In health AI budget meetings, “ROI” now carries too much weight for one word. A physician champion may mean fewer pajama-time notes. Finance may mean lower overtime, cleaner claims, or incremental revenue. A vendor may mean time theoretically released back to the organization. Those are not the same return.

That distinction matters because procurement pressure has caught up with deployment. In McKinsey’s Q4 2025 survey of 150 healthcare leaders, half said their organizations had implemented generative AI, 82% of implementers expected positive ROI, and 45% said they had quantified returns ranging from less than 2x to 4x investment.[1] Menlo Ventures’ 2025 survey of 700-plus healthcare executives found that 22% had implemented domain-specific AI tools, a sevenfold increase from 2024.[2] Meanwhile, AI companies captured 55% of all health tech funding in 2025, up from 37% in 2024, and healthcare AI venture funding reached $10.7 billion that year.[3][4]

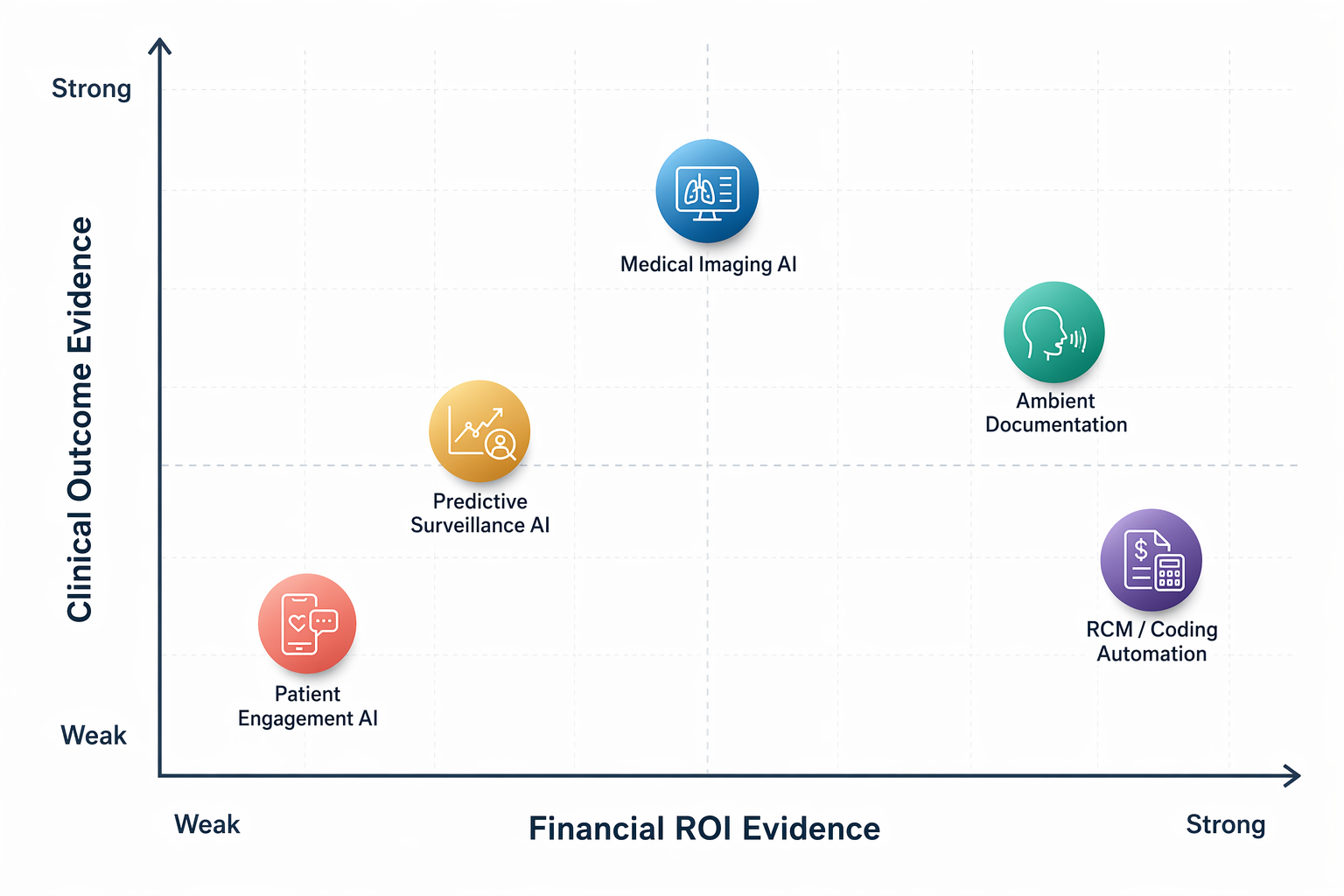

Those numbers explain why health systems are being pitched so aggressively in 2026. They do not prove where health AI companies are delivering return. Once financial ROI, clinical outcomes, user satisfaction, deployment scale, and independent validation are separated, the evidence is uneven: ambient documentation and revenue-cycle automation show the clearest financial ROI signals; imaging AI has stronger clinical-outcome evidence than financial evidence; predictive surveillance and patient engagement remain promising but less replicated.

