Searching for the “top healthcare AI companies” in 2026 should not produce one clean league table. It should produce a sorting problem. A stroke triage platform, an oncology data company, an ambient documentation vendor, an autonomous coding tool, and a drug discovery platform do not win by the same evidence standard. Some need FDA authorization and algorithm-level performance data. Some need to prove that physicians actually save time. Some need to show that a hospital’s OR block utilization, coding throughput, or capacity management improves in production.

That distinction matters because market enthusiasm is now broad enough to make almost any large vendor look like a leader. Global healthcare AI estimates for 2026 range from about $36.67 billion to $56.01 billion depending on scope, with Grand View Research estimating roughly $50.7 billion, Fortune Business Insights estimating $56.01 billion, and MarketsandMarkets estimating $36.67 billion.[1][2][3] Digital health funding tells a similar story: Rock Health reported that AI-enabled companies received 54% of all digital health funding in 2025, up from 37% in 2024, and AI deals carried about a 19% size premium over non-AI deals.[4]

Those numbers explain why the category is noisy. They do not tell a CMIO, radiology chair, revenue-cycle director, or procurement committee which claims deserve trust.

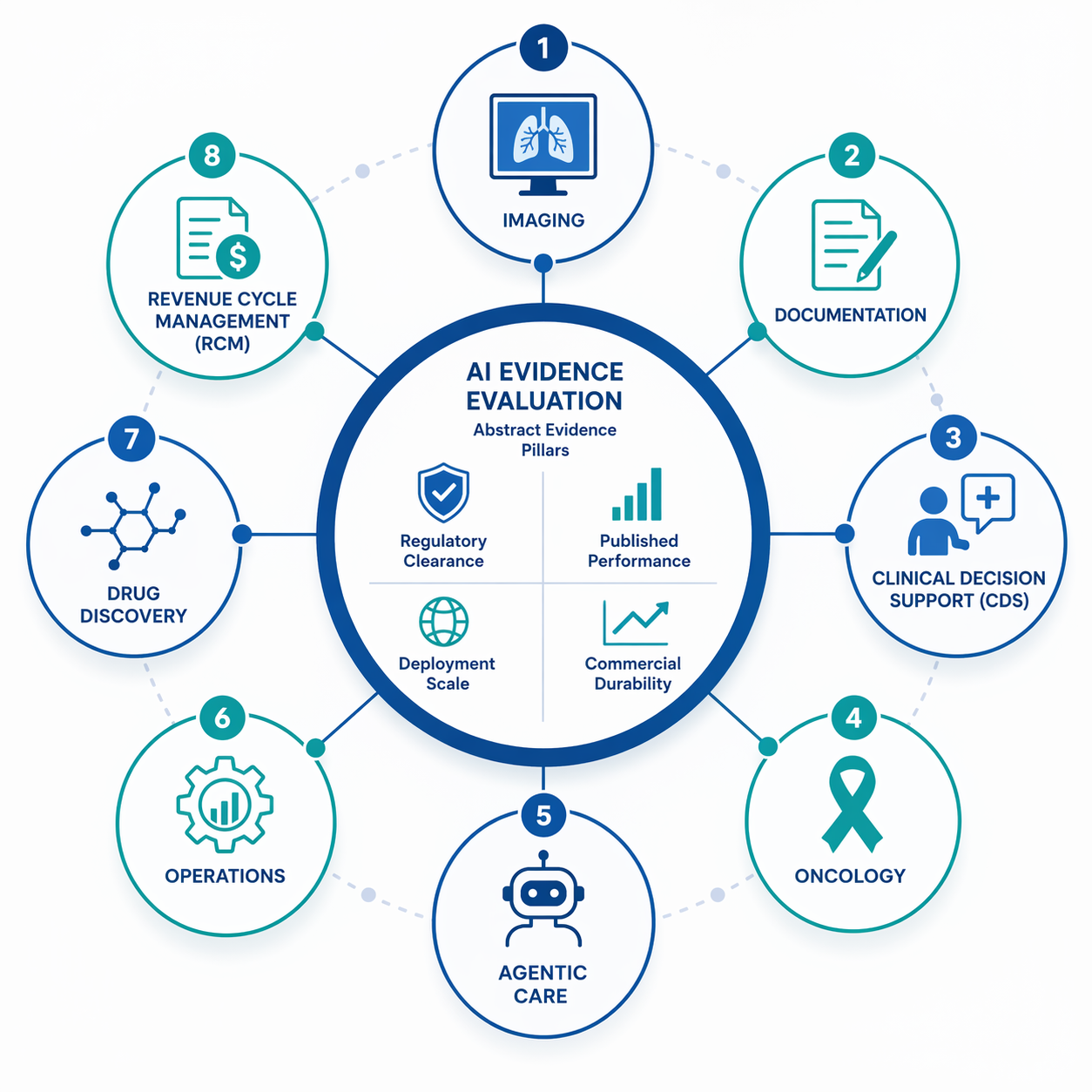

A Practical Evidence Map, Not a Top-10 List

The useful question is not which company is “best.” It is which company leads a specific function, and whether that claim rests on evidence appropriate to that function. FDA authorization is meaningful for imaging and diagnostic software, but it is not a clinical outcomes trial. Published sensitivity, specificity, or AUC can be important, but a model that performs well in one setting may still fail to change workflow. Deployment scale matters, but hospital count can reflect sales reach as much as clinical value.

The FDA’s AI/ML-enabled medical device list is still the most visible regulatory reference point, with 1,451 authorized AI/ML-enabled devices by the end of 2025 and roughly 76% in radiology, but the list is keyword-matched rather than a complete registry of every AI device.[5] That is why FDA status should be treated as one evidence pillar, not a finish line. For a deeper discussion of the gap between device authorization and clinical-trial evidence, see 1,451 FDA-Cleared AI Devices: Why Only 2% Have Clinical Trial Evidence.

| Function | Companies to watch | What leadership depends on | Evidence status in Q3 2026 |

|---|---|---|---|

| Clinical decision support | OpenEvidence | Clinician usage, trusted medical content, EHR distribution | Reported $12B valuation, Epic embedding, and about 18M clinical consultations in Dec. 2025; usage is company-reported and not outcomes validation.[6] |

