The AI Healthcare Stack: An Architectural View of the 2026 Landscape

The most common way to survey the healthcare AI market is a ranked list or a flat grouping by category. Both approaches have their uses, but they obscure something essential: the companies in this market do not operate independently. A clinical decision support tool is only as good as the data infrastructure beneath it. An ambient scribe that cannot integrate with the revenue cycle leaves money on the table. A diagnostic algorithm that cannot communicate with the EHR creates workflow friction, not relief.

This article takes a different approach. It maps the top AI healthcare companies as a layered stack — from foundational data and interoperability up through drug discovery — and identifies category leaders not by valuation alone, but by real-world deployment scale, regulatory clearance counts, and capital efficiency. The goal is to give healthcare executives, health IT leaders, and procurement teams an architectural understanding of the market, not just a directory of names.

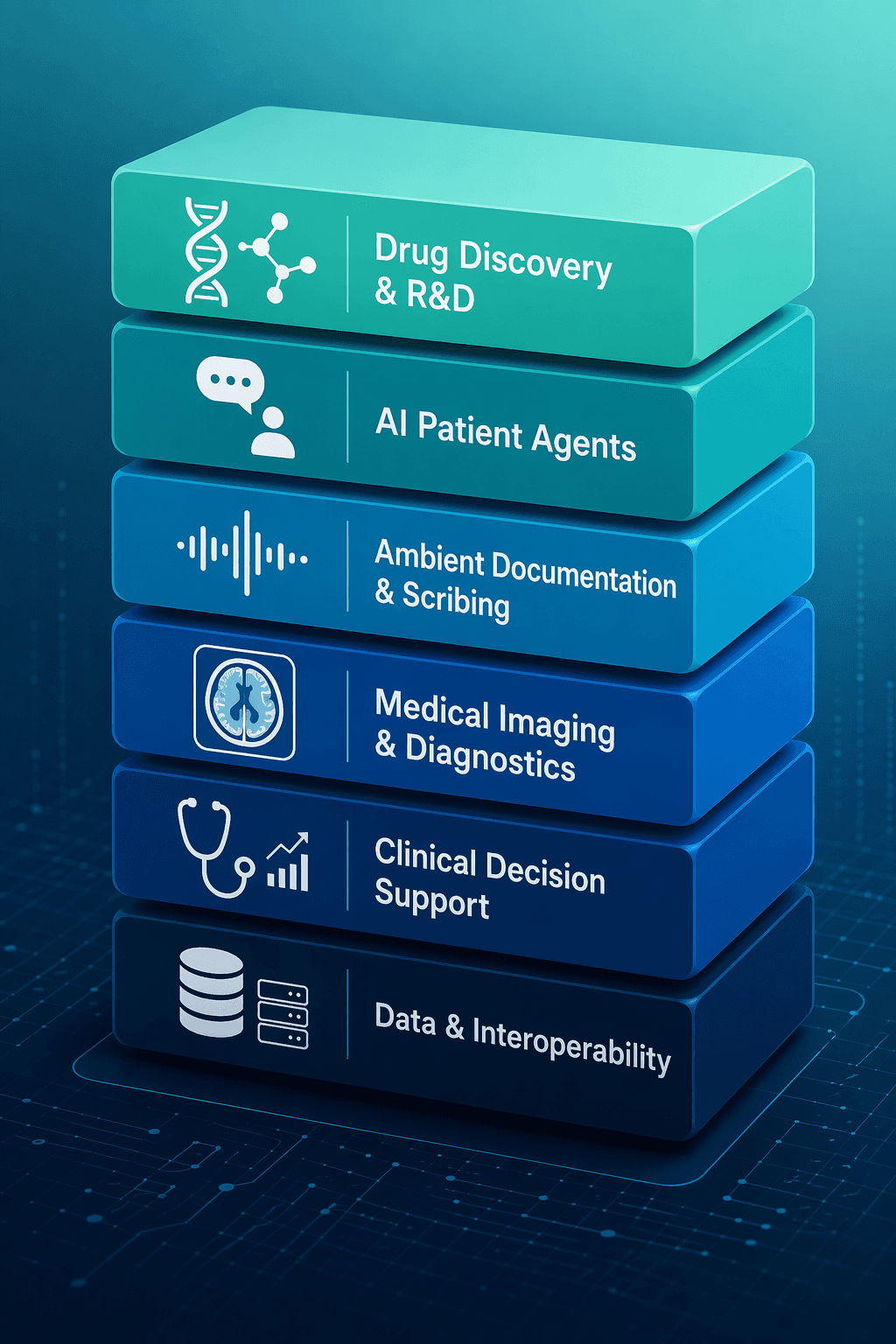

This stack framework builds on and differentiates from the site's existing category-based analysis by adding a data infrastructure layer, cross-cutting themes, and a structured buyer selection framework. The seven layers covered are:

- Data Infrastructure & Interoperability

- Clinical Decision Support

- Ambient Documentation & AI Scribing

- Medical Imaging & Diagnostics

- Patient-Facing AI Agents

- Revenue Cycle Automation

- Drug Discovery & R&D

Market Context: The $36.8 Billion Healthcare AI Opportunity in 2026

Before examining individual companies, it is worth establishing the market's scale and trajectory. According to data from AI Funding Tracker, the healthcare AI market reached $21.66 billion in 2025 and is projected to grow to $36.79 billion in 2026, representing a compound annual growth rate of 38.6%. By 2030, the market is expected to approach $110.61 billion.

Several indicators confirm that this growth is not just a projection but is already materializing:

| Metric | Value | Source |

|---|---|---|

| Healthcare AI market (2025) | $21.66B | AI Funding Tracker |

| Healthcare AI market (2026 projected) | $36.79B | AI Funding Tracker |

| CAGR (2025–2030) | 38.6% | AI Funding Tracker |

