Market Context: The AI Medical Imaging Market in 2026

The AI medical imaging market has crossed a critical threshold in 2026. No longer a collection of experimental point solutions, it has become a structured, category-driven industry where the most successful companies own specific clinical workflows rather than broad interpretation platforms. For hospital administrators, radiology leads, and investors, understanding this landscape requires a use-case lens, not a vendor list.

The numbers tell the story. According to the FDA's updated list of AI-enabled medical device authorizations through the end of 2025, there are now 1,451 total authorized AI devices since 1995, of which 1,104 — or 76% — are radiology devices. In Q4 2025 alone, 72 AI devices were cleared, with 55 (76%) falling under radiology. This sustained dominance of imaging within the broader AI-in-healthcare regulatory pipeline underscores the maturity of the modality-specific AI market.

Market valuations reflect this growth trajectory. The global AI in radiology market was valued at $518.1 million in 2025 and is projected to grow to $3.2 billion by 2034, representing a compound annual growth rate (CAGR) of 23.38%, according to Fortune Business Insights. North America held a 44.45% market share in 2025, driven by concentrated FDA clearance activity and early adoption by major health systems.

The key structural shift is the move from point-solution experimentation to category specialization. Early AI imaging companies often built single-condition algorithms — a pulmonary nodule detector here, a pneumothorax flag there — that sat outside clinical workflows and required radiologists to toggle between multiple standalone applications. The market has since consolidated around vendors that own an entire clinical decision pathway: stroke detection with care team notification, multi-condition emergency CT triage, or organized cancer screening. This evolution is the central dynamic shaping procurement decisions in 2026.

For a deeper dive into the clinical evidence and regulatory landscape underpinning these trends, see our companion article on AI in Medical Image Analysis: Clinical Evidence, Regulatory Landscape, and the Path to Maturity in 2026.