A useful ROI screen separates four things

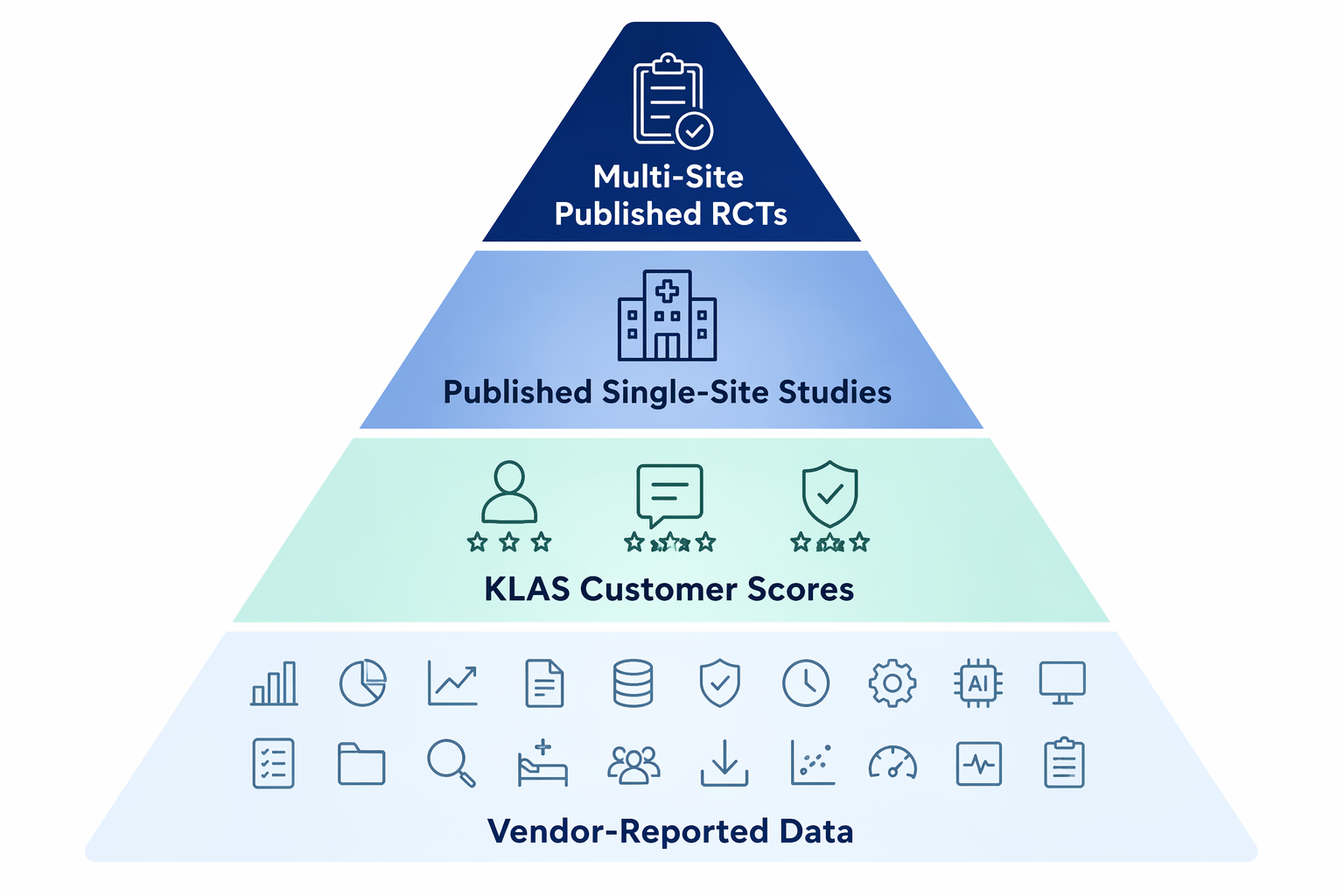

The fastest way to overbuy AI is to treat every favorable metric as the same kind of proof. A KLAS score is useful customer-experience evidence. A vendor case study can show a plausible mechanism. A published clinical study can show outcome change in a defined setting. A multi-site randomized trial carries a different evidentiary weight. A deployment count says something about market reach, but not necessarily about depth of use, active utilization, or net financial return.