| Ambient documentation | Abridge, Ambience | Workflow relief, adoption depth, documentation quality, expansion into coding and RCM | Abridge reports 250+ health systems and a $5.3B valuation; Ambience raised a $243M Series C and is cited in connection with Houston Methodist coverage.[6][7] |

| Medical imaging | Aidoc, Viz.ai, GE HealthCare | FDA clearance scope, algorithm-specific performance, hospital deployment, time-to-treatment impact | Aidoc reports a multi-condition foundation triage model with 14 findings, 97% sensitivity, 98% specificity, 100M+ patient cases, and 1,000+ hospitals; Viz.ai reports 1,700+ hospitals and faster stroke time-to-treatment; GE HealthCare leads by FDA authorization count.[5][6][7][8][9] |

| Precision oncology and pathology | Tempus AI, PathAI | Data assets, public financial durability, pharma adoption, diagnostic authorization, validation depth | Tempus reports $1.27B FY25 revenue, 45M+ de-identified records, and 95% of top oncology pharma companies as customers; PathAI reports 15M+ annotated samples and AISight Dx FDA 510(k) and CE Mark authorization.[6][9][10] |

| Patient-facing agentic care | Hippocratic AI | Safety controls, scope limitation, deployment governance, regulatory pathway clarity | Hippocratic AI is reported at about a $3.5B valuation, but the regulatory and outcomes evidence is thinner than in device-heavy categories.[6][11] |

| RCM and administrative infrastructure | CodaMetrix | Coding accuracy, automation rate, denial impact, customer retention, workflow integration | CodaMetrix is reported as #1 in 2026 Best in KLAS for autonomous coding; the category benefits from a lower regulatory bar and immediate ROI pressure.[6] |

| Drug discovery | Recursion, Insilico Medicine | Pipeline maturity, pharma partnerships, clinical-stage progress, reproducible discovery claims | Leadership is partnership- and pipeline-dependent; clinical proof takes longer than in deployed hospital software.[10][12] |

| Hospital operations | Qventus, LeanTaaS | Capacity gains, OR utilization, staffing and throughput metrics, reproducibility across sites | Important operational category with lower regulatory scrutiny; clinical impact is usually indirect and harder to compare across hospitals.[9] |

The table is deliberately uneven. Imaging has a regulatory and performance vocabulary that revenue-cycle automation does not. Ambient documentation can be valuable without FDA clearance. Drug discovery may have enormous strategic value before it produces a bedside clinical result. A useful vendor assessment keeps those differences visible instead of flattening them into one score.