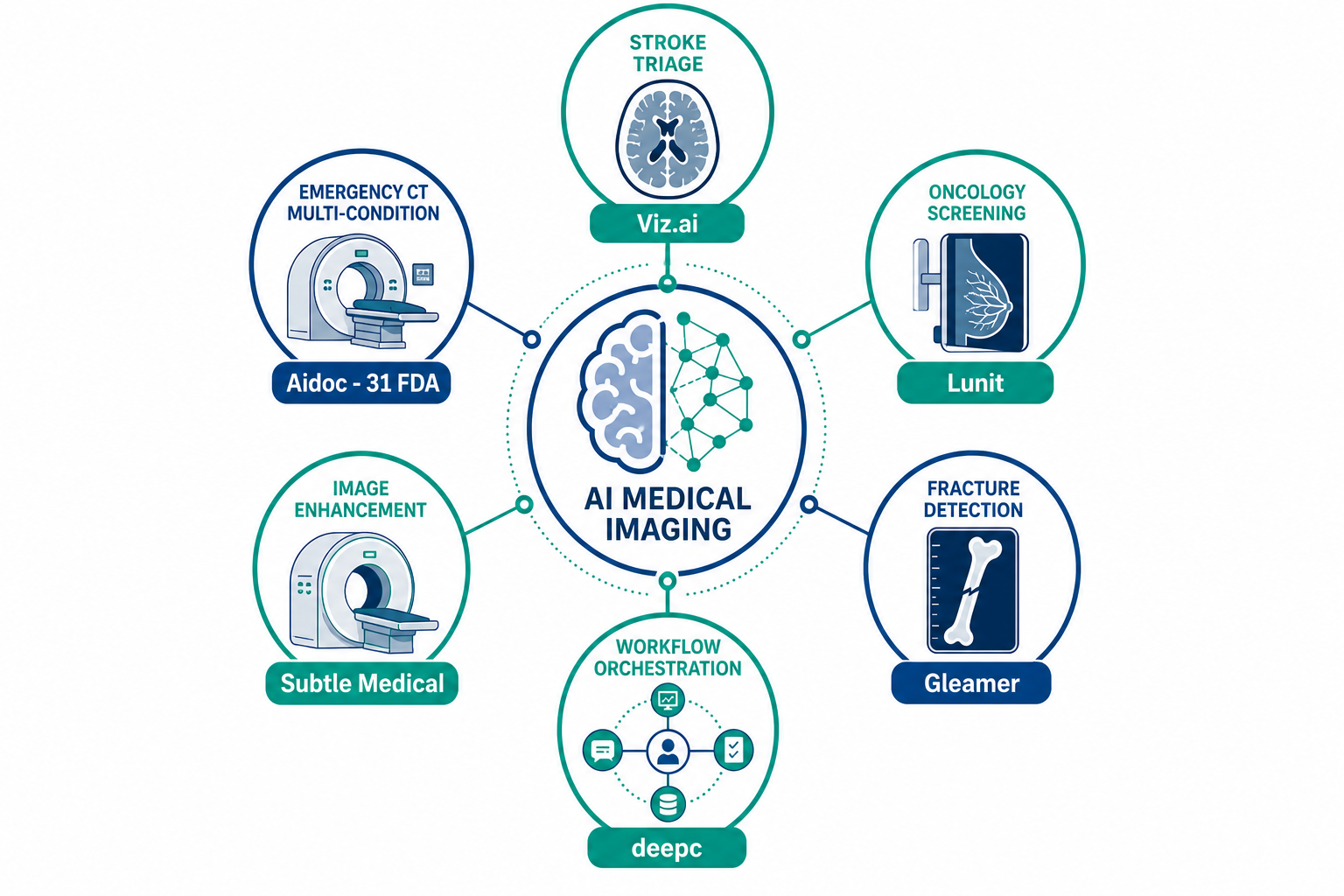

Category Leaders by Clinical Use Case

The following profiles examine the dominant vendor in each major clinical imaging use case. Each entry includes FDA clearance counts, deployment maturity, and specific market positioning. These are not rankings — they are category maps designed to help procurement teams match vendors to institutional priorities.

Stroke Triage: Viz.ai

Viz.ai has established itself as the category-defining company for AI-driven stroke care. Its platform specializes in automated detection of large vessel occlusion (LVO) on CT angiography, combined with real-time care team notification and mobile communication tools. Rather than simply flagging findings, Viz.ai orchestrates the entire acute stroke workflow — from imaging to specialist alert to treatment decision — which is why it has become the standard in comprehensive stroke centers across the U.S.

The company's FDA clearance portfolio spans multiple stroke-related indications, and its deployment footprint now covers over 1,500 hospitals. Its competitive moat lies not in algorithm performance alone — several competitors have comparable LVO detection accuracy — but in workflow integration: the platform connects directly to PACS, sends HIPAA-compliant mobile alerts, and provides a unified communication interface for the stroke team. For emergency departments that treat a high volume of stroke patients, Viz.ai remains the default choice.

Multi-Condition Emergency CT: Aidoc

Aidoc has built the broadest FDA-cleared portfolio among pure-play AI imaging companies, with 31 FDA clearances covering intracranial hemorrhage, pulmonary embolism, cervical spine fractures, free intra-abdominal air, and more. Its platform is designed for the emergency CT workflow: a single AI engine that simultaneously screens for multiple acute conditions on non-contrast head CTs, chest CTs, and CT angiograms, then prioritizes findings in the radiologist's worklist.

Aidoc's market position is built on breadth and integration. Rather than requiring separate point solutions for each condition, Aidoc offers a unified triage layer that reduces alert fatigue and simplifies procurement. The company has also invested heavily in PACS and EHR integration, with validated deployments at major health systems including HCA Healthcare and the U.S. Department of Veterans Affairs. For emergency departments and trauma centers that need comprehensive acute-condition coverage, Aidoc is the most frequently selected vendor.

Oncology Screening: Lunit

Lunit has emerged as the leading AI company focused on organized cancer screening, particularly in breast cancer and lung cancer. Its Lunit INSIGHT suite provides AI-powered analysis of mammography, digital breast tomosynthesis, and chest X-rays, with strong validation in large-scale screening programs. The company has secured regulatory clearances in the U.S., Europe, and Asia, and its technology is deployed in screening centers across South Korea, the U.S., and the Middle East.

Lunit's differentiation lies in its focus on screening specificity and recall reduction. In mammography screening, the platform has demonstrated the ability to reduce false positives while maintaining sensitivity, a critical metric for screening programs where unnecessary recalls create patient anxiety and system costs. For outpatient screening centers and population health programs, Lunit represents the most evidence-backed option in the oncology screening category.

Fracture Detection: Gleamer

Gleamer has carved out a clear leadership position in AI-powered fracture detection on X-ray, a high-volume, high-stakes use case in emergency departments and urgent care settings. Its BoneView platform detects fractures across the full skeletal anatomy — upper and lower extremities, pelvis, spine, and ribs — and integrates directly into the radiologist's PACS worklist.

The company's market position is built on specialization. While broader multi-condition platforms like Aidoc cover some fracture indications, Gleamer's dedicated focus on X-ray fracture detection allows it to achieve higher per-condition accuracy and a more comprehensive anatomical coverage. It has received CE marking and FDA clearance, and its deployments span emergency departments in Europe and the U.S. For trauma centers and orthopedic clinics that process high volumes of X-ray studies, Gleamer is the category leader.

Image Enhancement and Scan Acceleration: Subtle Medical

Subtle Medical occupies a distinct niche within the AI imaging landscape: rather than detecting pathology, its AI improves image quality and accelerates scan times. The company's SubtleMR and SubtlePET platforms use deep learning to reconstruct high-quality images from lower-dose or faster acquisitions, enabling MRI and PET scan time reductions of 50–70% without hardware changes.

