Healthcare survey |

Specific deployment case studies add texture to the aggregate numbers. Deloitte's survey of 100 US healthcare technology executives, published in September 2025, documents several early-adopter successes. MUSC Health deployed AI agents that now complete 40% of prior authorizations without human involvement. Sentara Health used agentic AI for virtual nursing, ambient documentation, and care management, reclaiming thousands of nursing hours. Stanford Health Care piloted ChatEHR, a system that brings personalized real-world evidence into the EHR at the point of care.

The ROI evidence is strongest in administrative and workflow applications — the areas where AI replaces or augments repetitive, high-volume tasks with clear time and cost baselines. Clinical AI applications, by contrast, face a higher evidence bar. For a detailed examination of what the clinical trial literature actually shows, see our overview of clinical evidence for AI in healthcare.

The Maturity Gap: Under 20% Deep Clinical Integration

The most important single data point in this entire landscape may be the one that gets the least attention: under 20% of institutions report sustained, high-success use of AI in core clinical diagnosis. This figure, drawn from the consolidated Uvik dataset and consistent with the pattern across multiple sources, reveals the central tension of health tech AI in 2026.

Administrative AI — documentation, coding, scheduling, prior authorization — has achieved broad deployment because the workflows are well-defined, the ROI is measurable in weeks or months, and the regulatory barriers are lower. Clinical AI, by contrast, must navigate FDA clearance, evidence generation, workflow integration, liability concerns, and clinician trust. These barriers are not insurmountable, but they slow the adoption curve substantially.

The FDA's AI/ML-enabled medical device list provides a concrete illustration of the specialty concentration. As of late 2025, the FDA had authorized approximately 1,450 AI/ML-enabled medical devices. Of those, roughly 76% are in radiology. Cardiology, neurology, and pathology account for most of the remainder. The distribution reflects both the maturity of imaging data for AI applications and the relative clarity of the regulatory pathway for imaging devices. It also means that clinical AI in primary care, emergency medicine, and most procedural specialties remains nascent.

The maturity gap has practical implications for anyone making investment or procurement decisions. An organization that deploys an AI scribe today can expect a clear, near-term return. An organization that deploys an AI diagnostic tool for a non-radiology specialty faces a longer timeline, higher integration costs, and less certainty about clinical outcomes. The two categories should not be evaluated on the same criteria.

For a detailed breakdown of clinical AI applications by specialty, including evidence quality and regulatory status for each, see our structured brief on clinical applications and deployment realities.

Cautionary Signals: Governance Gaps and Shadow AI

The rapid adoption of generative AI in healthcare has created a governance problem that most organizations are only beginning to address. Wolters Kluwer's 2026 healthcare AI trends report, drawing on insights from its clinical and technology leadership, identifies shadow AI — the use of unapproved or ungoverned AI tools by clinicians and staff — as a critical risk. Peter Bonis, Chief Medical Officer at Wolters Kluwer, notes that clinical-grade generative AI can be a trusted copilot when embedded in daily workflows and rigorously validated. The operative phrase is "when embedded and validated." Without those conditions, the same tools introduce risks around data privacy, clinical accuracy, and regulatory compliance.

Alex Tyrrell, CTO at Wolters Kluwer, predicts that 2026 will be "the year of governance," as C-suites play catch-up to clinicians who have rapidly adopted generative AI applications. Holly Urban, MD, adds that shadow AI surged across healthcare organizations in 2025, and that leaders in 2026 will be forced to rethink AI governance models and implement formalized organization-wide frameworks.

Deloitte's survey reinforces the governance concern. While 61% of healthcare technology executives report that their organizations are already building and implementing agentic AI initiatives, and 85% plan to increase investment over the next two to three years, the governance frameworks to manage these systems are not keeping pace. Agentic AI — systems that can autonomously execute multi-step workflows across clinical and administrative domains — introduces new failure modes that traditional governance models were not designed to handle.

HealthTech Magazine's 2026 trends analysis flags additional obstacles: trust, affordability for smaller organizations, and the tension between strong cybersecurity and efficient clinical workflows. Data governance is described as "easier said than done" but remains a foundational requirement for any AI strategy.

For a deeper look at the regulatory frameworks that govern AI data access and interoperability, see our analysis of the ONC Information Blocking Rule and its implications for AI systems and agentic workflows.

Outlook: 2026 Predictions and Strategic Imperatives

The major analyst and consulting firms that track health tech AI have published their 2026 predictions, and while the specifics vary, the directional signals are consistent. The following synthesis draws on forecasts from Bessemer Venture Partners, Deloitte, BCG, and Wolters Kluwer.

- CMS will launch experiments with clinical AI payment codes. BVP predicts that 2026 will see the first Medicare payment models specifically designed to reimburse AI-assisted clinical services, starting with radiology and cardiology. This would mark a fundamental shift from AI as a cost center to AI as a billable service.

- Cash-pay consumer AI will accelerate faster than reimbursement-driven adoption. BVP notes that RadNet's study of 747,604 women found 36% opted to pay $40 out-of-pocket for AI-enhanced mammography, with the overall cancer detection rate 43% higher for those who chose it. Consumer willingness to pay directly for AI-enhanced care may outpace the reimbursement system.

- Agentic AI investment will surge, but governance will lag. Deloitte's finding that 61% of health tech executives are already building agentic AI systems, combined with Wolters Kluwer's warning that governance frameworks are not keeping pace, points to a year of rapid deployment followed by regulatory and operational catch-up.

- Consumer readiness will force health systems to act. BCG's survey of 13,353 consumers across 15 countries found that most respondents would prefer to engage with either AI alone or a human augmented by AI rather than a human alone. BCG's four "no regrets" imperatives for health system CEOs include embedding AI in the digital front door and empowering patients with agentic access.

- Governance will become a board-level issue. Wolters Kluwer's prediction that 2026 will be "the year of governance" reflects a growing recognition that AI oversight cannot remain an IT department function. Formalized organization-wide frameworks, including AI use registries, vendor validation protocols, and clinician training requirements, will become standard.

For executives and investors, the strategic imperatives that emerge from this outlook are clear. First, invest in governance infrastructure now, before regulatory mandates force reactive compliance. Second, prioritize AI applications with measurable ROI in well-defined workflows — the administrative AI that is already delivering 3.2:1 returns — while building the clinical AI capabilities that will define the next phase. Third, prepare for a regulatory environment that will shift from permissive to structured, with CMS payment codes, FDA post-market surveillance requirements, and state-level AI transparency laws all on the horizon.

The health tech AI market in 2026 is not a bubble, and it is not a disappointment. It is a two-speed system where the fast lane — administrative and workflow AI — is delivering real, measurable returns, and the slow lane — deep clinical integration — is making steady but uneven progress through regulatory and evidence barriers. The organizations that succeed will be the ones that understand both speeds and plan accordingly.

For profiles of the companies shaping this landscape, see our coverage of Google Health's AI portfolio and Waystar's revenue cycle AI platform, two bellwethers for the clinical and administrative sides of the market respectively.