The AI Healthcare Market in 2026: A Market Defined by Tension

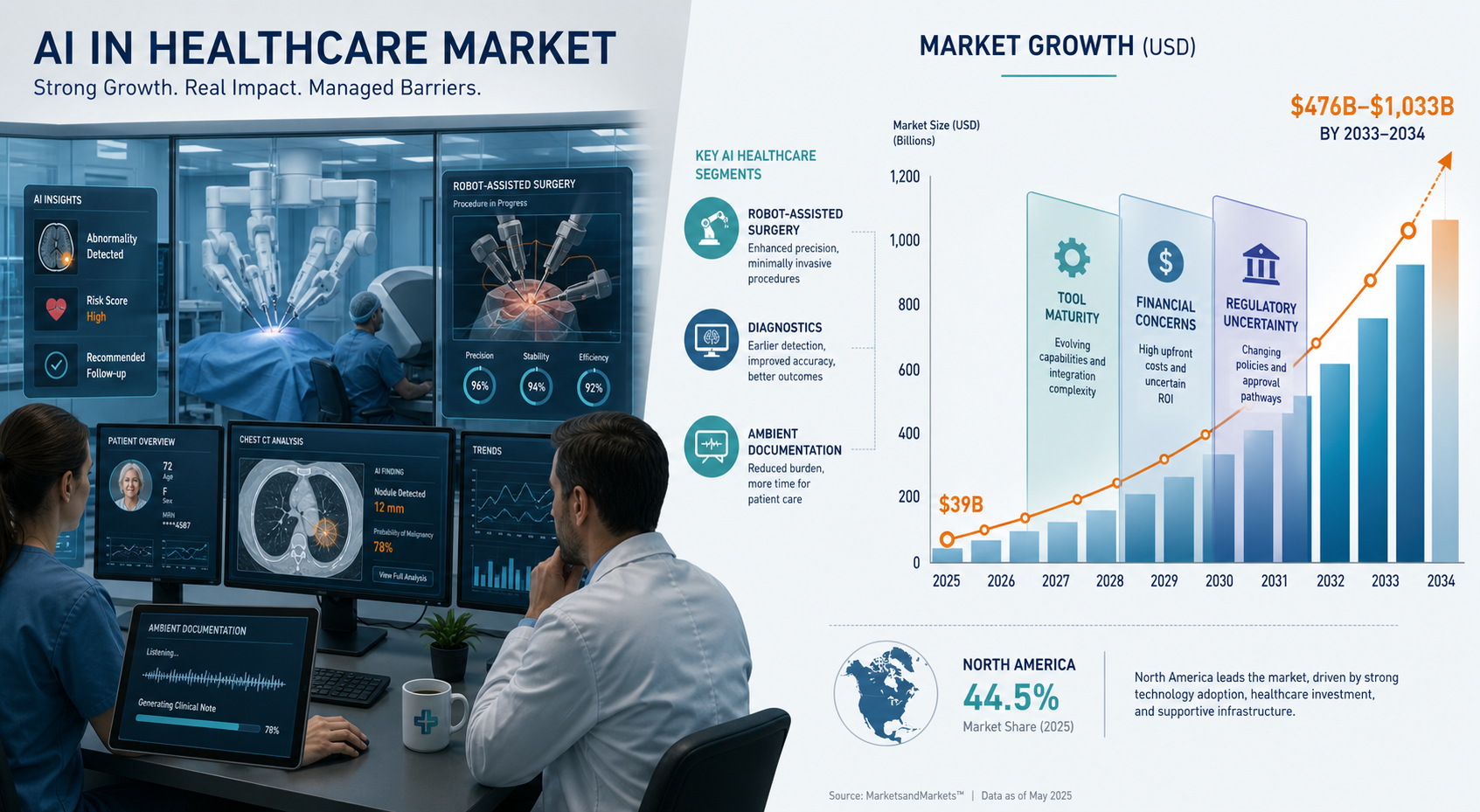

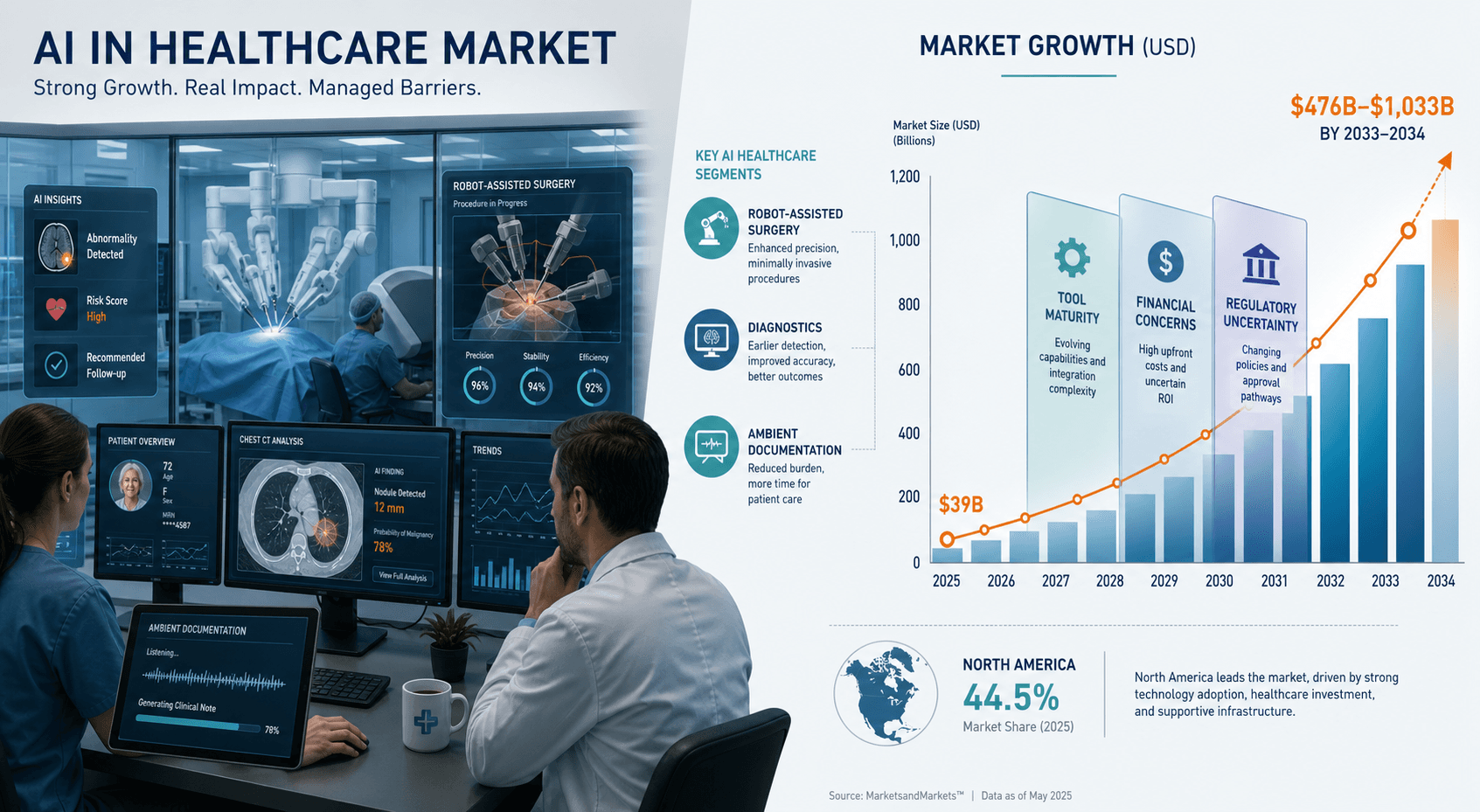

The global AI in healthcare market is projected to grow from $39.34 billion in 2025 to $56.01 billion in 2026, with long-term forecasts reaching as high as $1,033.27 billion by 2034 — a compound annual growth rate of 43.96%, according to Fortune Business Insights. These numbers are arresting. They have fueled a surge of venture investment exceeding $30 billion over the past three years, driven boardroom strategy sessions at every major health system, and prompted regulators worldwide to scramble for frameworks that can keep pace with technological change.

But the market is not a simple growth story. The same data that produces trillion-dollar projections also reveals persistent structural barriers that prevent AI from translating its theoretical promise into widespread, high-impact clinical deployment. A peer-reviewed survey of 43 large U.S. health systems published in JAMIA found that 77% of respondents cite immature AI tools as the top barrier to adoption, 47% flag financial concerns, and 40% point to regulatory uncertainty. These are not minor headwinds — they are fundamental constraints on how deeply and how quickly AI can embed itself into clinical workflows.