| VC funding into AI health tech (2025) | ~$14B (63% higher than 2024) | AI Funding Tracker |

| AI share of digital health funding (H1 2025) | 62% (up from 37% in 2024) | AI Funding Tracker |

| Healthcare organizations actively using AI | 63% | AI Funding Tracker |

| Physicians who used health AI (2024) | 66% (up 78% from 2023) | AI Funding Tracker |

| AI/ML medical device clearances (2025) | 295 devices from 221 manufacturers | Innolitics |

| Radiology share of FDA AI clearances | 71.5% | Innolitics |

The regulatory pipeline is equally telling. Innolitics reports that 295 AI/ML-enabled medical devices were cleared by the FDA in 2025 alone, from 221 unique manufacturers. The median clearance time was 142 days, and 10% of devices (30 total) were authorized with Predetermined Change Control Plans (PCCPs), enabling iterative updates without new submissions. This regulatory velocity signals that the FDA has moved beyond the early-adopter phase and into a steady-state review cadence for AI devices.

Layer 1: Data Infrastructure & Interoperability — The Foundation

Every downstream AI application — clinical decision support, ambient scribing, imaging diagnostics — depends on clean, accessible, and interoperable data. This layer is the least visible to clinicians but the most structurally important. Without it, AI tools operate in data silos, produce inconsistent outputs, and fail to scale across health systems.

The category leader in this layer is Innovaccer. The company raised a $275 million Series F in 2025 and operates in the $6.2 billion healthcare data analytics market. Its platform integrates with more than 140 healthcare data sources, spanning EHRs, claims systems, labs, and social determinants of health data. Innovaccer's value proposition is straightforward: unify the data first, then layer analytics and AI on top. This positions it as an infrastructure play rather than a point solution.

A contrasting approach comes from AWS Health AI, which provides the cloud infrastructure and AI services that health systems and developers use to build their own data pipelines. AWS does not compete directly with Innovaccer; rather, it offers the raw compute and storage layer, while Innovaccer provides the healthcare-specific data normalization and interoperability layer. For a detailed profile of Amazon's healthcare AI stack, see the site's AWS Health AI portfolio profile.