| Category | Financial ROI signal | Clinical ROI signal | Main evidence type | Replication strength |

|---|---|---|---|---|

| Ambient documentation | Strongest around time savings; weaker when translated into dollars | Indirect: less documentation burden and potentially better clinician experience | Vendor-reported studies, customer cases, KLAS experience data, large deployments | Moderate; time-savings mechanism is consistent, financial conversion varies |

| RCM and coding automation | Strong where the metric is coding yield, DNFB reduction, or avoided manual work | Limited direct clinical outcome claim | Vendor/customer ROI data, KLAS scores, encounter volumes, case studies | Moderate; measurable workflow but much evidence remains vendor-reported |

| Imaging AI | Mixed; reimbursement and workflow economics vary by modality and payer | Strongest category for published clinical and operational outcome signals | FDA authorization data, large deployments, published outcome studies | Higher for clinical use cases; lower for direct financial ROI |

| Predictive surveillance | Not yet broadly established | Promising in specific published studies, including sepsis | Published trial evidence and health-system implementation reports | Early; needs replication across different systems |

| Patient access and engagement | Promising when tied to scheduling automation, call cost, readmissions, or staffing relief | Early and use-case-specific | Company-reported operational data and early deployment results | Low to moderate; independent validation remains thin |

For readers who need the broader market map before the ROI screen, the companion healthcare AI companies landscape is the better starting point. This article stays with the narrower procurement question: what kind of return has actually been measured, and by whom?

Ambient documentation: visible relief, harder dollar conversion

Ambient documentation is the category where the user pain is easiest to see. The baseline problem is not abstract: physicians spend about one hour on documentation for every five hours of patient care, according to research cited in Menlo Ventures’ 2025 healthcare AI report.[2] A tool that removes clicks, drafts the note, and shortens after-hours charting can feel valuable before anyone opens a spreadsheet.

The evidence base reflects that. Suki has cited an AAFP study reporting a 72% median reduction in documentation time.[5] DeepScribe’s Ochsner case study reported a 75% time reduction and a 98.8 KLAS score.[6] Menlo also pointed to large-scale adoption, including Kaiser Permanente deploying Abridge across 40 hospitals and more than 600 offices.[2] The ambient AI clinical documentation evidence review goes deeper on what peer-reviewed and real-world evidence does and does not show.

The procurement trap is the slide that turns time saved into money saved without showing the operating change. If a physician saves documentation time and sees more patients, the return may be incremental access or revenue. If the same physician leaves earlier, the return may be retention, lower burnout risk, or simply a better workday. If the note requires heavy correction, the time saving may partly move from drafting to editing. These are all real possibilities, but they are different budget arguments.

KLAS scores help here, but only within their lane. A high customer score suggests that customers find the product usable and valuable enough to report favorably. It does not prove reduced burnout, improved coding, higher revenue, or better outcomes. The same caution applies to deployment scale. A health-system logo can mean enterprise use, a specialty rollout, or a limited population of early adopters. The economics depend on how many clinicians use the tool, how often they accept the draft, how much editing remains, and whether the organization changes scheduling, staffing, or retention assumptions around the saved time.

Nuance DAX Copilot, now part of Microsoft Dragon Copilot, sits in the same evidence conversation: valuable to evaluate because of scale and workflow integration, but still requiring a buyer-specific link between documentation relief and financial return. The Nuance DAX Copilot platform profile and the piece on ambient AI scribes in Epic EHR deployments are useful verification paths when the procurement question moves from category-level ROI to implementation detail.

RCM and coding automation: the cleanest financial mechanism, with compliance attached

Revenue-cycle and coding automation has a less glamorous pitch than ambient documentation, but its ROI mechanism is often cleaner. The organization can measure denials, coding yield, discharge-not-final-billed, exception queues, manual coding labor, and claim lag. When a tool improves one of those steps, finance can usually see where the benefit lands.