This article is built around that central tension. It examines the five converging forces creating genuine market momentum, transparently compares divergent market size projections, analyzes the three structural barriers that limit real-world impact, and provides a segment-level assessment of where drivers outweigh constraints — and where they do not. For investors, health system executives, and strategists navigating this landscape, understanding the tension is more valuable than any single growth projection.

Five Converging Growth Drivers

The market's momentum is not speculative. It is grounded in five concrete, measurable forces that are reshaping healthcare delivery and creating genuine demand for AI solutions.

1. The Clinician Burnout Crisis and Documentation Burden

Clinician burnout has reached crisis levels, and the documentation burden imposed by electronic health records is a primary driver. The JAMIA survey found that 72% of health system leaders rank reducing caregiver burden and improving clinician satisfaction as a top-two AI deployment goal. This is not an abstract aspiration — it is a direct response to workforce attrition, reduced clinical hours, and the growing difficulty of recruiting and retaining physicians. AI scribe deployments have demonstrated a 40–45% reduction in physician documentation time, according to data compiled by Uvik, making ambient documentation one of the fastest-adopted AI use cases in healthcare.

2. FDA Clearance Acceleration

The U.S. Food and Drug Administration has cleared approximately 1,250 AI/ML-enabled medical devices as of May 2025, representing roughly a 5× increase in cumulative device authorizations between 2020 and 2025. Approximately 76% of these cleared devices are in radiology, reflecting the maturity of computer vision applications in medical imaging. This acceleration provides a growing pool of regulatory-authorized tools that health systems can procure with confidence, reducing one dimension of adoption risk.

3. Massive Venture Investment

Over $30 billion has been invested in healthcare AI companies in the past three years alone. This capital has funded product development, clinical trials, regulatory submissions, and commercial expansion across virtually every clinical specialty and operational domain. While investment alone does not guarantee market success, it has created a dense ecosystem of startups and scale-ups that are competing to solve real clinical and operational problems — and that competition is accelerating the pace of innovation.

4. The Generative AI Breakthrough in Ambient Documentation

Generative AI, particularly large language models, has unlocked ambient clinical intelligence — systems that listen to patient-clinician conversations and automatically generate structured clinical notes. The JAMIA survey reports that 100% of responding health systems have adoption activities in ambient notes, with 53% reporting a high degree of success. This is the only AI application category in the survey where a majority of organizations report high success, and it is directly attributable to the generative AI advances of 2023–2025.

5. Rising Chronic Disease Burden and Demand for AI-Assisted Surgery

The global prevalence of chronic diseases — cardiovascular conditions, cancer, diabetes, and neurological disorders — continues to rise, driving demand for AI-assisted diagnostics, surgical robotics, and personalized treatment planning. Robot-assisted surgery captured the largest application segment share at 22.94% in 2026, according to Fortune Business Insights, reflecting the clinical and economic value of precision, minimally invasive procedures. Hospitals and clinics, the largest end-user segment at 42.44% of the market, are investing in AI tools that can improve surgical outcomes, reduce complications, and shorten recovery times.

Market Size Projections: $476B to $1,033B — Why the Range Matters

Market size forecasts for AI in healthcare vary dramatically across analyst firms. The range — from approximately $476 billion by 2033 (SkyQuest) to $1,033.27 billion by 2034 (Fortune Business Insights) — is not a sign of unreliable data. It reflects genuine methodological differences in scope definition, base year selection, and included market segments. Understanding these differences is essential for any decision-maker relying on these projections.

| Metric | Fortune Business Insights | SkyQuest (approx.) |

|---|---|---|

| 2025 Market Value | $39.34 billion | Not directly comparable |

| 2026 Market Value | $56.01 billion | Not directly comparable |

| Long-Term Forecast | $1,033.27 billion by 2034 | ~$476 billion by 2033 |

| Implied CAGR | 43.96% | ~37–40% (estimated) |

| Scope Definition | Broad: includes AI software, hardware, services across clinical and operational domains | Narrower: may exclude certain service or infrastructure segments |

Fortune Business Insights provides the most detailed publicly available breakdown. North America held a 44.50% share in 2025, valued at $17.51 billion, and is projected to reach $22.7 billion by 2026. Europe accounted for $11.05 billion (28.1%) in 2025, projected at $15.73 billion in 2026. Asia Pacific, the fastest-growing region, stood at $8.28 billion (21.05%) in 2025 and is projected at $12 billion in 2026. Latin America and the Middle East & Africa represent smaller but growing shares at $1.6 billion (4.08%) and $0.89 billion (2.26%) respectively in 2025.