Medical Imaging: The Most Mature Category, and Still Not Simple

Medical imaging is the closest healthcare AI has to a mature clinical software market. It has the largest FDA footprint, clearer task boundaries, and a familiar buyer: radiology and acute-care service lines that already understand imaging workflow, triage queues, PACS integration, and false-positive burden. It is also where lazy ranking becomes most misleading.

Aidoc is one of the strongest examples of multi-pillar leadership. The company is reported to have the first FDA clearance for a multi-condition foundation triage model covering 14 findings, with reported 97% sensitivity and 98% specificity, more than 100 million patient cases, and deployment across more than 1,000 hospitals.[5][6] That combination matters: regulatory clearance, performance metrics, and deployment breadth point in the same general direction, even if each pillar has limits.

The limit is that “Aidoc” is not one clinical claim. A pulmonary embolism triage model, an intracranial hemorrhage model, and a multi-condition triage system should be assessed at the level of the algorithm, workflow, patient population, and operational consequence. Sensitivity and specificity answer one question. Whether the alert changes time-to-treatment, reduces misses, avoids alert fatigue, or improves downstream outcomes is a separate question.

Viz.ai illustrates the same point from a different angle. It is reported to be deployed in more than 1,700 hospitals, and secondary coverage cites an approximately 66-minute faster time-to-treatment for stroke.[8][9] That is the kind of operational metric that health systems should care about. It is also not a universal proof statement about every Viz.ai algorithm, every site, or every care pathway. Stroke coordination is a particular use case with a particular urgency profile.

GE HealthCare complicates the “top company” label in another way. ITN reported that GE HealthCare tops the FDA list by AI authorization count.[8] Clearance count is a real signal of regulatory experience and portfolio breadth. It is not the same thing as being the strongest deployed AI triage company, the best-performing model developer in a given finding, or the vendor most likely to change a hospital’s acute-care workflow.

For imaging, then, the more honest answer is plural. Aidoc looks like a leading clinical AI deployment company because it combines clearance, reported performance, and hospital scale. Viz.ai remains a major care-coordination and acute-workflow player, especially in stroke. GE HealthCare is a regulatory portfolio leader by authorization count. Readers who want a fuller radiology-specific vendor landscape can use AI Medical Imaging Companies in 2026: A Use-Case-Driven Market Landscape as the deeper companion.

Precision Oncology: Tempus Has Scale, but Pathology Has Its Own Evidence Rules

Precision oncology is not a mirror image of imaging. The evidence is less about one algorithm flagging one radiology finding and more about data depth, molecular testing, clinical context, pharma usefulness, and whether a platform becomes part of oncology decision infrastructure. That makes Tempus AI one of the most important companies in healthcare AI, while also making its leadership harder to reduce to a single clinical-performance statistic.

Tempus is reported as the most valuable public healthcare AI company by market capitalization, at about $14 billion, with $1.27 billion in FY25 revenue, 83% annual growth, 126% net revenue retention, more than $1.1 billion in contract value pipeline, more than 45 million de-identified records, more than 400 petabytes of data, and 95% of top oncology pharma companies as customers.[6] Those figures are company-reported and should be checked against public filings, but the pattern is still notable: Tempus has commercial durability, data assets, and pharma penetration at a level few healthcare AI companies can claim.

That does not make every Tempus product clinically proven in the way a narrow FDA-cleared imaging algorithm might be. The company’s strength is platform-like: testing, data, oncology intelligence, and pharma-facing evidence generation. A health system evaluating Tempus should therefore ask different questions than it would ask of a stroke triage vendor. Which oncology workflows are affected? Which data are returned to clinicians, and when? Which recommendations are decision support rather than automation? Which claims are based on internal data assets, public filings, customer adoption, or peer-reviewed studies?

PathAI introduces another evidence profile. The company is reported to have more than 15 million annotated samples and more than 450 board-certified pathologists involved in model training, and its AISight Dx has FDA 510(k) clearance and CE Mark authorization for primary diagnostic use.[9][10] That is materially different from a company whose story rests only on computational pathology ambition. Authorization for diagnostic use matters.