That is why RCM-focused health AI companies show up strongly in 2026 ROI discussions. SmarterDx has reported an average 5:1 ROI across more than 60 health systems, a figure referenced in both Menlo Ventures’ 2025 report and Bessemer’s 2026 State of Health AI analysis.[2][3] Fathom reports a 95.5 KLAS score and more than 63 million encounters processed.[7] CodaMetrix was named Best in KLAS for Autonomous Coding in 2026.[8] Nym has reported $1.3 million in savings at Inova and a 50% reduction in DNFB in a customer case study.[9]

Those are procurement-relevant metrics, but they still need sorting. A 5:1 ROI claim is not the same as an independently replicated, peer-reviewed financial outcome. A high KLAS score is not the same as coding accuracy under audit. Encounter volume shows operational scale, not necessarily net benefit per encounter. A single customer case can be a useful mechanism check, especially if the baseline workflow was leaky, but it should not be treated as a generalizable guarantee.

The operational question is also different from the ambient documentation question. With autonomous coding, the benefit is not usually “time saved” in the abstract. It is which codes changed, which claims moved faster, which exceptions remained for human review, which denials were avoided, and who signs off when the model is wrong. That last point is not a footnote. Coding automation creates a compliance surface as well as a savings opportunity, which is why the buyer’s evaluation should include auditability, exception handling, payer variation, and medical-record traceability. The AI medical coding compliance guide addresses that part of the decision directly.

This is the category where CFO interest is easiest to understand. The numerator and denominator can be built from existing operational data. But that also means there is less excuse for vague ROI. A health system should be able to ask for baseline DNFB, pre- and post-implementation coding distribution, denial impact, labor redeployment, exception rates, and audit outcomes. If the vendor cannot connect its claimed return to those workflow measures, the claim is not yet finance-grade.

Imaging AI: stronger clinical evidence than direct financial ROI

Imaging AI complicates the ROI picture because it has some of the strongest clinical and regulatory evidence in health AI, while the direct financial case is often less tidy. The category is mature by FDA standards: as of the end of 2025, the FDA had authorized 1,451 AI-enabled medical devices, and 76% were in radiology.[10] That does not mean every device improves outcomes or saves money, but it does show how much of medical AI’s regulated footprint sits in imaging.

Viz.ai is one of the clearer operational-outcome examples. Bessemer’s 2026 analysis cites published data showing a 39.5-minute reduction in time to neurointerventionalist contact across more than 1,700 hospitals, alongside multiple FDA clearances.[3] Aidoc reports deployment in more than 1,600 hospitals and has cited length-of-stay reduction data, with Menlo identifying the company as a scaled example in imaging AI.[2] In breast imaging, a RadNet study of 747,604 women found that 36% paid $40 out of pocket for AI-enhanced mammography, with 43% higher cancer detection using AI and a 21% higher likelihood of detection.[11]

Those are important signals, but they are not all the same kind of return. Door-to-treatment time is a clinical workflow metric with obvious patient relevance. Cancer detection improvement is a clinical-performance signal, and in the RadNet case it also gives a rare look at patient willingness to pay. Length-of-stay reduction could have financial implications, but the value depends on bed capacity, payer mix, discharge constraints, and whether the hospital can actually convert freed capacity into throughput.

The imaging category therefore deserves more confidence on clinical-outcome maturity than on universal financial ROI. A stroke-alert tool that shortens specialist contact time may be compelling even if the finance model is not a simple labor-savings calculation. A mammography add-on with out-of-pocket uptake may work in one population and fail in another. A triage tool may reduce delay but increase downstream work for radiologists or care teams if alerts are poorly tuned. The buyer has to decide whether the return being purchased is faster care, better detection, downstream revenue, avoided adverse events, or capacity improvement.

Predictive surveillance: promising where trials exist, not yet broadly replicated

Predictive AI has lived through enough abandoned early-warning dashboards that buyers are right to ask harder questions. The relevant issue is not whether prediction can work. It is whether the prediction changes a clinical action quickly enough, reliably enough, and with low enough alert burden to improve outcomes.

Bayesian Health is the strongest example in the current evidence set. Menlo Ventures cited a published multi-site randomized controlled trial showing a significant sepsis mortality reduction.[2] That is a different evidence tier from a retrospective model-performance paper or a vendor-reported alert-acceptance rate. It ties the technology to an outcome that matters.

The remaining caution is not small. The trial evidence still needs replication across different health systems, patient populations, staffing models, EHR configurations, and sepsis workflows. An alert that works in one operating model can lose value if the receiving team lacks capacity, if escalation pathways are unclear, or if clinicians learn to ignore it. McKinsey’s survey found that 43% of healthcare leaders cited risk and safety as a barrier to scaling generative AI, and that concern applies with extra force when AI influences clinical surveillance and escalation.[1]

Patient access and engagement: operational signals before independent ROI

Patient access and engagement AI is attractive because the bottlenecks are familiar: unanswered calls, scheduling friction, missed follow-up, avoidable readmissions, and staff who spend too much of the day on repeatable outreach. The ROI case can be real when the tool reduces call volume, automates scheduling, improves follow-up completion, or prevents a costly utilization event. The evidence, however, is still more company-reported and use-case-specific than independently replicated.