This category addresses a fundamentally different problem than diagnostic AI. For imaging centers and hospitals facing MRI scheduling backlogs, Subtle Medical's technology directly increases throughput and patient access. The company has secured FDA clearance and partnerships with major OEMs including GE HealthCare and Siemens Healthineers, which embed Subtle's technology into their own reconstruction pipelines. For institutions where scanner capacity is the primary bottleneck, Subtle Medical offers a non-diagnostic AI solution with clear operational ROI.

Workflow Orchestration: deepc

deepc has pioneered a different model: rather than building its own diagnostic algorithms, it operates as an AI orchestration layer — a marketplace and integration platform that connects multiple third-party AI applications to existing PACS and RIS systems. This approach solves the fragmentation problem that has plagued radiology AI adoption: instead of managing separate integrations for each point solution, health systems can use deepc's platform to access a curated library of FDA-cleared algorithms through a single interface.

deepc's value proposition is particularly strong for multi-specialty hospitals and large health systems that want to deploy multiple AI tools without the integration overhead. The company has partnered with Konica Minolta Healthcare (announced January 2026) to expand its cloud-based deployment capabilities. For institutions that have already identified several AI tools they want to deploy but lack the IT resources to integrate each one individually, deepc's orchestration model is the most practical path forward.

| Clinical Use Case | Category Leader | FDA Clearances | Primary Modality | Best For |

|---|---|---|---|---|

| Stroke Triage | Viz.ai | Multiple stroke-specific | CT Angiography | Comprehensive stroke centers, EDs with high stroke volume |

| Multi-Condition Emergency CT | Aidoc | 31 | CT (head, chest, spine) | Emergency departments, trauma centers |

| Oncology Screening | Lunit | Multiple (US, EU, Asia) | Mammography, Chest X-ray | Organized screening programs, outpatient screening centers |

| Fracture Detection | Gleamer | FDA-cleared, CE-marked | X-ray (full skeletal) | Trauma centers, orthopedic clinics, urgent care |

| Image Enhancement / Scan Acceleration | Subtle Medical | FDA-cleared | MRI, PET | Imaging centers with scanner capacity constraints |

| Workflow Orchestration | deepc | N/A (platform, not algorithm) | Multi-modality | Multi-specialty hospitals deploying multiple AI tools |

OEM Incumbents: The Platform Players

No landscape of AI medical imaging companies is complete without the OEM incumbents — GE HealthCare, Siemens Healthineers, Philips, Canon Medical, and United Imaging — whose radiology AI clearance portfolios now rival or exceed those of pure-play AI companies. However, the nature of their AI portfolios differs fundamentally from the category leaders profiled above.

According to The Imaging Wire's analysis of the FDA list (March 2026), GE HealthCare leads all companies with 120 radiology AI authorizations, followed by Siemens Healthineers at 89, Philips at 50, Canon at 45, and United Imaging at 38. These numbers include both internally developed algorithms and algorithms acquired through company acquisitions — GE's count, for example, includes Bay Labs, BK Medical, Caption Health, MIM Software, icometrix, and Spectronic Medical.

The strategic difference between OEMs and pure-play AI companies is critical for procurement. OEMs embed AI directly into their imaging hardware and reconstruction pipelines, offering seamless integration and single-vendor accountability. When a GE scanner ships with GE AI, there is no separate integration, no additional vendor management, and no data leaving the scanner's native environment. For health systems that prefer a single-vendor strategy and are already standardized on one OEM's imaging fleet, this is a compelling advantage.

However, OEM AI portfolios are inherently tied to the OEM's hardware base. A Siemens AI algorithm for cardiac CT will not run on a Canon scanner. This creates a lock-in dynamic that pure-play AI companies — particularly those using orchestration platforms like deepc — explicitly aim to break. For multi-vendor imaging departments, the best-of-breed approach offered by category-specific AI companies may deliver better per-condition performance than relying on a single OEM's portfolio.

