Hospital revenue leakage is a better starting point for AI in hospital financial guidance and stock analysis than the usual claim that AI will “save time.” Time savings can vanish inside an understaffed billing office. Leakage shows up closer to the income statement: claims denied, charges missed, payer contracts under-enforced, accounts reworked, and dollars collected late or not at all.

HFMA estimated in January 2026 that hospitals lose 3% to 5% of net revenue annually to revenue leakage, and the problem is not confined to one failure point in the revenue cycle. The same article cited denial prediction, charge capture, and contract-compliance analytics as AI use cases already tied to measurable financial recovery in case examples, not just generic automation claims.[1]

That distinction matters for investors. A hospital CFO does not buy revenue cycle AI because a demo screen looks intelligent. The purchase has to survive a budget meeting, a baseline challenge, an implementation delay, and usually a 12-month return requirement. The investable question is therefore narrower than “Will healthcare adopt AI?” It is whether the AI layer can repeatedly convert messy hospital workflows into financial results that executives can measure, defend, and renew.

Where AI Touches Hospital Cash

Revenue cycle AI is appealing because it operates in places where the economic unit is already visible. A denied claim has a dollar value. A missing charge can be traced to a clinical event. A payer underpayment can be compared against a contract term. That does not make attribution easy, but it does give finance teams a cleaner testing ground than many clinical AI deployments.

