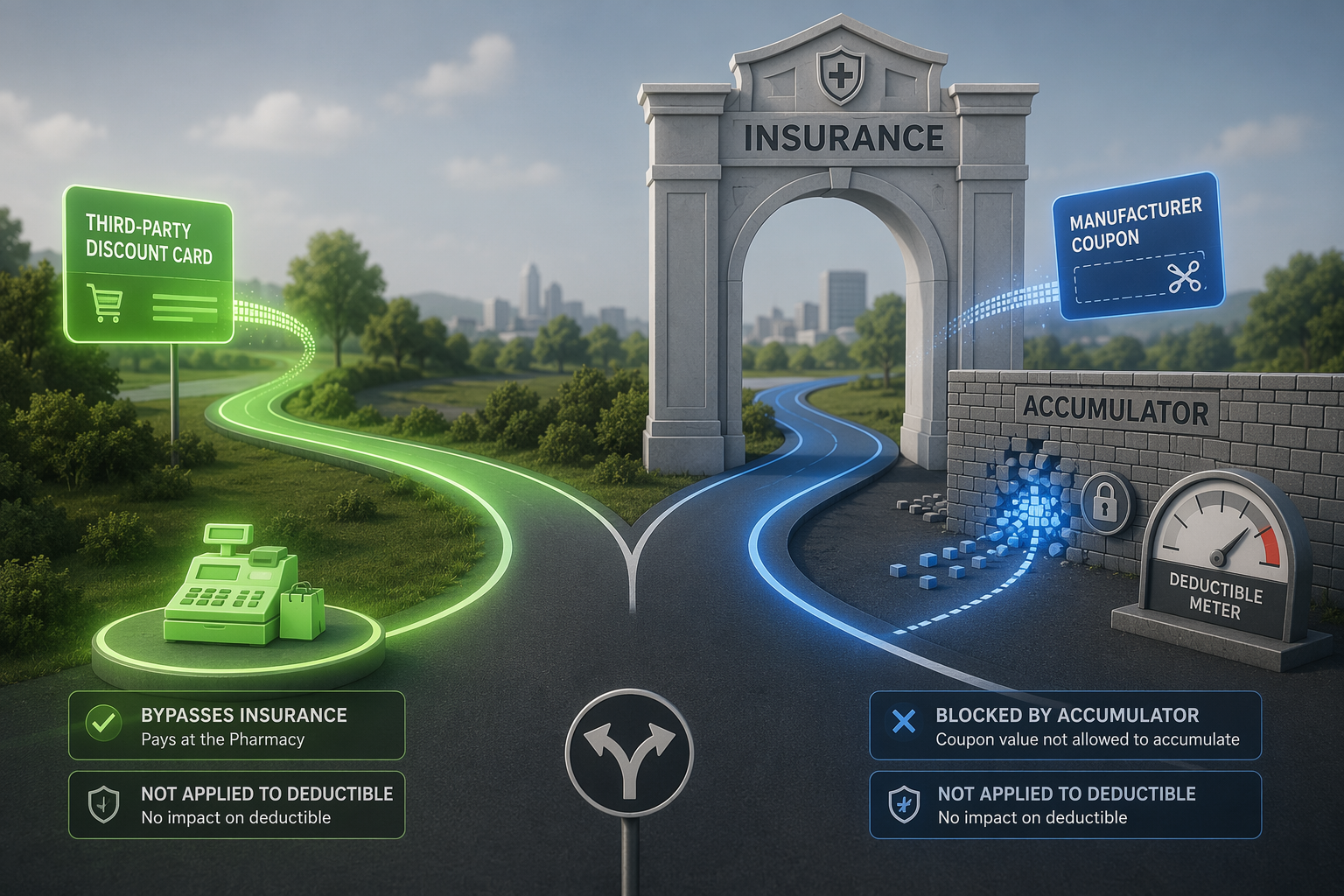

The answer changes the moment you separate the two things people often bundle under “prescription discount program.” Third-party discount cards such as GoodRx, SingleCare, or Optum Perks are used instead of insurance, so the claim never moves through the deductible. Manufacturer copay coupons are different: they are built to work alongside insurance, which is why plan design can interfere with whether that coupon value counts toward deductible progress at all [1].