Layer 2: Clinical Decision Support — The Physician's Co-Pilot

Clinical decision support (CDS) is the layer where AI directly influences patient care decisions at the point of care. The dominant player in this category is OpenEvidence, which has achieved a $12 billion valuation as of January 2026 after its most recent funding round. The company's metrics are striking: 760,000 registered U.S. physicians, 18 million clinical consultations per month, and deployment across more than 10,000 hospitals. According to AI Funding Tracker, more than 40% of all U.S. physicians use OpenEvidence daily.

What sets OpenEvidence apart is its capital efficiency. With approximately $700 million raised, its valuation-to-capital ratio stands at 16.3x — the highest among the top 10 AI healthcare companies by valuation. This suggests that the company has achieved product-market fit without requiring the massive capital infusions typical of the sector.

In March 2026, OpenEvidence launched Coding Intelligence, a move that signals its ambition to expand beyond clinical decision support into the revenue cycle. This is a pattern we will see repeated across multiple layers: companies that establish dominance in one category are using their physician user base and data infrastructure to expand into adjacent categories.

A complementary player in this layer is Google Health AI. While Google's portfolio spans multiple layers — from imaging AI to genomics — its clinical decision support capabilities, powered by Med-PaLM and other foundation models, make it a significant presence. For a comprehensive overview, see the site's Google Health AI portfolio profile.

| Company | Valuation | Key Metric | Capital Efficiency |

|---|---|---|---|

| OpenEvidence | $12B | 760K physicians, 18M consultations/month | 16.3x |

| Google Health AI | N/A (Alphabet subsidiary) | Multi-layer portfolio | N/A |

Layer 3: Ambient Documentation & AI Scribing — The Workflow Revolution

Ambient documentation has emerged as the most rapidly adopted AI category in clinical settings. The clinical documentation category generated $600 million in revenue in 2025, a 2.4x year-over-year increase, according to AI Funding Tracker. This growth is driven by a simple value proposition: physicians spend an average of two hours on documentation for every hour of direct patient care. Ambient AI scribes listen to the clinical conversation and generate structured notes automatically, directly in the EHR.

The category leader is Abridge, valued at $5.3 billion after a $300 million Series E in June 2025. Abridge has surpassed $100 million in annual recurring revenue and is deployed across more than 150 enterprise health systems. It has been named #1 Best in KLAS for Ambient AI in Revenue Cycle Management for two consecutive years. The company is on pace to support more than 50 million medical conversations in 2026.

Abridge's competitive moat lies in its deep Epic integration. In health systems where Epic is the dominant EHR — which represents the majority of large U.S. hospitals — Abridge's ability to write notes directly into the clinical workflow without requiring physicians to switch applications has driven adoption rates that competitors have struggled to match.

Key competitors in this layer include:

- Nabla: A strong alternative with a focus on multi-language support and European market penetration.

- Ambience Healthcare: Valued at $1.04 billion after a $243 million Series C. Recognized as a 2026 KLAS/CHIME Trailblazer Award winner.

- Rad AI: Part of the $7.7 billion clinical documentation cluster, with a focus on radiology-specific workflow automation.

Layer 4: Medical Imaging & Diagnostics — The Most Regulated Layer

Medical imaging is the most mature and most regulated layer of the AI healthcare stack. It accounts for 71.5% of all FDA AI/ML device clearances, according to Innolitics' 2025 review. Cardiovascular imaging (8.8%) and neurology (4.7%) are distant but growing categories. The top product code for AI clearances is QIH (Radiological Computer-Aided Detection and Diagnosis), with 75 clearances in 2025 alone.

The incumbent leader in this layer is GE HealthCare. As of July 2025, GE HealthCare topped the FDA's list of AI-enabled medical device authorizations for the fourth consecutive year, with 100 listed authorizations. The company has publicly stated a goal of attaining more than 200 authorizations by 2028. Its AIR Recon DL deep learning algorithm, which reduces MRI scan times by up to 50%, has been used on more than 50 million patients since its launch in 2020.

GE HealthCare's strategy differs from AI-native imaging companies in a critical way: it embeds AI directly into its hardware. When a hospital buys a GE MRI or CT scanner, the AI comes pre-integrated. This eliminates the workflow friction of a separate AI workstation and gives GE a distribution advantage that pure-software companies cannot easily replicate.