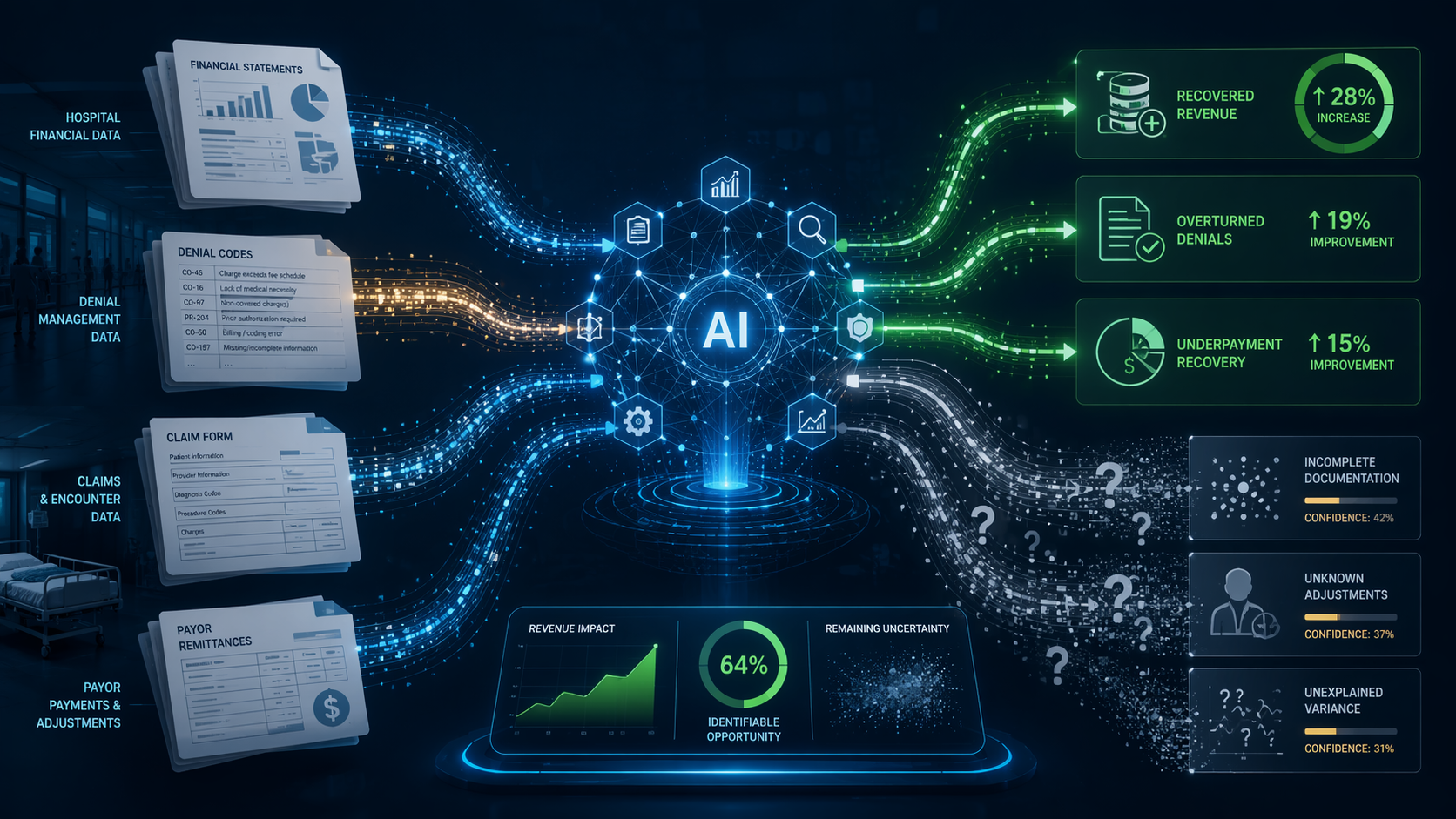

Denial prediction is the cleanest example. HFMA described case examples in which AI denial prediction reduced denial rates by 18% to 22% within six months and improved first-pass yield from 85% to 92%.[1] Those are not soft productivity metrics. A higher first-pass yield means fewer claims returning to staff for appeal, correction, or write-off review. It also shifts cash timing, because claims that pass on the first submission do not wait behind a rework queue.

The case that will get the most attention is a Midwest health system with $3 billion in revenue. According to HFMA, the system deployed denial prediction AI, reduced denials by 18%, and added $40 million in net revenue in one year.[1] That figure is compelling precisely because it is specific enough to test. A buyer can ask what baseline denial rate was used, which denial categories changed, whether staffing or payer mix moved at the same time, and whether the gain repeated after the first year.

The case should not be treated as an industry average. It is a single case summary, not a peer-reviewed study or an independently audited benchmark. But it does point to the kind of evidence that matters: a financial result large enough to appear in a CFO conversation, tied to a workflow where the pre-AI and post-AI states can be compared.

For readers who want a deeper split between production-ready revenue cycle AI and overclaimed use cases, ClinicalMind’s 2026 evidence review of revenue cycle AI functions is the more granular companion piece. The key point here is that the investor lens should start with functions where a hospital can observe avoided denials, recovered charges, or enforced contract terms.

Charge capture and contract compliance are less glamorous, and more useful

Charge capture is one of those hospital finance categories that rarely sounds like a technology story until the missed dollars are counted. HFMA cited a large academic medical center that used natural language processing-based charge capture to identify $12 million in missed charges over six months.[1] The technology claim is not that AI “understood medicine” in the abstract. It is that documentation, orders, and billable events contained patterns that existing manual review did not reliably catch.

Contract-compliance analytics sits even closer to the CFO’s office. HFMA described an integrated delivery network in Texas that used AI to uncover recurring underpayments, renegotiated contracts, and secured an 8% reimbursement increase worth more than $25 million annually.[1] The same article noted that hidden underpayments inside payer contracts can erode collections by as much as 11%, citing HealthAsyst.[1]

There is an important difference between finding a missed charge and changing the hospital’s recurring margin profile. The former may be a one-time cleanup, especially if the tool is applied to a backlog. The latter requires continuous monitoring, payer-specific rule interpretation, workflow adoption, and finance-team trust. For stock analysis, recurring detect-and-correct value is more relevant than a large first-year recovery number that may not recur at the same level.