The caution is that independent validation remains limited in the cited secondary sources.[10] Pathology AI also depends on scanner infrastructure, lab workflow, specimen handling, pathologist acceptance, and integration with existing diagnostic responsibility. A diagnostic platform can be technically impressive and still face slower adoption than software that removes a daily documentation burden.

Precision oncology is also where category boundaries are starting to collapse. Tempus has moved deeper into pathology AI through its acquisition of Paige, while pathology companies increasingly position themselves as data infrastructure, pharma partners, and diagnostic workflow platforms rather than single-use AI tools. The result is not one oncology AI winner. It is a set of companies trying to own different layers of oncology evidence and workflow.

Ambient Documentation: The Evidence Standard Bends, but It Does Not Disappear

Ambient documentation is where a strict medical-device evidence framework starts to bend. An AI scribe does not need to prove lesion detection performance. It needs to reduce documentation burden, fit into clinical workflow, avoid introducing unsafe note errors, protect privacy, and make the economics work. Absence of FDA clearance does not automatically weaken a documentation vendor. It simply changes what procurement should demand.

Abridge is the leading example of why this category has scaled so quickly. The company is reported to be used by more than 250 health systems and to carry a $5.3 billion valuation.[6] That kind of adoption does not prove clinical benefit, but it does indicate that the pain point is immediate. Physicians feel documentation burden every day. Health systems can see whether notes are produced faster, whether clinicians accept the output, whether coding and billing workflows improve, and whether the tool becomes embedded deeply enough to be hard to replace.

Ambience belongs in the same conversation because it is reported to have raised a $243 million Series C and is associated with Houston Methodist in 2026 trend coverage.[7] The company’s importance is not only transcription. The broader commercial movement is from note generation into clinical documentation improvement, coding support, and revenue-cycle adjacency. That expansion can make a documentation vendor stickier, but it also raises the stakes: once a tool touches coding, billing, and clinical record quality, error monitoring becomes more than a usability issue.

For readers who need terminology and workflow distinctions across scribes, coding, and CDI, see NLP in Clinical Documentation: AI Scribes, Coding, and Clinical Documentation Improvement. The short version for vendor assessment is this: ask for evidence at the level of the job being automated. Note drafting, specialty-specific documentation, EHR integration, coding support, and CDI are related, but they are not the same claim.

Clinical Decision Support: OpenEvidence Has Distribution, Not Yet Outcomes Proof

Clinical decision support sits between information retrieval and care recommendation, which makes evidence slippery. OpenEvidence is one of the most visible companies in this category. It is reported at a $12 billion valuation, with $735 million raised, embedding in Epic at Sutter, Mount Sinai, and Cedars-Sinai, and about 18 million clinical consultations in December 2025.[6]

Those are impressive distribution and usage claims. They are also company-reported, not independently audited in the cited source, and consultation volume is not the same as patient outcome improvement. A clinician looking up a question through an AI interface may save time, find a useful citation, or reduce cognitive friction. The metric itself does not tell us whether diagnoses improved, treatment changed appropriately, or harm decreased.

The right standard for this category should include source transparency, citation reliability, specialty coverage, EHR workflow fit, monitoring for unsafe answers, and evidence that clinicians use the system appropriately. OpenEvidence may still be a category leader by adoption and distribution. The unresolved question is whether that leadership has moved from usage to measured clinical effect.

Agentic Patient Care Needs a Higher Safety Bar Than Its Valuation Story

Patient-facing conversational agents are attracting attention because the staffing problem is real and the interface is intuitive. Hippocratic AI is the standout name here, reported at about a $3.5 billion valuation and focused on patient-facing conversational AI agents.[6][11]

That valuation does not settle the safety question. Patient-facing agents need evidence about task scope, escalation behavior, clinical guardrails, language coverage, monitoring, and what happens when a patient gives incomplete or misleading information. The leadership standard should be stricter than “the agent can converse” and more specific than “it reduces labor.” It should identify which patient interactions are in scope and which are not.

This is not a reason to dismiss the category. It is a reason to keep the claims narrower than the marketing. A scheduling assistant, post-discharge check-in tool, medication reminder, triage navigator, and autonomous clinical agent carry different risk. Lumping them together under agentic care makes the category sound more mature than the evidence base currently supports.

RCM and Administrative AI: Lower Regulatory Burden, Faster Adoption Logic

Administrative AI rarely gets the prestige of diagnostic AI, but hospitals do not buy only for prestige. Revenue-cycle and coding tools address cost, staffing, denial risk, and throughput. The regulatory bar is usually lower than for diagnostic software, and the ROI case can be more immediate.