The key takeaway is not which number is "correct" — it is that both projections point to a market that will grow substantially over the next decade, but the magnitude of that growth depends on how structural barriers resolve. The higher projection assumes that barriers like tool immaturity, financial concerns, and regulatory uncertainty will be substantially addressed. The lower projection assumes they will persist, limiting the depth of real-world deployment.

Three Structural Barriers That Limit Real-World Impact

The JAMIA survey of 43 U.S. health systems (64% response rate, Fall 2024) provides the most current, peer-reviewed window into the barriers that health system leaders actually face. The survey's respondents represent large non-profit systems with net patient revenue exceeding $1 billion — organizations with the resources and scale to be early adopters. If these barriers are binding for well-resourced systems, they are likely even more acute for smaller or rural health systems.

- AI tool immaturity (77% of respondents): The top-cited barrier. Health systems report that many AI tools do not perform reliably across diverse patient populations, clinical settings, and data environments. Model drift, poor generalizability, and lack of external validation are recurring themes. This is not a perception problem — it reflects the current state of the technology, where most FDA-cleared devices are narrow, task-specific models validated on curated datasets.

- Financial concerns (47%): Health systems struggle to build a clear business case for AI investments. The average ROI on healthcare AI investments is reported at 3.2:1, with a 12-to-18-month typical payback period, but these figures are averages that mask wide variation across use cases. For many tools, the return is indirect — improved clinician satisfaction, reduced burnout, or better patient outcomes — and difficult to quantify in budget cycles.

- Regulatory uncertainty (40%): The regulatory landscape for AI in healthcare remains in flux. While the FDA has accelerated device clearances, the framework for continuous learning algorithms, generative AI, and post-market surveillance is still evolving. Health systems are hesitant to invest in tools whose regulatory status may change, or whose liability implications are unclear.

Beyond these three top barriers, additional constraints include data privacy and cybersecurity risks, EHR integration friction, model drift and governance gaps, and a shortage of AI-literate clinical staff who can evaluate, deploy, and monitor these tools effectively. The Deloitte 2026 U.S. health care outlook found that only one-third of organizations operate AI at scale, while 49% are still experimenting with generative AI and agentic AI, and 18% have not adopted these technologies at all.