| AI revenue cycle use case | What the cited evidence measures | Why investors should care |

|---|---|---|

| Denial prediction | 18% to 22% denial-rate reductions within six months; first-pass yield improvement from 85% to 92% | Links AI to avoidable rework, cash timing, and net revenue recovery |

| NLP-based charge capture | $12 million in missed charges identified over six months at a large academic medical center | Shows AI finding billable activity that manual processes missed |

| Contract compliance | Recurring underpayments identified; 8% reimbursement increase worth more than $25 million annually in a Texas IDN case | Tests whether AI can enforce payer economics, not just automate back-office tasks |

| Cost-to-collect reduction | Industry estimates of 30% to 60% reduction through AI-enabled revenue cycle optimization | Matters only if the reduction converts into durable operating leverage rather than absorbed workload |

Cost-to-collect is the most tempting metric to overread. HFMA cited industry estimates that AI-enabled revenue cycle optimization could reduce cost-to-collect by 30% to 60%.[1] In a clean software model, that would flow neatly into margin. In a hospital, it may first show up as fewer open roles, slower growth in outsourced collections spend, or staff shifted to higher-value exceptions. That can still be economically meaningful, but analysts should ask where the savings actually land.

Deloitte’s hospital AI benchmarks broaden the picture beyond revenue cycle. The firm estimated that AI can improve avoidable days by 4% to 10%, operating room utilization by 10% to 20%, and reduce denials due to missing information by 4% to 6%.[2] Those figures matter because hospital financial performance is not only a billing-office problem. Capacity, documentation quality, and utilization discipline all feed the same margin conversation.

The Public-Company Lens: Growth Looks Software-Like, Trust Does Not

The operating evidence explains why public-market investors are watching Health Tech 2.0 companies more closely in 2026. Bessemer Venture Partners reported that Health Tech 2.0 public companies grew average revenue by 67% in 2025, compared with 19% for the EMCLOUD software index. Yet the same cohort traded at 7.2x EV/revenue versus 8.0x for comparable cloud software companies, a discount that persisted despite faster growth.[3]

That comparison should not be flattened into “healthcare AI stocks are cheap.” The more useful reading is that growth and productivity signals look increasingly software-like, while valuation still reflects healthcare-specific execution risk. Hospitals buy slowly. Implementations touch legacy systems. ROI attribution is contested. A vendor may produce strong results in one health system and still struggle to repeat them across a different payer mix, EHR configuration, staffing model, or governance structure.

BVP also reported that AI-native healthcare companies achieve $500,000 to more than $1 million in annual recurring revenue per full-time employee, compared with $200,000 to $400,000 for traditional healthcare SaaS companies.[3] ARR per FTE is not a hospital outcome metric, but it is a useful operating signal. If a company can deliver complex healthcare workflows with fewer service-heavy implementation requirements, investors can start to underwrite a different margin structure.

Tempus AI, Waystar, R1 RCM, Hinge Health, and Stryker belong on a watchlist for different reasons. They are not interchangeable “AI healthcare stocks.” Tempus is watched for AI-enabled data and diagnostics economics. Waystar and R1 RCM sit closer to administrative and revenue cycle workflows where hospital financial ROI can be tested. Hinge Health is a different version of healthcare technology execution, tied to digital musculoskeletal care and employer or payer value narratives. Stryker brings a medtech and procedural platform angle rather than a pure software one.

The common question is not whether each company uses AI language. It is whether AI improves a measurable economic unit in a way customers renew, expand, and reference. For revenue cycle-exposed companies, that unit may be denial avoidance, collections lift, first-pass yield, or cost-to-collect. For clinical or procedural platforms, the unit may sit elsewhere. The stock work starts by matching the claimed AI advantage to the customer’s budget owner and the customer’s measurable return.

No source in the current evidence set proves that hospital AI performance causes stock outperformance for any specific public company. The linkage is a synthesis: hospital finance teams are beginning to report measurable AI-assisted improvements, while public Health Tech 2.0 companies are showing strong growth and productivity metrics. That is enough to build an analytical framework. It is not enough to declare a direct stock-price causal chain.