Hippocratic AI has reported 30% readmission reductions at WellSpan and UHS, and has said it stress-tested more than 500,000 calls across 7,000-plus clinicians with no severe-harm errors; those figures were cited in Menlo Ventures’ 2025 report and Bessemer’s 2026 analysis.[2][3] Prosper AI has reported more than 60% scheduling automation and roughly 50% call-cost reduction in company-reported data.[12]

Those are meaningful claims to investigate, especially in access centers where staffing shortages and call abandonment are visible every day. But the procurement posture should remain narrower than the marketing language. A safety stress test conducted by the company is not the same as external post-deployment safety validation. A readmission reduction at named systems is not the same as a multi-site replicated effect across service lines. A call-cost reduction may be compelling if the organization can reduce overtime, redeploy staff, or improve access; it is weaker if the automated work simply creates new exception queues elsewhere.

Vendor momentum is not the same as buyer evidence

The startup-heavy nature of the current market makes evidence discipline harder, not less important. Menlo reported that 85% of generative AI spend flows to startups, excluding general-purpose LLMs.[2] That can be healthy: startups often attack miserable workflows faster than incumbents do. It also means buyers see more young companies with impressive pilots, limited longitudinal data, and pressure to turn early traction into enterprise contracts. The broader startup-versus-incumbent dynamics are covered in the competitive landscape of AI in healthcare.

Evidence should be read in layers. Vendor-reported data belongs in the conversation when the workflow mechanism is plausible and the baseline is visible. KLAS data helps assess customer experience and implementation satisfaction. Published single-site studies can show whether an effect survived a real clinical environment. Multi-site trials and replicated outcomes carry more weight because they reduce the chance that the result depended on one unusually prepared team.

That is also why adoption metrics need careful labels. McKinsey’s 50% implementation figure refers to generative AI among surveyed healthcare leaders.[1] Menlo’s 22% figure refers to domain-specific AI tools among surveyed healthcare executives.[2] Physician use of any AI, enterprise deployment of an AI product, and paid use of a domain-specific system are different measurements. Treating them as interchangeable makes the market look more settled than it is. For broader evidence and policy context around generative AI specifically, see the 2026 generative AI in healthcare evidence review.

Where the evidence is strongest

The most defensible category-level conclusion is not that one group of health AI companies has “won.” It is that the return mechanisms differ enough that they should not be compared on a single ROI slide.

- Ambient documentation has the clearest user-facing relief and repeated time-savings signals, but financial ROI depends on what the health system does with the saved time.

- RCM and coding automation has the cleanest financial measurement path because the affected workflows already produce auditable operational and revenue metrics.

- Imaging AI has the strongest clinical and regulatory maturity, especially in radiology, but the financial model varies by use case, payer environment, and capacity constraints.

- Predictive surveillance has credible promise where published trial evidence exists, but generalization depends on clinical workflow replication.

- Patient access and engagement AI has operationally plausible ROI, but much of the current evidence remains company-reported or early-stage.

Health AI ROI is no longer hypothetical. It is also not evenly proven. The strongest procurement cases start with the buyer’s bottleneck, identify the specific mechanism of return, and then match the evidence type to the size of the budget decision. A time-savings study, a KLAS score, a customer case, an FDA clearance, a deployment count, and a randomized trial can all be useful. They should not be asked to do the same job.

References

- Generative AI in healthcare: current trends and future outlook, McKinsey, Q4 2025

- 2025: The State of AI in Healthcare, Menlo Ventures, 2025

- State of Health AI 2026, Bessemer Venture Partners, 2026

- AI Healthcare Funding Rises In 2025, Crunchbase News, 2025

- AAFP Study, Suki

- Ochsner Case Study, DeepScribe

- Fathom Autonomous Medical Coding, Fathom

- 2026 Best in KLAS Awards, KLAS, 2026

- Inova Case Study, Nym

- Numbers From the FDA Show Radiology Is Maintaining Its Lead, The Imaging Wire, March 2026

- AI-Enhanced Mammography Study, RadNet, 2025-2026

- Prosper AI Scheduling Automation Data, Prosper AI

Comments

Join the discussion with an anonymous comment.