When the card replaces insurance

A third-party discount card is the simpler case. The pharmacy applies a negotiated cash-style price, the insurer is bypassed, and there is nothing to credit to the deductible. That is true whether the card saves the patient a little or a lot at the counter: the transaction did not become an insurance claim, so the deductible does not budge [1].

When the coupon enters the insured claim

Manufacturer copay coupons create the more complicated problem because the claim still runs through the pharmacy benefit. The patient sees a lower copay, but the plan can still decide how much of that coupon value counts toward the deductible or out-of-pocket maximum. Copay accumulator programs block that value from accumulating. Copay maximizer programs go a step further by spreading coupon assistance across the year so the patient keeps seeing a plan-priced copay after the coupon subsidy has been allocated, even though deductible credit may never materialize in the way the patient expects [1].

That distinction is why the same phrase, “I used a discount program,” can describe two very different ledger effects. One path takes the insurer out of the transaction entirely. The other path keeps the insurer in the middle, then strips out some or all of the coupon value before it can help the patient reach the deductible.

The scale is no longer niche. Drug Channels estimated in 2026 that accumulators were available to 84% of commercially insured beneficiaries, maximizers to 81%, and about 39% of covered lives were in plans with full implementation, affecting 112.9 million people [2].

The trend also has not stayed confined to one drug class. IQVIA reported that among oncology brand users, accumulator exposure rose from 6% in 2019 to 24% in 2024, while maximizer exposure rose from 4%-6% to 13%-24% over the same period [3].

Once the mechanism is clear, the downstream effects are easier to interpret. A peer-reviewed AJMC study found that copay accumulator adjustment program implementation was associated with significant reductions in adherence to autoimmune specialty drugs and a higher risk of discontinuation, while a 2023 JMCP study found that non-White patients were more likely to face accumulator programs even when coupon use rates were similar [4][5].

Why the policy answer stays fragmented

State bans matter, but only inside the slice of the market states can regulate. Avalere estimated that the 26 states plus the District of Columbia with accumulator bans covered about 17% of commercial lives as of January 2026 [6]. That is a meaningful restriction, but it does not settle the issue for self-funded ERISA plans, which are beyond state insurance law and cover about 63% of workers with employer coverage, compared with about 37% in fully insured plans.

Federal policy remains unsettled. After the 2023 court vacatur of the HHS accumulator rule, neither the 2025 NBPP nor the proposed 2027 NBPP had delivered a definitive replacement as of Q3 2026, so the national baseline is still provisional rather than final [1].

The operational response is also moving upstream. Infinitus describes AI phone agents that detect accumulator and maximizer status during benefits-verification calls, which suggests that more plans and vendors now treat this as a verification problem before the prescription reaches adjudication [7].

So the practical answer is narrow and plan-specific: third-party discount cards never count toward deductibles because they bypass insurance, while manufacturer copay coupons can fail to count because accumulator and maximizer designs often intercept that value before it reaches deductible credit. The result is a market split by plan type and jurisdiction, not a single rule that applies to every prescription discount program.

References

- Copay Adjustment Programs: What Are They and What Do They Mean for Consumers? KFF

- Copay Accumulators and Maximizers in 2026Drug Channels

- Still on the Rise: Deductible Accumulators & Copay Maximizers in 2024IQVIA, April 2025

- Copay Accumulator Adjustment Programs and Adherence to Specialty Medications for Autoimmune DiseaseAmerican Journal of Managed Care

- Racial and Ethnic Disparities in Exposure to Copay Accumulator Adjustment ProgramsJournal of Managed Care & Specialty Pharmacy, 2023

- State Copay Accumulator Bans Now Affect at Least 17% of Commercial LivesAvalere, January 2026

- Copay Accumulators & Copay Maximizers: AIInfinitus AI

Comments

Join the discussion with an anonymous comment.