The Trust Gap Is the Valuation Question

The strongest argument against a simple bullish narrative is the adoption math. A Qventus report covered by Becker’s in April 2026 found that only 4% of health systems had achieved scaled AI ROI. The same report said 74% of CIOs must demonstrate ROI within a year, and 80% say they have difficulty measuring it.[4]

The 4% figure is not a reason to dismiss the category. It is a reason to be selective. If only a small share of health systems can show scaled returns, the companies that help customers move from pilot evidence to repeatable ROI may deserve more attention than companies with broader but less measurable AI claims. Scarcity matters, especially when the buyer’s finance team is under pressure to prove payback quickly.

The 80% measurement difficulty is the more important number. Measurement failure can come from several places: an unstable baseline, poor attribution between technology and workflow redesign, insufficient integration into billing operations, payer behavior changes, or a pilot that works only because a high-performing local team carried it. A vendor may truthfully report a good result and still leave the next buyer unsure whether the result is transferable.

This is where hospital financial guidance and stock analysis meet. A hospital CFO wants to know whether a product will improve cash recovery or reduce avoidable cost inside the budget window. An investor wants to know whether that proof will shorten sales cycles, improve retention, support pricing, or expand account penetration. Both questions depend on the same middle layer: credible measurement.

The source limitations are not minor. HFMA’s revenue cycle examples are useful but not independently audited industry averages. BVP’s State of Health AI report comes from a venture capital firm with a natural interest in the category’s upside. The Qventus and Becker’s report is based on more than 60 IT leaders, a sample that may not represent all health systems. Deloitte’s benchmark estimates are helpful, but benchmarks still need local validation before they become a hospital’s operating plan.[1][2][3][4]

Those caveats do not erase the signal. They define the due diligence. For an investor, the question is less whether AI can produce a striking hospital case study and more whether a company can make the case study boring: repeatable baseline, repeatable implementation, repeatable measurement, repeatable renewal.

What to Track Before Treating AI as a Margin Lever

A disciplined watchlist for public Health Tech 2.0 companies should begin with operating evidence, not ticker enthusiasm. The practical test is whether the company can show that AI changes a financial workflow in a way the customer can measure before and after deployment.

- Baseline quality: whether the company defines denial rates, first-pass yield, cost-to-collect, underpayment recovery, or charge capture before implementation rather than after a result is found.

- Attribution discipline: whether reported improvement separates AI contribution from staffing changes, payer mix changes, contract renegotiation, cleanup projects, or parallel consulting work.

- Workflow integration: whether recommendations enter the daily queue used by billing, coding, utilization, or contract teams, rather than remaining in a dashboard.

- Repeatability across sites: whether outcomes appear across multiple hospitals, specialties, payer relationships, and EHR configurations.

- Renewal and expansion behavior: whether customers expand usage after the first ROI period, which is a stronger signal than a pilot announcement.

For companies closest to revenue cycle workflows, the best disclosures will not be the broadest AI statements. They will be mundane financial metrics: fewer preventable denials, higher clean-claim rates, faster cash conversion, lower outsourced collection burden, more recovered underpayments, and a clearer line from product usage to net revenue impact. If those metrics become standardized, valuation discounts may narrow. If they remain trapped in isolated case studies, public-market skepticism will be harder to dislodge.

Market data should also be dated. The growth and EV/revenue comparisons cited here reflect early-to-mid 2026 conditions, and multiples can change quickly with rates, earnings revisions, or a single disappointing implementation cycle. A better denial rate at a hospital does not automatically create a higher stock price. It becomes relevant to equity value only if it supports durable revenue growth, pricing power, gross margin expansion, lower service intensity, or stronger retention for the vendor.

That is the real opportunity in hospital AI: not the existence of impressive pilots, but the conversion of financial improvement into a legible, repeatable buying argument. The companies worth watching are the ones that help hospitals prove the return as much as produce it.

References

- Why AI is such a promising tool for eliminating a hospital’s revenue leakage, HFMA, Jan 2026.

- Artificial intelligence in hospitals: financial performance and clinical burnout, Deloitte.

- State of Health AI 2026, Bessemer Venture Partners.

- Only 4% of health systems achieve scaled AI ROI: report, Becker’s Hospital Review, Apr 2026.

Comments

Join the discussion with an anonymous comment.