CodaMetrix is the clearest company to flag in autonomous coding, reported as #1 in the 2026 Best in KLAS ranking for that category.[6] The relevant evidence standard should include automation rate, accuracy by specialty, coder oversight model, denial impact, audit performance, and how exceptions move through human review. A high-performing coding system should decrease manual work without creating hidden compliance debt.

The category’s growth logic is easy to understand: administrative costs exceed $450 billion annually in the cited market commentary, and tools that reduce rework or improve capture can be evaluated in financial and operational terms.[6] Still, lower regulatory burden is not a free pass. Coding and billing errors have consequences for patients, payers, compliance teams, and revenue integrity.

Drug Discovery and Hospital Operations: Important Markets, Longer Proof Cycles

Drug discovery companies such as Recursion Pharmaceuticals and Insilico Medicine are often included in healthcare AI lists, and they should be, but not because they compete directly with hospital AI vendors. Their evidence cycle runs through target discovery, molecule generation, preclinical work, clinical trials, and pharma partnerships. Secondary market sources consistently place Recursion and Insilico among the leading AI drug discovery companies, but partnership announcements and platform claims should not be confused with approved therapeutic impact.[10][12]

Hospital operations companies such as Qventus and LeanTaaS occupy a different evidence lane. They are associated with capacity management, OR optimization, and operational AI.[9] These tools can matter enormously to hospitals because a delayed discharge, unused OR block, or bottlenecked inpatient unit has real consequences. The evidence is usually local and operational: throughput, utilization, length of stay, staffing burden, and repeatability across sites.

Neither category should be penalized for lacking the same evidence package as a radiology device. They should be judged by whether their claims survive the right operational or pipeline-specific test.

Where the Framework Bends

The strongest healthcare AI companies in Q3 2026 are not simply the most valuable, the most funded, or the most frequently named. They are the companies whose claims hold up when matched to the evidence standard of their function. Aidoc looks strongest when the standard is clearance plus performance plus deployment. Tempus looks strongest when the standard is oncology data scale, pharma adoption, and public-company durability. Abridge looks strongest when the standard is workflow relief and fast health-system adoption.

That is also why a broader catalog can be useful only after the evidence standard is clear. Readers who want more names across the landscape can use AI in Healthcare Companies: A Structured Landscape of Active Developers, while market-sizing assumptions are treated separately in From $39B to $1T: What's Driving and What's Constraining the AI Healthcare Market in 2026. The important move is to avoid letting a company’s category momentum answer a buyer’s evidence question.

The cautionary history still matters. IBM Watson Health remains a useful reminder that brand, ambition, and access to clinical data do not guarantee fit with real care delivery; see 4 Critical Lessons from IBM Watson Health's Failure. But that lesson should not flatten the current market into a morality play about hype. Some companies now have real regulatory clearances, measurable workflow adoption, public financial scale, or operational traction. The unresolved work is separating those signals from promotional noise.

Leadership remains provisional. Category boundaries are blurring, companies are consolidating, and several headline metrics still come from the companies themselves. The best answer to “top healthcare AI companies” is therefore a disciplined map: function first, evidence second, ranking only after the claim has been narrowed enough to test.

References

- Artificial Intelligence In Healthcare Market Size, Share & Trends Analysis Report, Grand View Research.

- Artificial Intelligence in Healthcare Market Size, Share & Industry Analysis, Fortune Business Insights.

- AI in Healthcare Market, MarketsandMarkets.

- 2025 year-end digital health funding overview: A tale of two markets, Rock Health.

- Artificial Intelligence-Enabled Medical Devices, U.S. Food and Drug Administration.

- Top AI Companies in Healthcare, Luca Dezzani, LinkedIn.

- Top healthcare AI trends for 2026, Healthcare Dive.

- GE HealthCare Tops FDA List of AI Authorizations, Imaging Technology News.

- Biotech Startups Using AI for Care Delivery, WeWillCure.

- Top 12 Healthcare AI Companies in the US in 2026, OpenLoop Health.

- Top 9 Companies Building AI Agents in Healthcare 2026, Light-it.

- Top Healthcare AI Companies, NCHStats.

Comments

Join the discussion with an anonymous comment.