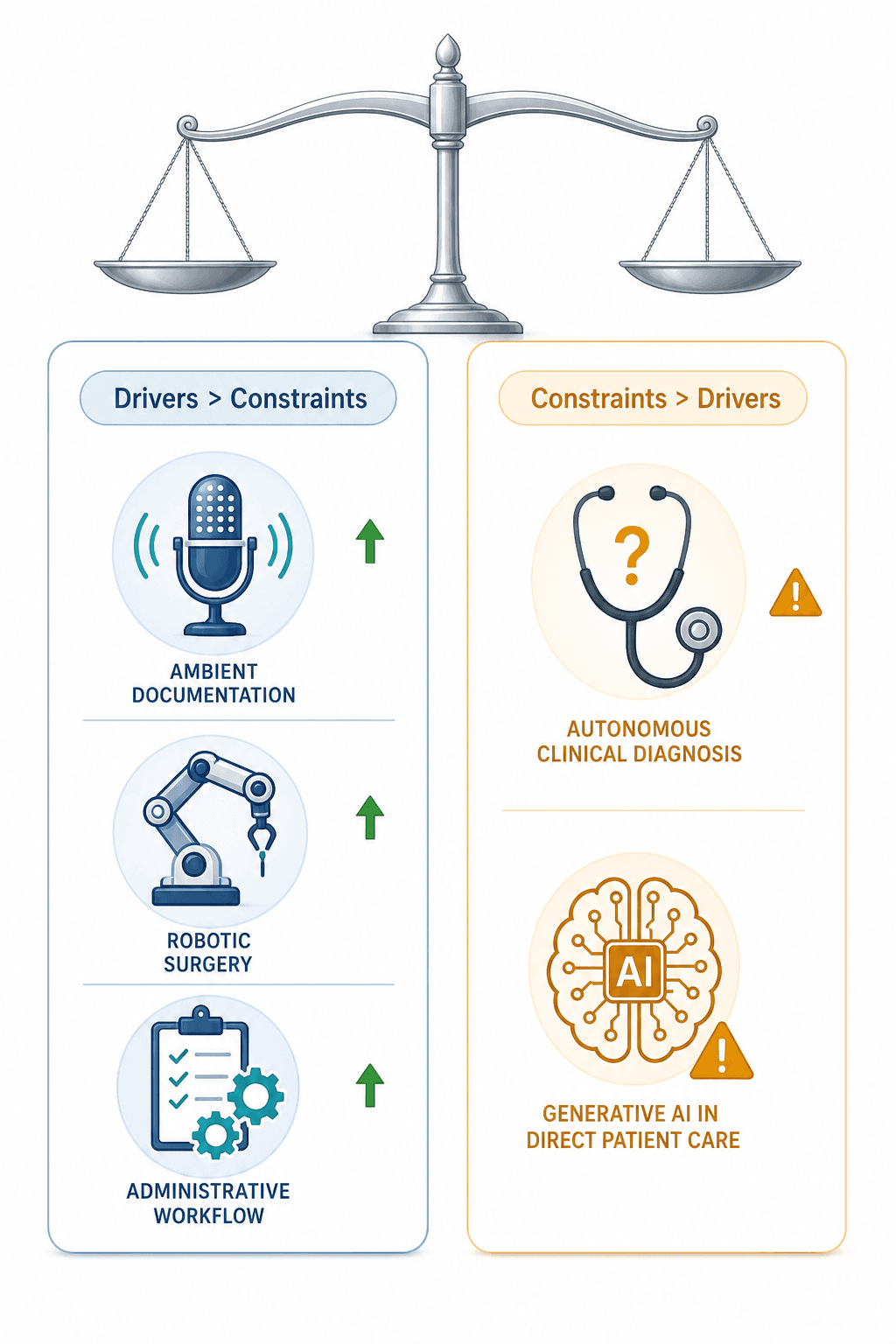

Segment-Level Tension Analysis: Where Drivers Outweigh Constraints — and Where They Don't

The most useful analysis for decision-makers is not the aggregate market size, but the segment-level assessment of where the drivers-constraints tension resolves in favor of adoption — and where it does not. The JAMIA survey provides the most direct evidence for this analysis, supplemented by market share data from Fortune Business Insights.

| Segment | Adoption Activity | High Success Rate | Key Driver | Key Constraint |

|---|---|---|---|---|

| Ambient Documentation | 100% | 53% | Clinician burnout crisis; 40–45% documentation time reduction | EHR integration; data privacy |

| Robot-Assisted Surgery | High (22.94% market share in 2026) | Not separately surveyed | Precision, minimally invasive outcomes; chronic disease demand | Cost; training requirements |

| Imaging / Radiology | 90% deployed | 19% (clinical diagnosis AI) | FDA clearance acceleration; 76% of cleared devices in radiology | Tool immaturity; model drift; workflow integration |

| Administrative Workflow | Moderate to high | Not separately surveyed | Operational efficiency; ROI clarity (3.2:1 average) | Financial concerns; change management |

| Autonomous Clinical Diagnosis | Moderate | 19% | Diagnostic accuracy potential; chronic disease burden | Tool immaturity; regulatory uncertainty; liability concerns |

| Generative AI in Direct Patient Care | Early stage (46% still experimenting in 2024) | Not separately surveyed | Generative AI capability; patient engagement potential | Hallucination risk; regulatory uncertainty; evidence gap |

The data reveals a clear pattern. Ambient documentation and robot-assisted surgery are the segments where drivers most clearly outweigh constraints. Both address well-defined, high-pain-point clinical problems with mature technology that delivers measurable outcomes. Imaging and radiology, despite being the most deployed AI use case (90% of health systems have at least partial deployment), shows a striking gap: only 19% report high success in clinical diagnosis AI. This suggests that while radiology AI is widely adopted for triage and workflow optimization, its use for autonomous diagnosis remains constrained by tool immaturity and the complexity of integrating AI into diagnostic decision-making.

At the other end of the spectrum, autonomous clinical diagnosis and generative AI in direct patient care remain segments where constraints dominate. The evidence base for these applications is thinner, regulatory frameworks are less settled, and the risks — diagnostic error, hallucination, liability — are higher. The Evidence Gap and Regulatory Landscape for Conversational AI in Healthcare article provides a deeper analysis of these constraints.