For a broader view of the healthcare AI company landscape beyond imaging, see our article on AI in Healthcare Companies: A Structured Landscape of Active Developers.

| OEM | Radiology AI Authorizations | Key Acquisitions Included | Strategic Advantage |

|---|---|---|---|

| GE HealthCare | 120 | Bay Labs, BK Medical, Caption Health, MIM Software, icometrix, Spectronic Medical | Largest portfolio; deep hardware integration |

| Siemens Healthineers | 89 | Varian | Strong in oncology and interventional imaging AI |

| Philips | 50 | DiA Analysis, TomTec | Ultrasound and cardiac AI leadership |

| Canon Medical | 45 | Vital Images, Olea Medical | CT and MRI reconstruction AI |

| United Imaging | 38 | Organic development | Fast-growing portfolio; strong in China and emerging markets |

A Vendor Selection Framework by Institutional Profile

The most important insight for procurement teams is that there is no single "best" AI imaging company. The right vendor depends on the institution's clinical priorities, patient volume patterns, and existing IT infrastructure. The following framework maps institutional profiles to recommended AI vendor categories.

| Institutional Profile | Primary Clinical Need | Recommended AI Category | Key Evaluation Criteria |

|---|---|---|---|

| Comprehensive Stroke Center / High-Volume ED | Rapid stroke triage, acute condition detection | Stroke triage (Viz.ai) + Multi-condition CT (Aidoc) | Workflow integration, PACS connectivity, alert latency |

| Outpatient Screening Center | Cancer screening accuracy, recall reduction | Oncology screening (Lunit) | Sensitivity/specificity in screening populations, regulatory status in target geography |

| Trauma Center / Orthopedic Clinic | Fracture detection on X-ray | Fracture detection (Gleamer) | Anatomical coverage, false positive rate, ED workflow fit |

| Imaging Center with Scanner Capacity Constraints | MRI/PET throughput, scan time reduction | Image enhancement (Subtle Medical) | Scan time reduction %, image quality preservation, OEM compatibility |

| Multi-Specialty Hospital with Multi-Vendor Fleet | Deploying multiple AI tools without integration overhead | Workflow orchestration (deepc) | Number of available algorithms, PACS/RIS compatibility, vendor neutrality |

| Single-OEM Standardized Health System | Seamless AI integration with existing hardware | OEM AI portfolio (GE, Siemens, Philips, Canon, United Imaging) | Portfolio breadth, upgrade path, service and support terms |

When evaluating any vendor, procurement teams should prioritize three factors beyond algorithm performance: workflow integration (does the AI sit inside or outside the radiologist's existing reading environment?), regulatory status (is the algorithm FDA-cleared for the specific intended use and patient population?), and evidence tier (has the vendor published peer-reviewed validation studies with external datasets, or only white papers and retrospective single-center data?). For a detailed guide on evaluating clinical validation, see our article on Healthcare AI Companies with the Strongest Clinical Validation Evidence.

Emerging Trends: Wave 2, Foundation Models, and Beyond

The AI medical imaging market is entering its second wave, and the changes are structural, not incremental. According to an analysis by Out-Of-Pocket (December 2025), Wave 1 companies — typified by firms like Nines — built FDA-cleared models but struggled with brittle algorithms, clunky workflows, and unclear reimbursement pathways. Many of these companies have been acquired, pivoted, or shut down.

Wave 2 companies are defined by a fundamentally different approach: workflow-first design. Rather than building a diagnostic algorithm and then figuring out how to insert it into the radiologist's day, Wave 2 companies start by understanding the workflow — the PACS environment, the reporting process, the communication pathways — and build AI that fits naturally within it. This includes leveraging large language models (LLMs) for automated impression drafting and consistency checks, building better PACS interfaces, and embedding AI within end-to-end radiology services rather than offering standalone analysis.

Several regulatory and reimbursement developments are accelerating this shift:

- The FDA has formalized Predetermined Change Control Plans (PCCPs), allowing companies to make iterative model updates without submitting new 510(k) applications for each change. This removes a major regulatory bottleneck that previously discouraged continuous improvement.

- CMS updated its payment policies for AI coronary plaque analysis in October 2025, signaling the beginning of dedicated reimbursement pathways for AI-interpreted imaging findings. This could unlock broader adoption in cardiovascular imaging.

- New approaches are emerging that expand the scope of existing imaging studies — for example, using AI to surface bone density signals from routine chest CTs that were acquired for other indications, effectively creating new clinical value from existing scans.

The expansion of AI beyond diagnostic imaging into adjacent areas like revenue cycle management (RCM) and clinical documentation is also reshaping the competitive landscape. Companies that started in imaging are increasingly offering broader platforms, while companies from adjacent categories are moving into imaging. For a cross-sector analysis of AI healthcare companies, see our article on Top AI Healthcare Companies in 2026 — A Category-Based Analysis.

For a detailed analysis of how the FDA is reshaping AI medical device regulation through PCCPs, total product lifecycle (TPLC) oversight, and transparency requirements, see our article on From Evidence Gaps to Lifecycle Oversight: How the FDA is Reshaping AI Medical Device Regulation.

For a comprehensive set of statistics on AI adoption, market size, clinical accuracy, and ROI across healthcare, see our data article on AI in Healthcare by the Numbers: 100+ Statistics on Adoption, Market Size, Clinical Accuracy, ROI, and Risk (2026).

Comments

Join the discussion with an anonymous comment.