Key AI-native competitors in this layer include:

- Aidoc: Used in more than 1,000 hospitals globally, with a focus on radiology workflow triage and prioritization.

- PathAI: Specializes in AI-powered pathology, with applications in cancer diagnosis and clinical trial matching.

- Qure.ai: Deployed in more than 90 countries, with a focus on chest X-ray and CT interpretation for tuberculosis, lung cancer, and stroke.

A company that bridges the imaging and data infrastructure layers is Tempus AI. With a $14 billion valuation, $1.27 billion in total revenue in 2025 (83% year-over-year growth), and a network of more than 45 million de-identified patient records, Tempus operates at the intersection of genomic data, clinical data, and AI-powered diagnostics. Its network extends across approximately 4,000 to 4,500 hospitals, and it works with 95% of top oncology pharmaceutical companies. Tempus is not purely an imaging company — it is a data and diagnostics platform that happens to have strong imaging capabilities.

Layer 5: Patient-Facing AI Agents — The New Front Door

Patient-facing AI agents represent a shift from administrative chatbots to clinically-grounded engagement platforms. These agents handle pre-visit intake, post-discharge follow-up, medication adherence monitoring, and chronic disease management — tasks that have traditionally required human call center staff or manual outreach.

The category leader is Hippocratic AI, valued at $3.5 billion. The company has deployed its AI agents across more than 50 large health systems in six countries — all within 15 months of its commercial launch. This deployment velocity is the defining metric for this layer. Unlike imaging AI, which requires FDA clearance and months of workflow integration, patient-facing AI agents can be deployed in weeks, making adoption speed a competitive differentiator.

Hippocratic AI's agents are designed to operate within strict clinical guardrails. The company has emphasized safety protocols, including escalation pathways to human clinicians when the AI encounters situations beyond its scope. This is critical for a layer that interacts directly with patients: a misdiagnosis from an imaging AI is caught by the radiologist, but a misleading response from a patient-facing agent may not be caught at all.

Layer 6: Revenue Cycle Automation — The $250 Billion Battleground

Revenue cycle management (RCM) represents the largest addressable market in the AI healthcare stack. The annual RCM market exceeds $250 billion, according to industry estimates cited by AI Funding Tracker. Healthcare administrative costs exceed $450 billion annually, and a significant portion of that is tied to billing, coding, prior authorization, and claims management — all areas where AI can drive measurable ROI.

The category leader in autonomous coding is CodaMetrix, which raised $110.65 million across four rounds and was ranked #1 in the 2026 Best in KLAS segment for Autonomous Coding (February 2026). CodaMetrix focuses specifically on medical coding automation — converting clinical documentation into accurate billing codes without human intervention.

A broader RCM automation platform is AKASA, valued at $205 million in 2026. AKASA covers the full revenue cycle, from eligibility verification and prior authorization through claims submission and denial management.

What makes this layer particularly dynamic is the convergence happening from adjacent layers. Abridge, the ambient scribing leader, is expanding into coding and billing. OpenEvidence launched Coding Intelligence in March 2026. Nabla is building RCM capabilities. The thesis is straightforward: if an AI system already has access to the clinical conversation (ambient scribing) or the clinical decision process (CDS), it is well-positioned to generate the billing codes and documentation required for reimbursement.

| Company | Primary Focus | Key Metric | Expansion Direction |

|---|---|---|---|

| CodaMetrix | Autonomous medical coding | #1 Best in KLAS (2026) | Coding depth |

| AKASA | Full RCM automation | $205M valuation | End-to-end RCM |

| Abridge | Ambient scribing → coding | $5.3B valuation, 150+ health systems | RCM expansion |

| OpenEvidence | CDS → coding | $12B valuation, Coding Intelligence launched Mar 2026 | RCM expansion |

Layer 7: Drug Discovery & R&D — The Longest Horizon

Drug discovery is the layer with the longest time-to-value but the highest potential ROI. Unlike the other layers in this stack, where deployment happens in months, AI-driven drug discovery operates on timelines measured in years. The evaluation criteria are also different: instead of deployment counts or FDA clearances, the relevant metrics are pipeline progress, partnership quality, and platform validation.