Competitive Dynamics: Startups, Incumbents, and the 10-20-70 Rule

The competitive landscape is shaped by a dynamic tension between AI-native startups and established healthcare technology incumbents. Key players include Amazon, Microsoft, NVIDIA, Google, Siemens Healthineers, and GE HealthCare, alongside hundreds of specialized startups targeting specific clinical or operational use cases.

A notable pattern is that AI-native companies have captured an estimated 85% of healthcare AI spend, according to industry analysis. This reflects the first-mover advantage of startups that built products specifically for AI-driven workflows, rather than retrofitting AI onto legacy systems. However, incumbents are responding through acquisitions — Microsoft's acquisition of Nuance Communications in March 2022 is a prominent example — and through internal AI development programs.

BCG's 10-20-70 rule provides a useful framework for understanding where value is created in AI deployment: 10% of effort goes to algorithms, 20% to technology and data infrastructure, and 70% to people and process change. This rule underscores that the competitive advantage in healthcare AI will not come from having the best algorithm alone — it will come from the ability to integrate AI into complex clinical workflows, train staff, manage change, and measure outcomes. The Startups vs. Incumbents in Medical AI article provides a deeper analysis of this competitive dynamic.

Outlook Scenarios for 2026–2030

The trajectory of the AI healthcare market over the next five years will depend on how the drivers-constraints tension resolves. Three plausible scenarios emerge from the data.

- Optimistic scenario: Structural barriers soften significantly. Regulatory clarity improves through finalized FDA guidance on predetermined change control plans and post-market surveillance. AI tool maturity advances as more products undergo rigorous external validation and real-world evidence studies. Financial ROI becomes clearer as early adopters publish detailed cost-benefit analyses. In this scenario, the market tracks toward the higher end of projections, with ambient documentation and robotic surgery leading, and autonomous diagnosis beginning to gain traction by 2028–2029.

- Baseline scenario: Gradual progress with persistent friction. Regulatory frameworks evolve but remain fragmented across jurisdictions. Tool quality improves incrementally but continues to lag expectations in complex clinical scenarios. Financial concerns persist as health systems struggle to build convincing business cases for AI investments. The market grows steadily but does not reach the most optimistic projections. Ambient documentation and administrative AI continue to lead adoption; autonomous clinical diagnosis remains niche.

- Pessimistic scenario: Regulatory setbacks or safety incidents slow adoption. A high-profile AI diagnostic failure or a regulatory enforcement action could trigger a pullback in investment and deployment. Public trust erodes, and health systems become more cautious. In this scenario, market growth slows, and the lower end of projections becomes more likely. The focus shifts back to narrow, well-validated use cases, and generative AI in direct patient care faces significant headwinds.

The Health Tech AI in 2026: Where Investment, Adoption, and ROI Data Converge article provides additional investment and ROI data that informs these scenarios.

Key Questions for Decision-Makers

For investors, health system executives, and strategists evaluating AI investments, the most useful framework is not a single market projection but a readiness lens that considers tool maturity, integration complexity, and organizational capacity. The following questions can guide that evaluation.

- Is the AI tool solving a documented workflow pain point or a speculative future need? The highest-success applications — ambient documentation, robotic surgery — address well-defined, high-pain-point problems with measurable outcomes. Tools that target speculative or poorly defined problems are more likely to encounter adoption barriers.

- What is the evidence tier supporting this product? Has it been validated in a prospective, multi-center study with diverse patient populations? Or does its evidence base consist of retrospective single-center studies or vendor white papers? The JAMIA survey's finding that 77% of health systems cite tool immaturity as the top barrier underscores the importance of rigorous evidence.

- Does my organization have the change management capacity to deploy this tool effectively? BCG's 10-20-70 rule is a reminder that 70% of the effort in AI deployment is people and process change. Organizations that underestimate this dimension will struggle to realize value, regardless of the tool's technical quality.

- How does the regulatory status of this tool affect my risk exposure? Is it FDA-cleared, and if so, through which pathway? Does the clearance cover the specific clinical use case I am considering? The U.S. Regulatory Framework in 2026 article provides a comprehensive overview of the current regulatory landscape.

- What is the total cost of ownership, including integration, training, and ongoing monitoring? The average ROI of 3.2:1 and 12-to-18-month payback period are useful benchmarks, but they mask wide variation. A detailed total-cost-of-ownership analysis should be part of any procurement decision.

Comments

Join the discussion with an anonymous comment.