The most notable company in this layer is Xaira Therapeutics, which raised a $1 billion-plus Series A — one of the largest initial financings in biotech history. Xaira applies generative AI and protein engineering to drug design, with a focus on previously undruggable targets. The company's valuation is not publicly disclosed, but the size of its Series A signals strong investor conviction in its platform.

Another significant player is Formation Bio, which has raised $372 million. Formation Bio focuses on using AI to accelerate clinical trial operations — patient recruitment, site selection, and data management — rather than on drug design itself. This positions it as an operational AI layer within the drug development pipeline, distinct from the discovery-focused approach of Xaira.

Cross-Cutting Themes: Consolidation, the RCM Battleground, and the European Opportunity

Three themes cut across all seven layers and are likely to define the market's evolution over the next 12 to 24 months.

1. Consolidation and the Incumbent Response

AI-native companies have captured an outsized share of healthcare AI spending. According to industry analysis, AI-native companies account for approximately 85% of AI spend in healthcare, while traditional health IT incumbents have been slower to respond. However, that dynamic is shifting. GE HealthCare's aggressive AI authorization strategy, Epic's growing AI marketplace, and Oracle Health's AI investments all signal that incumbents are mobilizing. For a detailed analysis of this tension, see the site's article on Startups vs. Incumbents in Medical AI.

2. The RCM Battleground

Revenue cycle management has become the convergence point for multiple AI categories. Ambient scribing companies (Abridge, Nabla) are moving into coding. Clinical decision support companies (OpenEvidence) are launching coding modules. Imaging AI companies are exploring how their findings can automatically populate billing codes. The $250 billion RCM market is large enough to support multiple winners, but the competition will intensify as vendors from adjacent layers collide.

3. The European Opportunity

The European healthcare AI market remains underpenetrated relative to the United States. The EU AI Act introduces a new regulatory framework that will shape how AI companies approach the European market. Companies that can navigate the Act's risk-based classification system — particularly for high-risk medical AI applications — will have a first-mover advantage. Hippocratic AI's deployment across six countries in 15 months demonstrates that the European market is ready for adoption, but the regulatory path is still being defined.

A Buyer's Selection Framework: How to Choose a Platform at Each Stack Layer

The following framework provides actionable procurement criteria for each layer of the stack. These criteria are designed to help health system executives and procurement teams evaluate vendors on the dimensions that matter most for their specific deployment context.

| Stack Layer | Primary Procurement Criteria | Key Questions to Ask |

|---|---|---|

| Data Infrastructure & Interoperability | Integration breadth, FHIR compliance, data governance | How many data sources does the platform integrate with? What is the timeline for adding a new data source? How is patient data de-identified and governed? |

| Clinical Decision Support | Physician adoption rate, evidence base, EHR integration depth | What percentage of physicians at similar health systems use the tool daily? What peer-reviewed evidence supports the clinical recommendations? Does it write back to the EHR? |

| Ambient Documentation & Scribing | KLAS ranking, Epic integration, RCM expansion roadmap | Is the tool natively integrated with your EHR? What is the ambient note accuracy rate? Does the vendor have a roadmap for coding and billing automation? |

| Medical Imaging & Diagnostics | FDA clearance count, clinical specialty coverage, real-world evidence | How many FDA clearances does the vendor have in your specialty? What is the false positive rate in real-world deployment? Does the AI integrate with your PACS or require a separate workstation? |

| Patient-Facing AI Agents | Deployment velocity, clinical validation, patient safety protocols | What is the average deployment timeline? What escalation pathways exist for situations the AI cannot handle? Has the vendor published safety or outcomes data? |

| Revenue Cycle Automation | Compliance track record, ROI timeline, coding accuracy rates | What compliance framework does the vendor use for coding accuracy? What is the average ROI timeline for health systems of your size? How does the vendor handle FCA/OIG compliance? |

| Drug Discovery & R&D | Partnership quality, platform validation, pipeline stage | What pharmaceutical partnerships does the vendor have? Has the platform been validated on internal or external datasets? What is the stage of the most advanced pipeline candidate? |

Comments

Join the discussion with an anonymous comment.